Source: Yuan Chuan Research Institute Author: Huang Zhuren / Lin Yedao Editor: Dai Laoban

Intern Yin Ziyi also contributed significantly to this article.

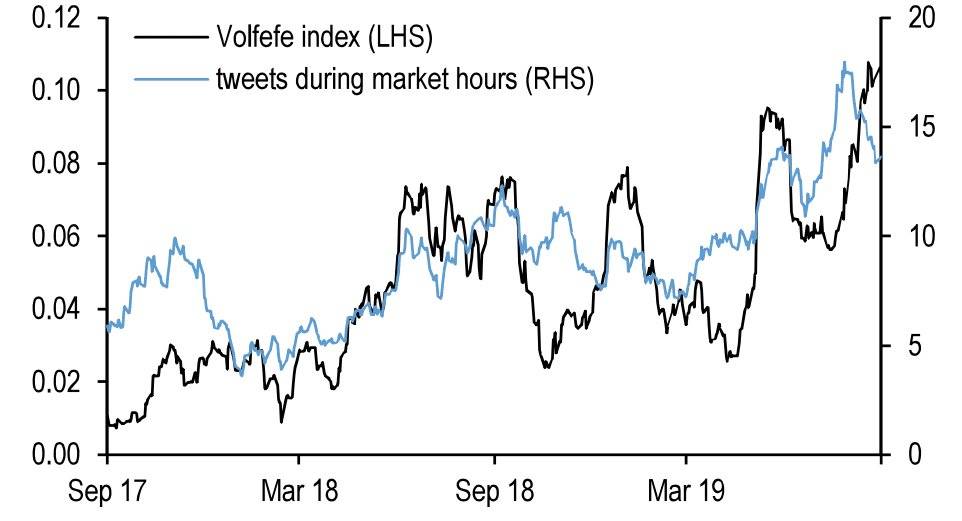

On September 9, 2019, JPMorgan Chase unveiled an unusual new index: the Volfefe Index.

Its purpose was to quantify the impact of President Trump's tweets on U.S. Treasury yields. As JPMorgan noted: "We find that President Trump’s tweets have increasingly moved U.S. interest rate markets immediately after they are posted."

The name "Volfefe" is a blend of "Volatility" and the infamous Trump typo-turned-meme, "covfefe."

The Volfefe Index (left axis) versus the number of Trump's tweets during market hours (right axis).

The "covfefe" saga began in May 2017 with a Trump tweet: "Despite the constant negative press covfefe." The apparent misspelling of "coverage" turned the U.S. President into a global punchline (though some insisted it was intentional). The tweet went viral, with the hashtag #covfefe used 1.4 million times within 24 hours.

While Wall Street poked fun, the prevailing reality in financial markets was clear: "Endless analysis, but the market moves on Trump's word."

That year, markets in equities, bonds, or forex would swing decisively wherever Trump aimed his Twitter commentary, leaving many frustrated traders in their wake. His apparent market-moving power was so precise it even raised suspicions of insider influence. Meanwhile, his outlandish threats—like "Impeach me, and the stock market crashes" or "If I’m not re-elected, you’ll see a market crash the likes of which you’ve never seen"—began to carry real weight and genuinely spook investors.

Historically, U.S. presidents have kept their distance from taking credit for stock market performance. In the late 1990s, when Bill Clinton tried to associate himself with the rising market, he was sharply rebuked by Treasury Secretary Robert Rubin—often called the greatest since Alexander Hamilton. Rubin warned, "You’ll look terrible if the market falls." The dot-com bubble burst soon after, proving Rubin right. Such caution, however, was lost on Trump.

Man proposes, but God disposes. In March 2020, hammered by the pandemic and an oil price war, U.S. stocks plunged into a historic collapse.

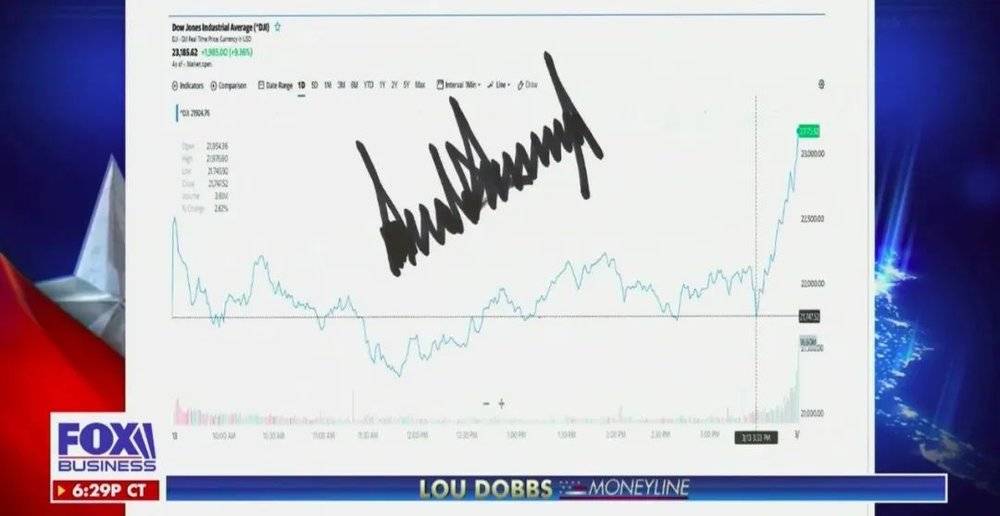

The Commander-in-Chief wasn't ready to concede. On March 13, after declaring a national emergency and pledging full federal resources to fight COVID-19, all three major indices rallied to close up over 9%. Trump then took a screenshot of the market chart, signed it, and sent it to Fox News for broadcast. He even added a line marking the time of his speech, implying the rally was solely due to his decisive action.

Fox News airs Trump's signed market chart, March 2020.

Behind this forced bravado was a Commander-in-Chief whose confidence in steering U.S. stocks—and the unique American capitalist mechanism governing their rise and fall—was fading as markets tanked. The sell-off only intensified afterward. Finally, Trump panicked. Facing the near-13% plunge on March 16, which nearly triggered a Level 2 circuit breaker, he resorted to an uncharacteristically rare plea: "God bless America!"

It's likely too late to try and decouple from the stock market now. As of today, U.S. equity markets have reached levels reminiscent of the 1929 Great Crash.

The pandemic merely tipped over the first domino in an already fragile system. Behind this dramatic market collapse lie the most aggressive share buybacks in history, policy missteps that worsened the situation, distorted incentives, and a shift of capital away from the real economy toward financial assets. While it shares the same human flaws and institutional blind spots, this crisis is fundamentally different from 2008.

To understand where this bear market is headed, we must first understand where the bull market came from.

01. Origins: How the Bull Market Began

U.S. equities enjoyed a bull market for a full decade.

From the 2009 low to the peak earlier this year, the S&P 500 rose 408%, the Dow Jones Industrial Average 357%, and the Nasdaq Composite 669%—with virtually no major corrections along the way. Over $30 trillion in wealth was "created" during this period, cementing U.S. equities as the world's highest-returning capital market.

The main drivers of this rally were internet giants—Facebook, Apple, Amazon, and Google—which replaced aging industrial stalwarts like ExxonMobil and Walmart as the new leaders of the U.S. economy. The dazzling earnings growth of these tech oligopolies, however, obscured the bull market's true engine. Countless analysts proclaimed in reports that "U.S. equity gains are driven by earnings."

This is not quite accurate. While corporate profitability was one pillar of the bull market, the single largest driver of U.S. equities has been corporate share buybacks.

From 2009 through the end of 2017, U.S. non-financial corporations bought back $3.37 trillion of their own shares. ETFs and mutual funds purchased $1.64 trillion, while U.S. households and institutions were net sellers, offloading $655.7 billion and $1.14 trillion, respectively. In other words, since 2009, the largest net buyer in the U.S. equity market has been corporate America itself.

Share buybacks are traditionally seen as a signal from management that the business is healthy and the stock is undervalued. Since 2009, the S&P 500's annualized earnings per share (EPS) growth reached a staggering 9%, suggesting companies were buying back shares due to robust profits. Unfortunately, this is an illusion.

In reality, U.S. corporate profits have stagnated since 2013. As Tianfeng Securities' Song Xuetao pointed out in a research report, according to the Bureau of Economic Analysis (BEA) National Income and Product Accounts (NIPA) methodology, aggregate U.S. corporate profits remain stuck at 2014 levels, and corporate profits as a share of GDP are back to 2005 levels.

The mystery of rising EPS despite flat profits is solved by share buybacks. By repurchasing and retiring shares, companies reduce their share count, artificially boosting EPS even when total profits are unchanged.

Take Walmart as a classic example: from 2009 to the end of 2017, its net income grew by a mere -2.02%, yet its EPS surged 24.13%. This gap is due to Walmart's $64.7 billion in share buybacks over the same period. Because of these buybacks, Walmart's stock price doubled—yet its market capitalization increased by less than 20%.

Over a decade, profits barely budged, yet EPS rose 24% and the stock price doubled. This is the bull market in microcosm.

This bull market has seen a wave of major U.S. corporations, like Walmart, turn to share buybacks. Traditional giants such as Procter & Gamble, McDonald’s, and Coca-Cola—whose stock charts show dramatic climbs—have become standout performers. While the Nasdaq's surge owes much to the internet sector's strength, the rallies in the Dow Jones and S&P 500 have been significantly fueled by share repurchases.

Buybacks directly boost stock prices and improve key metrics like earnings per share (EPS) and return on equity (ROE), making them highly attractive to investors. As Warren Buffett has often noted in his shareholder letters: “We love repurchases when the company’s shares sell at a sensible price.”

In theory, companies should only buy back shares when they're undervalued. Yet in practice, both undervalued and overvalued firms engage in buybacks—some even accelerating them as their stock price rises. Why does this happen?

02. The Distortion: CEOs Cashing In on Rising Shares

A persistent issue for corporations is the misalignment between executive and shareholder interests. While buybacks provide short-term price support, they often do little for long-term growth. Executives' zeal for buybacks is frequently driven by their own stock-based compensation.

U.S. executive pay is heavily weighted toward equity. In strong markets, stock-related compensation can make up over 80% of total pay. For instance, the CEO of Fortune 500 company UnitedHealthcare received $27 million in total compensation, with $20 million from equity awards and a base salary of just $1.2 million.

From 2009 to 2014, Qualcomm spent $13.6 billion to repurchase 238 million shares. Yet its outstanding shares actually increased by 2% during that period due to massive stock and option grants to executives. As the share price rose, executives could cash out for returns far exceeding their salaries.

Faced with such lucrative incentives—and often lacking strict oversight—executives naturally prioritize buybacks to prop up the stock price.

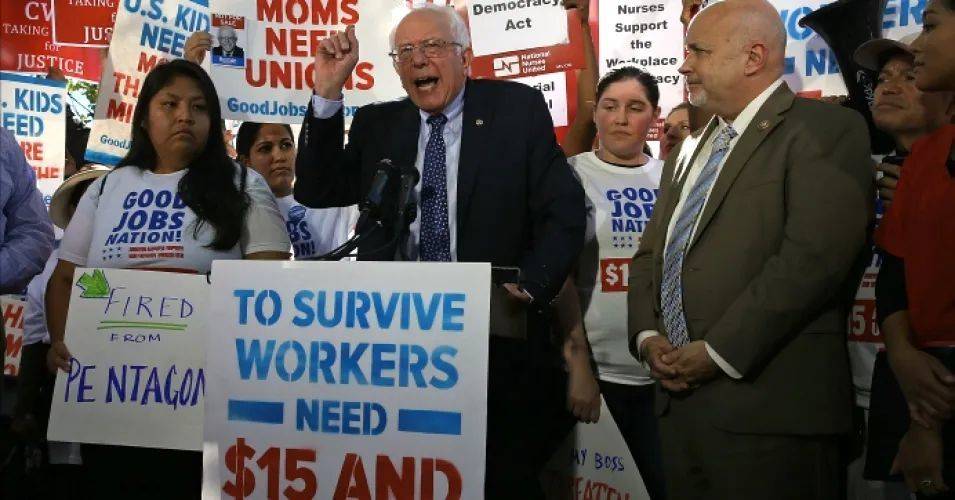

Rising stock prices primarily benefit shareholders and executives, not rank-and-file employees who typically hold little to no equity. In 2019, Walmart announced a $20 billion buyback program while closing dozens of Sam's Club stores and laying off thousands of workers—a move that drew sharp criticism from figures like Bernie Sanders.

Senator Bernie Sanders criticizing Walmart at a rally, 2019.

Buybacks and dividends are meant to reward shareholders. But when buybacks devolve into financial engineering tools to artificially inflate prices, their purpose is distorted. This is especially concerning when struggling companies mimic large-scale buybacks. If healthy companies can afford it, where do weaker ones find the funds?

To answer that, we need to go back to Ben Bernanke, the Federal Reserve Chair during the 2008 financial crisis.

Some athletes are described as "born for the big moment." In 2008, Bernanke was that figure, arriving when most needed. A scholar who had spent his career studying the Great Depression, he became Fed Chair in 2006—just in time to face the worst financial crisis since 1929.

True to form, the lifelong expert in economic crises stepped onto the field, ready to save the American economy.

Ben Bernanke believed the Hoover administration's contractionary policies triggered the Great Depression. Determined not to repeat history during the subprime mortgage crisis, he led the Federal Reserve to act swiftly and decisively. The Fed slashed the federal funds rate from 5.25% to 0% in under a year, injected liquidity directly into banks, and purchased government financial bonds. To revive the frozen credit markets, Bernanke deployed multiple rounds of quantitative easing—essentially "printing money" on a massive scale.

In 2009, Time magazine named Bernanke its Person of the Year, crediting his aggressive use of quantitative easing (QE) and zero interest rates for pulling the U.S. economy back from the brink of another depression.

Ben Bernanke on the cover of Time magazine, 2009

However, while Bernanke averted a repeat of 1929, he created a new and unprecedented problem: seven years of ultra-low interest rates that fueled a massive corporate debt boom in the United States.

By positioning the Federal Reserve and the U.S. government as market backstops, Bernanke's policies revived credit and stimulated the economy through low rates and expanded money supply. For U.S. corporations, debt financing became unprecedentedly cheap. Yet, with post-crisis demand remaining weak, companies were hesitant to invest in productive capacity. Instead, they found an attractive alternative: raising cheap capital through debt issuance to fund share buybacks.

As a result, U.S. corporate debt skyrocketed. Total outstanding corporate bonds stood below $6 trillion at the end of 2009 but have since soared to $10 trillion. With corporate profits stagnant or even declining, debt became a key funding source for share repurchases. Starting around 2011, publicly listed companies established a self-reinforcing cycle: issue debt → buy back shares → boost EPS → drive stock prices higher.

By 2017, U.S. equities had already seen massive gains. Then, like pouring oil on a fire, the market welcomed a leader who treated rising stock prices as a key political achievement.

03. Fueling the Fire: A President Who Treated the Bull Market as a Political Achievement

After taking office in 2017, Donald Trump pursued two major initiatives that directly or indirectly boosted equity markets: a sweeping tax-cut bill and relentless pressure on the Federal Reserve to lower interest rates.

The 2017 Tax Cuts and Jobs Act forced U.S. multinationals to repatriate overseas earnings. Rather than investing this capital into business expansion, companies funneled it from the "real" economy into financial markets—creating a massive inflow into equities. In 2018, the U.S. stock market witnessed its most aggressive wave of large-cap buybacks in history, with S&P 500 repurchases surging 23% to a record $650 billion.

Trump's tax cuts were originally intended to revive manufacturing, but they failed to deliver the expected results. Instead, the legislation created a $1 trillion fiscal deficit within a single year. Facing unprecedented fiscal pressure, it became obvious even to a layperson: lower interest rates would save the federal government tens of billions annually on its $20 trillion debt burden.

Thus, Trump turned his focus to the Federal Reserve. Initially, he met resistance from Chair Janet Yellen, who held her ground.

Yellen, Bernanke's successor, had begun guiding the Fed to raise interest rates and shrink its balance sheet in 2016. She proceeded methodically, aiming to normalize policy without derailing the economic recovery. After three rounds of QE, the Fed's balance sheet had ballooned from under $1 trillion before the crisis to $4.5 trillion. Yellen systematically began reducing this figure while simultaneously initiating a gradual rate-hiking cycle.

Yellen vs. Trump

When Jerome Powell took over as Federal Reserve Chair in 2018, he initially stuck to Janet Yellen's playbook—steady and resolute. But for the debt-laden U.S. economy, the medicine of rate hikes and balance sheet reduction proved too bitter to swallow. Markets churned throughout 2018 and plunged sharply in the fourth quarter, breaking below their annual moving average. For Donald Trump, who saw rising stock prices as a core political achievement, this was simply unacceptable.

In 2019, Trump repeatedly lashed out at the Fed on Twitter, calling it "stupid" and its officials "idiots," while insisting the U.S. needed even lower rates to keep its manufacturing sector competitive. In August alone, he attacked the Fed 25 times. The result? The Fed cut rates three times—in July, September, and October—and restarted quantitative easing (QE) in September.

And just as Trump wanted, U.S. stocks soared to new highs.

The Fed's renewed balance sheet expansion became a key engine for the equity rally.

If the tax cuts directly encouraged tech giants to buy back shares, persistently low market rates indirectly protected companies borrowing to fund those buybacks.

Trapped in the cycle of issuing debt, buying back stock, boosting EPS, and pushing share prices higher, many U.S. corporations have drifted further into dangerous waters.

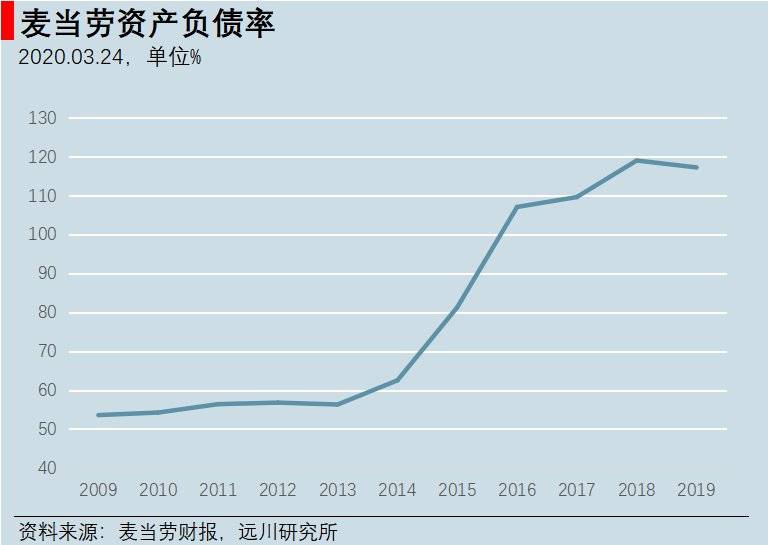

Between 2008 and 2015, McDonald's spent about $18 billion on share repurchases. Over the same period, the share of executive pay tied to stock incentives jumped from under 40% to nearly 80%. Its total liabilities ballooned from $16 billion to $30.8 billion. And because most repurchased shares were recorded as treasury stock (excluded from assets), McDonald's became technically insolvent—with liabilities exceeding assets—starting in 2016.

McDonald's debt-to-equity ratio has exceeded 100% since 2016.

It must be said: McDonald's never fails to upend Chinese perceptions of its business model. First, people thought it sold burgers; then they learned it was essentially a real estate play; now, it's a company that borrows money to speculate on its own stock.

04. The Downward Spiral: A Fragile Market and Weakening Companies Amid Soaring Prices

In the end, borrowing to trade stocks inevitably leads to a mountain of debt and growing reliance on rolling it over. Sooner or later, the game becomes unsustainable.

The debt growth of publicly listed companies far outpaces that of the broader U.S. corporate sector. While total corporate debt sits at about 47% of GDP—only slightly above pre-crisis levels—the debt of listed companies alone has reached 20% of GDP, well above the 13% seen during the subprime crisis. The $10 trillion corporate bond market is effectively tapped out.

The market's underlying fragility was laid bare by the brief interest rate hike in 2018 and the subsequent crash.

Corporate debt has ballooned to unsustainable levels, while companies' ability to service that debt is rapidly deteriorating. Outside of the tech giants, the performance of U.S. corporations continues to weaken. Over the past decade, the proportion of unprofitable companies in the Russell 3000 Index has surged; today, a quarter of them are in the red.

This has led to a deterioration in corporate credit ratings. BBB is the lowest investment-grade rating; anything below is considered high-yield or "junk" bonds, which conservative investors like pension funds typically avoid. The outstanding volume of BBB-rated bonds has soared to $3.3 trillion, now making up a record 50% of the entire investment-grade bond market. A decade ago, that share was only about 30%.

BBB-rated bonds carry significant hidden risk: if downgraded, many institutional investors are forced to sell. These downgraded bonds are known as "fallen angels." The entire high-yield bond market—bonds rated below BBB—is currently only about $1 trillion in size.

Historically, when the credit cycle turns, roughly 10–15% of BBB-rated bonds become fallen angels. This means a recession could trigger nearly $500 billion in downgrades—the largest wave of fallen angels ever. That would instantly flood the high-yield market and inevitably lead to a wave of corporate bankruptcies.

Savvy investors have long been wary of the crisis brewing in U.S. corporate debt. Steve Eisman, a fund manager with deep experience in mortgage-backed securities and one of the real-life inspirations for *The Big Short*, put it bluntly: "When the next recession hits, BBB and high-yield corporate bonds will get crushed. Corporate debt won't cause the recession, but it will be where the pain is most acute."

Eisman isn't the only one sounding the alarm. Scott Minerd, Global Chief Investment Officer at Guggenheim Partners, which manages $310 billion, wrote in January: "With the Fed cutting rates and U.S. stocks hitting new highs, the current market looks eerily similar to the period before the 1998 crisis. A 'Minsky Moment' could be imminent."

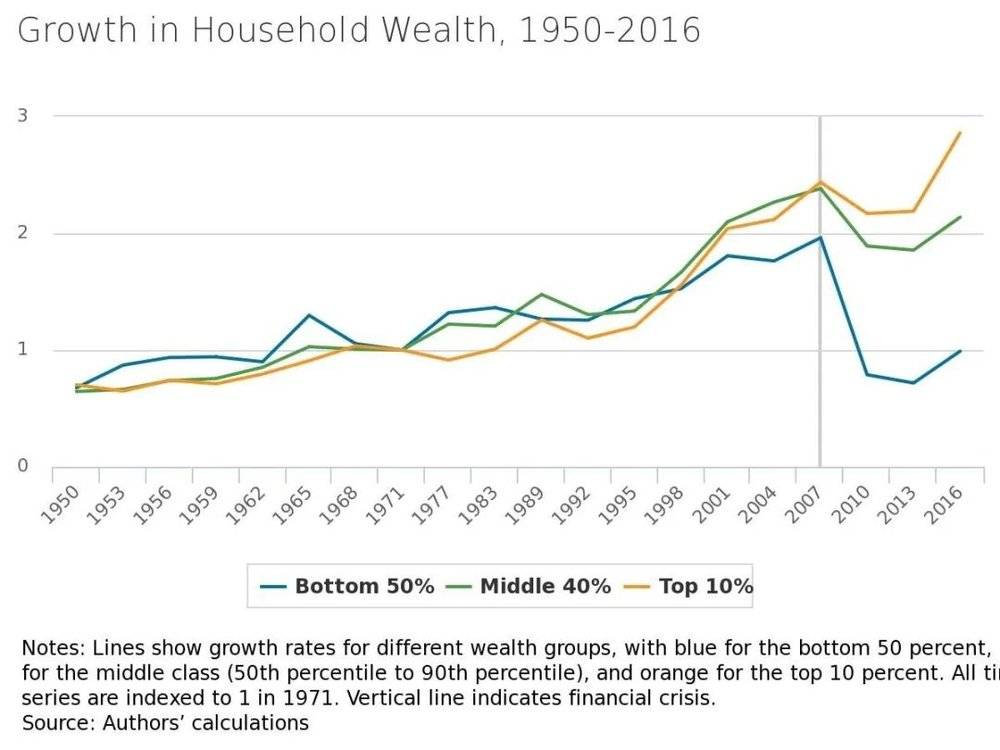

The frenzy of debt-fueled buybacks during the bull market has also exacerbated wealth inequality in the U.S.:

The wealth effect from rising markets has largely bypassed most Americans. According to Gallup, about half of Americans under 35 were invested in stocks before the 2008 crash; by 2018, that figure had fallen to just 37%.

U.S. household wealth growth has diverged sharply since 2008—Minneapolis Fed

Ironically, over the past two years of record highs, retail investors have started returning to the market. Fed data shows that since 2016, individual investors have been net buyers of U.S. stocks for the first time since the dot-com bubble. It seems no matter where they are, retail investors often end up holding the bag.

The market is waiting for the first domino to fall. Until it does, no one knows exactly what shape it will take.

05. Shock: The Gray Rhino Has Finally Arrived!

On January 23, 2020, Wuhan went into lockdown. That same noon, an interview with Professor Guan Yi was published. By that afternoon, China's Shanghai and Shenzhen stock markets had plunged, with all three major indices dropping nearly 3%.

Amid the pandemic, a surprisingly optimistic report from JPMorgan on January 30 struck a hopeful note. It argued that while the outbreak was hurting China's economy—dampening demand and trade—it might actually stabilize markets for U.S. investors. The reasoning? History shows that prolonged stock market declines due to public health crises, natural disasters, or political turmoil are rare.

At first, U.S. stocks seemed to prove them right—they not only held steady but climbed. By February 19, all three major indices had hit record highs. The optimism was short-lived. On February 24, as Italy's outbreak intensified, the S&P 500 gapped down at the open and plunged over 3%. The next day, with 57 confirmed cases in the U.S., the major indices fell another 3% or more. From there, both the pandemic and the markets spiraled out of control.

In contrast, Scott Minerd, Chief Investment Officer at Guggenheim Partners—who had previously warned of a "Minsky Moment"—offered a stark assessment on February 28: "We are at a tipping point. Either the pandemic is brought under control quickly, or the world faces a full-blown crisis. I'm not an epidemiologist, so I'll leave the specifics to the experts. But if the coronavirus spreads widely in the U.S., equity markets could fall much further—potentially up to 40% from their peak."

On March 3, the Federal Reserve made an emergency 50-basis-point rate cut, but markets shrugged it off. Then came a second major shock: the Saudi-Russia oil price war that erupted on March 8, sending crude prices down 30%. For U.S. energy stocks, it was a catastrophe. On March 9, the S&P Oil & Gas Exploration & Production Index plummeted 28%, triggering a market-wide circuit breaker at the open.

What followed was a relentless collapse: four circuit breakers in ten days, marking the definitive start of a full-blown U.S. stock market crash.

Boeing's stock performance was a telling example. After a near-vertical collapse, its share price lost 70% of its value. America's premier industrial champion, once boasting a market cap rivaling Kweichow Moutai, saw its status evaporate overnight. Even through past aircraft safety incidents, its stock had shown resilience. This time, it found no support.

Boeing's stock price decline was astonishing

On March 20, Boeing's corporate credit rating was downgraded from 'A' to 'BBB'. If the pandemic persists, weakness in aviation could push the company toward bankruptcy—its interest-bearing debt exceeds $40 billion.

While the pandemic and oil price crash are clearly hurting corporate operations, the market's extreme reaction stems largely from high leverage. Fragile financial systems are vulnerable to even minor shocks. More alarmingly, despite the severe stock collapse, the financial system—already burdened with multiple overlapping risks—has yet to defuse some of its most dangerous "bombs."

The corporate bond bubble has only just entered its first phase. Although BBB-rated corporate bonds have been heavily sold off since February 24, widespread rating downgrades have yet to materialize. As of March 20, the yield spread on BBB-rated bonds had only just reached the level seen on September 15, 2008—the day Lehman Brothers filed for bankruptcy. Recall that after Lehman's collapse, the S&P 500 plunged another 40%.

If the subprime crisis unfolded as "asset price decline → complex derivatives blow-up → financial institution failures," then the current corporate bond crisis is still firmly in Phase One.

Meanwhile, ETFs—another key driver of this bull market—have been blamed by many investors as potential catalysts for cascading sell-offs. As early as September 2019, Michael Burry—the real-life inspiration for one of "The Big Short" protagonists—warned that ETF liquidations could trigger a stampede.

However, the data doesn't support this. Deng Hu, Chief Analyst for Financial Products at Everbright Securities, calculated that U.S. equity ETFs actually saw over $10 billion in net inflows over the past three weeks. There's no evidence that ETF redemptions triggered a rapid, cascading market collapse.

The author speculates that the most critical factor behind the market's unprecedented speed of decline may indeed be Bridgewater Associates' risk parity strategy.

For the past few years, U.S. stock market volatility has been on a steady decline, with markets climbing smoothly. This environment made risk-parity strategies wildly popular—maintaining high equity exposure while shorting volatility proved to be a remarkably profitable trade. However, when extreme market conditions hit, this strategy can trigger a self-reinforcing cascade of forced liquidations. Recent reports of heavy losses at Bridgewater Associates are likely tied to insufficient hedging for its massive equity positions.

If the current downturn is indeed driven primarily by risk-parity unwinding, then the recent stock market crash may be just a taste of what's to come. The real "gray rhino"—the corporate bond crisis—has yet to charge. When it does, the problems could become far more severe.

06. Epilogue: The End of an Era?

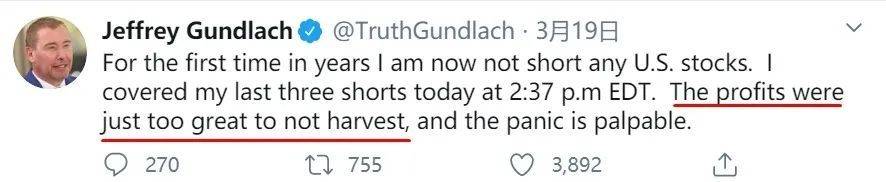

Jeffrey Gundlach, the so-called "Bond King," was among the first to warn of the corporate bond bubble. On March 19, he tweeted that he had closed his last three short positions, marking the first time in years he held no short exposure to U.S. equities. The profits from those shorts were staggering, and market panic was palpable.

Looking back, anyone would regret not heeding this legendary investor's outlook earlier this year. One of his more stark predictions included the following historical parallel:

“In the late 1980s, Japan's markets vastly outperformed the rest of the world. Its real estate market boomed and the Nikkei 225 soared. Then, a sharp recession hit in the early 1990s, and the Nikkei collapsed.

In the late 1990s, Europe took center stage. There was widespread, almost blind optimism that the euro could become a reserve currency. Shortly after its 1999 launch, European markets led global equities—only for a recession in the early 2000s to send them plunging.

Then came emerging markets in the mid-2000s, fueled by a weak dollar and China's rise. They led global indices until they, too, succumbed to recession.

None of these markets ever reclaimed their previous peaks.

Today, the S&P 500 has enjoyed a decade-long bull run, outperforming other equity markets by nearly 100%. When the next recession arrives, U.S. stocks will collapse—and the U.S. dollar will weaken further under the weight of soaring fiscal deficits.

For the rest of my career, U.S. equities will never again trade at today's levels.

So, decades from now, will U.S. stock investors look back at the S&P 500's peak of 3,393 points with the same nostalgic affection we hold for the Shanghai Composite's 6,124-point high?

Gundlach's deep pessimism likely stems from his sharp analysis of America's debt problem. He argues that since the 1980s, all U.S. economic growth has been debt-fueled. This ever-expanding debt is a perpetual Sword of Damocles hanging over the economy; the Federal Reserve's accommodative policies are fundamentally just delaying the inevitable rollover of this massive debt burden.

During this pandemic, the Fed has moved with unprecedented speed—both its aggressive rate cuts and its $700 billion quantitative easing (QE) program exceeded expectations. Then, on March 23, it announced plans for unlimited bond purchases, injecting limitless liquidity into the market in an extraordinary monetary expansion. To paraphrase a popular saying: "We thought they were running a fish pond, but it turns out they control the entire ocean."

In a crisis, survival comes first—that's understandable. But can growth fueled by debt last forever? The answer, of course, is no.

In his seminal book Principles for Navigating Big Debt Crises, Ray Dalio outlines four policy tools for tackling long-term debt burdens: 1) Fiscal austerity; 2) Debt default and restructuring; 3) Central bank money printing and asset purchases; and 4) Wealth redistribution. Given the near-limitless credit capacity of the U.S. government and the Federal Reserve, nearly every debt crisis has been resolved at step three.

However, the asset price surges that follow monetary easing inevitably widen the wealth gap.

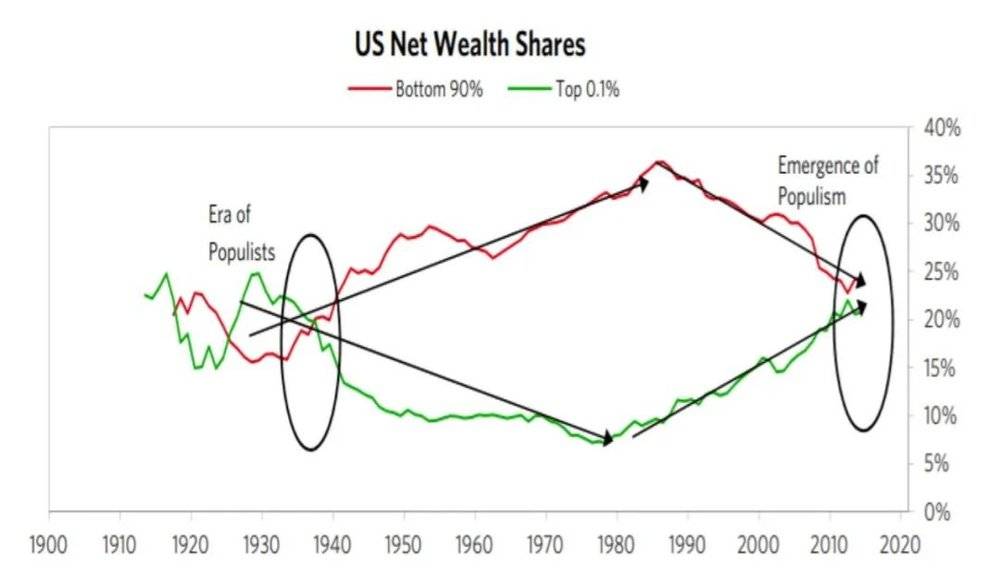

Today, wealth inequality in the U.S. has returned to levels not seen since 1929. In 2016, the top 1% of Americans held 38.9% of the nation's total wealth, while the bottom 50% of households owned just 1%. Burdened by the high costs of education and healthcare, the middle class is increasingly reliant on debt—and 40% of Americans lack $400 in emergency savings.

U.S. wealth inequality has returned to 1929 levels, Principles for Navigating Big Debt Crises

During the pandemic, unemployment and medical bills have become unbearable for ordinary families. Without intervention, household balance sheets would deteriorate rapidly—threatening social stability. This necessity is driving the U.S. plan for a one-time $3,000 cash payment to households. Ultimately, deep-seated structural problems require targeted monetary expansion to address.

This makes the current crisis especially alarming: the market crash is battering corporate balance sheets, while the pandemic is ravaging household finances. Both require long-term structural fixes, yet neither can wait. The short-term "band-aid" solutions applied to these problems will inevitably create new challenges. How to resolve these century-scale dilemmas remains an open question—not just for America, but for the entire world.

Whether it's the pandemic or market turmoil, the story unfolding across the Pacific is still being written. Understanding why systems fail is essential to inspiring how we build. From this perspective, the structural issues beneath surface-level events offer critical case studies—ones we must examine, review, and heed with vigilance.