Author: Kyle, Investment Manager at Bing Ventures

Key Takeaways:

Bitcoin and Ethereum are forming robust value networks. More importantly, they constitute the foundational trust layer of cryptocurrency—implying that stablecoin projects built atop these value networks enjoy solid asset backing. However, improvements in user experience and the scale of assets locked into the network will be the primary differentiators determining their relative value;

Stablecoins issued by super-apps with established user bases effectively bypass traditional trust intermediaries, establishing direct minting agreements with their users. In such cases, protocols like Curve, Aave, and Synthetix become “super pawnshops.” Their users gain access to customized financial services faster and more seamlessly than in traditional finance. User scale and business innovation determine their ceilings; the author is particularly bullish on Synthetix’s prospects;

Fully chain-agnostic algorithmic stablecoins have the potential to achieve true decentralization, cross-chain interoperability, and infinite scalability. They can be freely issued, transferred, and traded across any blockchain, thereby enabling cross-chain interoperability and portability.

Additionally, delta-neutral stablecoin models may emerge as a significant trend going forward. However, implementing such models requires corresponding futures protocol support, while also demanding careful attention to risk management and market adaptability.

An algorithmic stablecoin is a cryptocurrency whose price stability is maintained primarily through algorithmic mechanisms rather than full reliance on reserve-backed collateral. In practice, however, some algorithmic stablecoins have failed to maintain price stability and face risks including insufficient market liquidity and black-swan events. Some argue this stems from an inherent flaw—the “original sin”—of algorithmic design.

This industry research report by Bing Ventures focuses on algorithmic stablecoins. By analyzing current types, mechanisms, and challenges facing algorithmic stablecoins, it explores future development directions. The author posits that, as algorithmic stablecoins evolve, they will form a global hierarchical stablecoin system—some achieving top-tier status while others serve as multi-layered peripheral complements. Unlike traditional fiat currencies, algorithmic stablecoins can be created and traded globally without being constrained by any single nation’s regulatory framework. Consequently, algorithmic stablecoins hold strong potential to become the dominant monetary instruments within the future decentralized finance (DeFi) ecosystem.

The Original Sin of Algorithmic Stablecoins

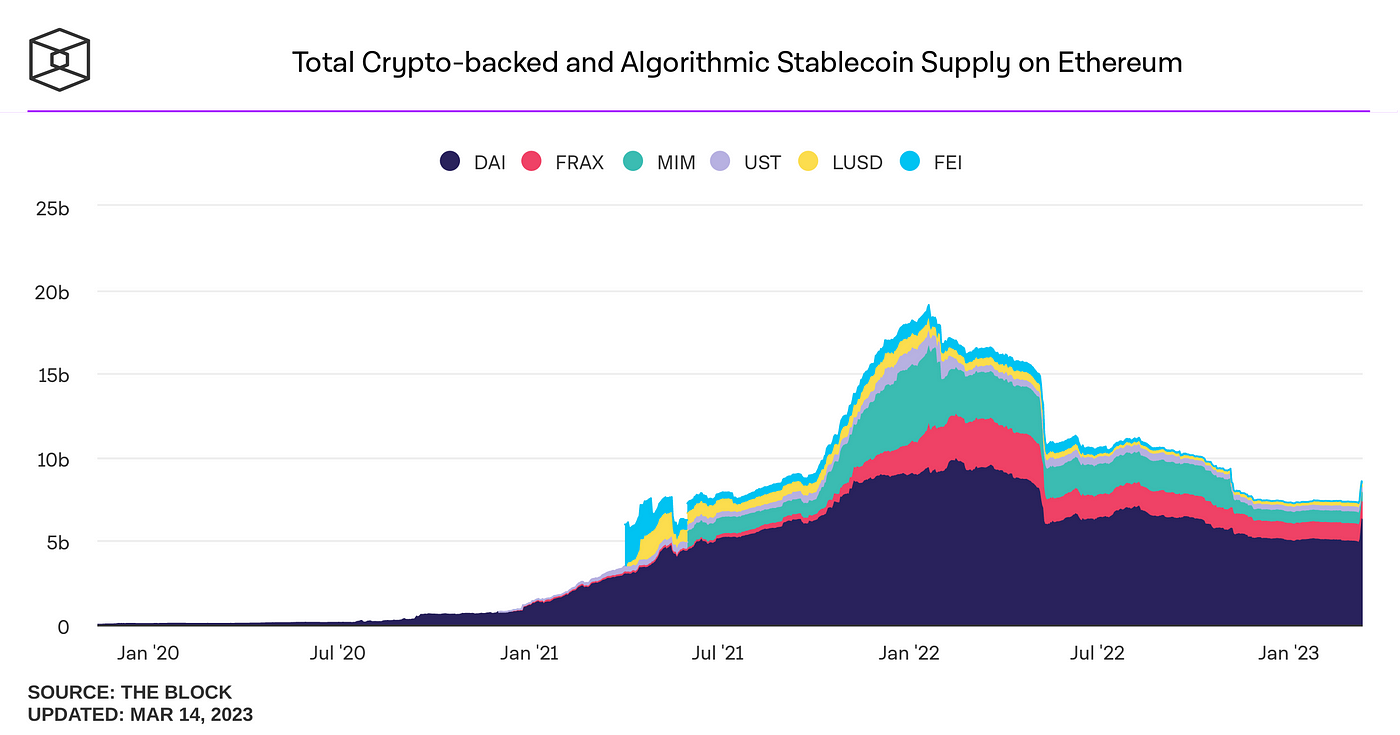

Algorithmic stablecoins employ mechanisms analogous to shadow banking, creating an offshore space for monetary creation. Unlike traditional stablecoins, they do not rely on centralized entities to maintain stability but instead use algorithms to regulate supply and demand, keeping prices within a target range. This monetary form faces multiple challenges, including insufficient market liquidity and exposure to black-swan events.

Source: The Block

Algorithmic stablecoins utilize various algorithmic mechanisms to adjust supply and demand to maintain their peg to a target value—typically the US dollar. Two classic algorithmic mechanisms have emerged:

Rebase: Rebase-based algorithmic stablecoins influence price by adjusting the base supply. When the stablecoin’s price exceeds its target, the protocol mints additional tokens to reduce price; when price falls below target, the protocol burns or repurchases tokens to increase price. For example, Ampleforth employs the Rebase mechanism.

Seigniorage: Seigniorage-based algorithmic stablecoins issue a secondary cryptocurrency to underpin the stablecoin’s value. When the stablecoin trades above its target, the protocol uses seigniorage tokens as collateral to mint and sell additional stablecoins into the market; when trading below target, the protocol uses market proceeds to buy back and burn seigniorage tokens. For example, Basis Cash utilizes the seigniorage mechanism.

Beyond these two foundational mechanisms, emerging algorithmic stablecoin projects are experimenting with novel innovations to maintain their peg. Frax, for instance, is a partially collateralized algorithmic stablecoin combining fiat-backed collateral with the seigniorage model. Frax uses USDC as part of its collateral and dynamically adjusts its collateral ratio based on market demand. Unlike traditional stablecoins, algorithmic stablecoins derive value not solely from external reserves but from algorithm-driven market mechanisms regulating supply and demand to preserve price stability. Yet in recent years, algorithmic stablecoins have encountered several key issues:

Supply-Demand Imbalance: When market demand for an algorithmic stablecoin declines, its price falls below the target, prompting issuers to burn or repurchase circulating supply to restore equilibrium. However, this action may further erode market confidence and demand, triggering a downward spiral—a scenario most brutally exemplified by Terra.

Governance Risk: Because algorithmic stablecoins operate via smart contracts and community consensus, they face governance risks—including code vulnerabilities, hacker attacks, human manipulation, or conflicts of interest.

Regulatory Uncertainty: Lacking physical assets as backing or peg, algorithmic stablecoins confront heightened legal and regulatory challenges and uncertainty. More jurisdictions are expected to restrict or ban their use in the future.

Mainstream Mechanism: Semi-Decentralized Over-Collateralized / Fully-Collateralized

Multiple algorithmic stablecoin mechanisms exist today in DeFi. Prominent examples include MakerDAO’s collateralized lending model—issuing DAI against locked ETH and adjusting stablecoin supply based on market demand—and Aave’s liquidity pool model, which dynamically adjusts stablecoin pricing in real time according to supply-demand dynamics and arbitrage across multiple stablecoins to maintain peg stability.

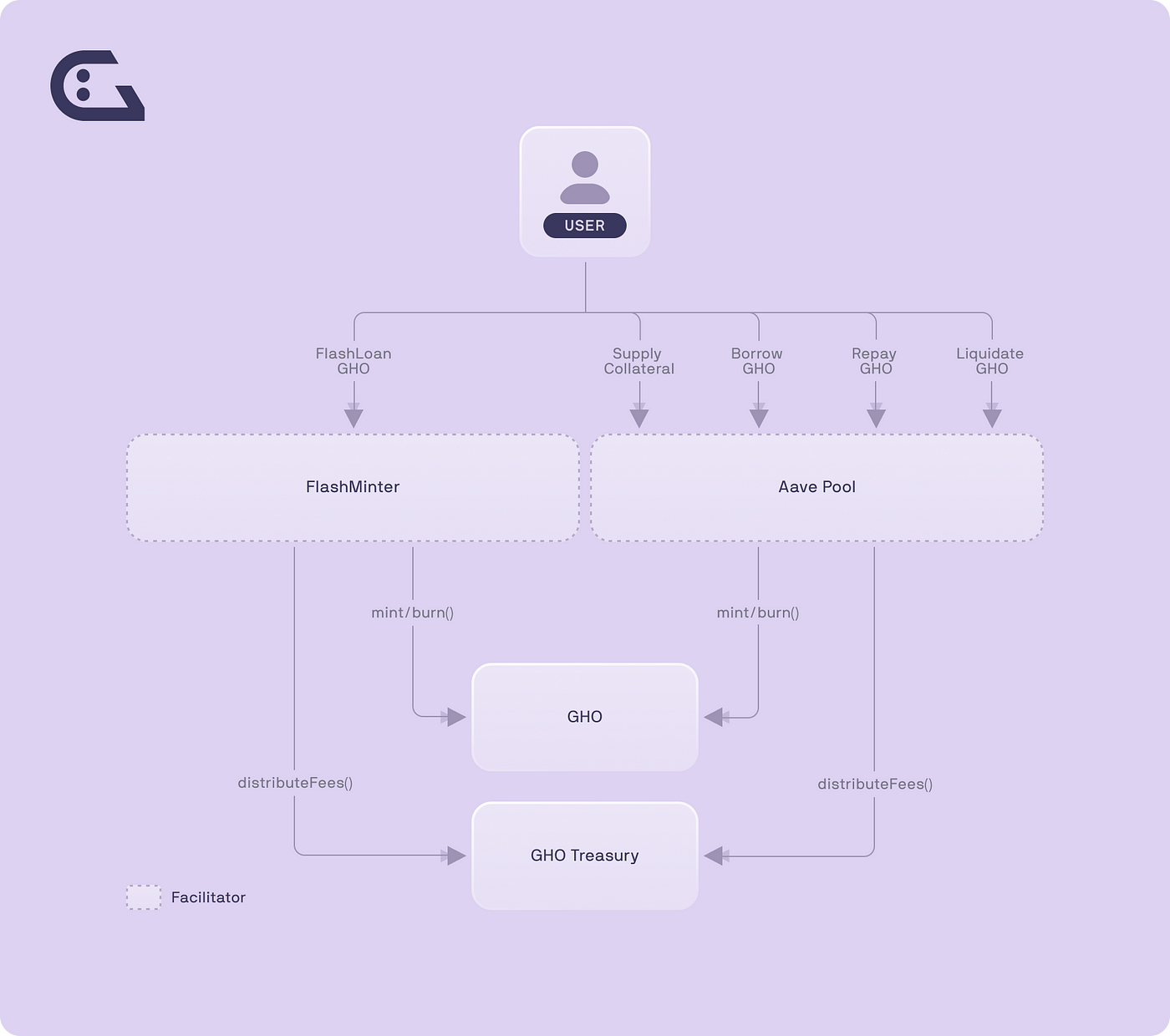

GHO: Aave’s Deposit-Supported Stablecoin

GHO is a decentralized, multi-collateral stablecoin pegged to the US dollar (USD). Users or borrowers can mint GHO tokens on the Aave protocol using their chosen basket of crypto assets as collateral. When Aave loan users deposit crypto assets as collateral to borrow GHO, Aave mints new GHO tokens. Upon loan repayment, Aave burns the corresponding GHO tokens, reducing the total token supply in the protocol. GHO tokens can be used for payments, lending, and other applications—and generate yield automatically by participating in Aave’s liquidity mining program.

GHO adopts Aave V3’s liquidity pool model, with Aave acting as the sole liquidity pool provider. Users must interact with Aave V3 to purchase and use GHO. Future expansion may include adding additional liquidity pool providers to enable decentralized stablecoin issuance and trading. Only assets held within the Aave protocol qualify as collateral for GHO. All revenue generated from GHO accrues directly to the Aave Treasury and subsequently flows to the Aave DAO. Fundamentally, GHO is an innovative stablecoin integrating decentralization, multi-collateralization, and yield-bearing features—especially seamless integration with other Aave protocol services.

However, GHO’s stability depends critically on the value and liquidity of its underlying collateral. Severe market volatility or liquidity crises could cause GHO to lose its peg and trigger liquidations. Enhancing GHO’s risk management and advancing its decentralization remain critical concerns. As more liquidity pool providers join, risk allocation and incentive distribution will grow increasingly complex—requiring more sophisticated decentralized governance mechanisms to ensure GHO’s long-term stability and sustainability.

Source: Aave

CrvUSD: The LLAMMA Algorithm

CrvUSD is an algorithmic stablecoin whose core design centers on the Lending-Liquidating AMM Algorithm (LLAMMA). This algorithm maintains price stability by converting between collateral (e.g., ETH) and stablecoin (USD). When collateral appreciates, users’ entire deposits convert to ETH; when collateral depreciates, conversions shift toward USD. Collateral options may also include positions in liquidity pools (LPs).

This differs significantly from traditional AMM designs, where USD is typically placed at the top and ETH at the bottom. In Curve’s algorithmic stablecoin, the LLAMMA algorithm aims to provide users with a soft liquidation window—converting collateral into LP positions to avoid abrupt liquidations of collateral. Curve’s stablecoin mechanism maintains price stability and liquidity through cross-chain liquidity aggregation, multi-strategy pool liquidity convergence, and synergies with other DeFi projects. Additionally, Curve stablecoins can generate returns via trading, lending, and liquidity mining, thereby incentivizing broader participation in its ecosystem.

Source: CrvUSD Whitepaper

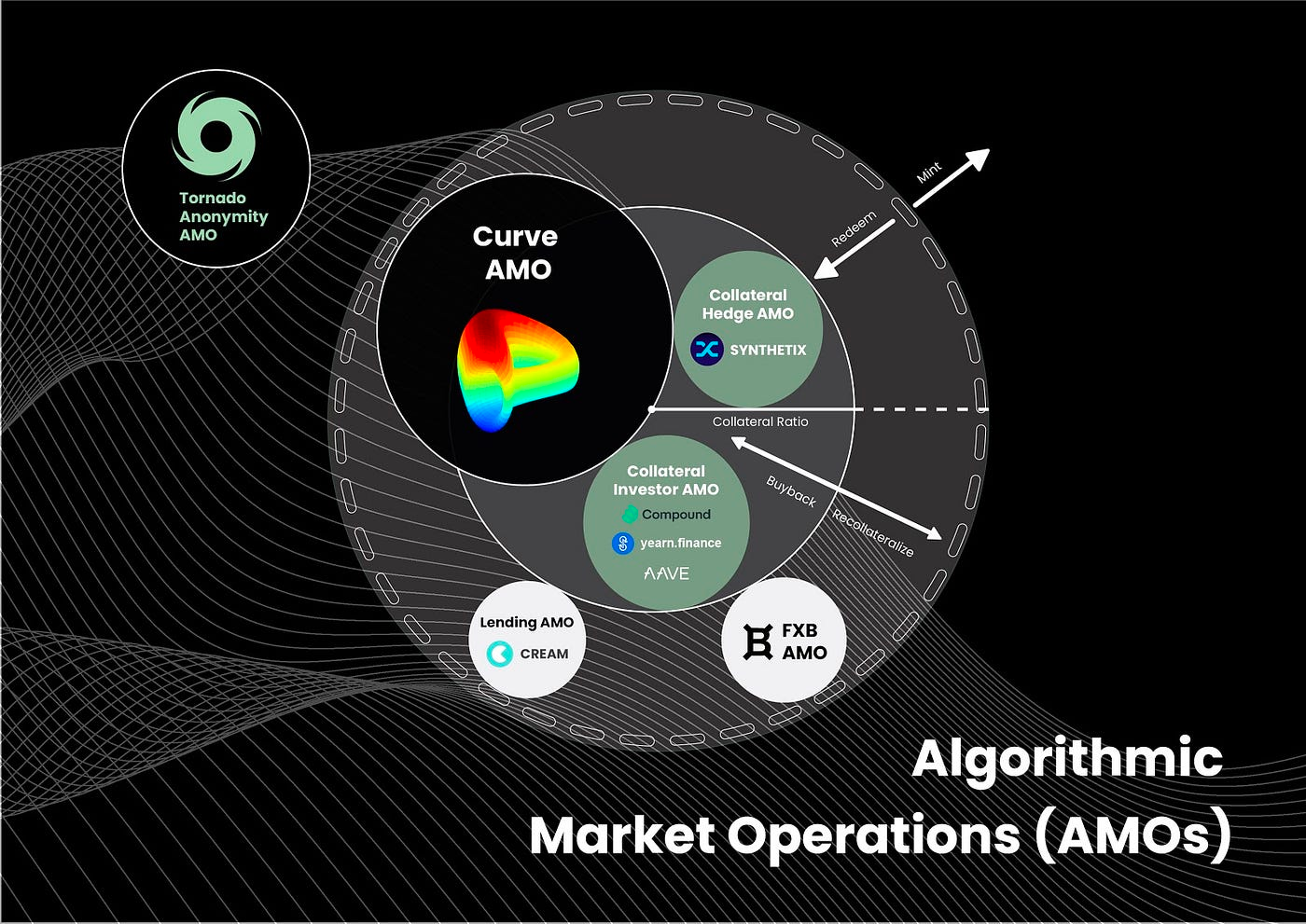

Frax: The Ambition of AMOs

Frax is partially backed by collateral assets and partially by its native token, FXS. The proportion of these two components in Frax’s backing is referred to as the collateral ratio. Typically, USDC serves as the primary collateral asset. The Frax protocol dynamically adjusts this collateral ratio based on the market price of FRAX tokens. If FRAX trades above $1, the protocol lowers the collateral ratio—reducing reliance on collateral and increasing the algorithmic portion. Conversely, if FRAX trades below $1, the protocol raises the collateral ratio—increasing trust in collateral and reducing the algorithmic portion. Through this mechanism, the Frax protocol seeks to maintain FRAX’s peg to the US dollar.

In its V2 upgrade, Frax introduced an Algorithmic Market Operations Controller (AMO) mechanism, which reinvests collateral into Frax pools to generate additional revenue supporting protocol growth. Frax’s community has agreed to abandon the dual-token model and raise the target collateral ratio to 100%, making Frax a more attractive long-term store-of-value asset for users. This increase in the collateral ratio will be achieved via the AMO mechanism—not through FXS token sales.

The AMO enables fully programmable monetary policy without lowering the collateral ratio or altering the FRAX price. The AMO controller is an autonomous smart contract capable of executing algorithmic open-market operations—but it cannot break the peg solely by minting FRAX. The AMO controller makes FRAX one of the most robust stablecoin protocols, delivering maximum flexibility and opportunity while preserving its core stability mechanism.

However, the Frax protocol still relies on external stablecoins as its ultimate backstop. Should an external stablecoin fail or become frozen—as occurred recently with USDC’s de-pegging event—it would directly impact Frax’s stability and security. Frax also depends on the FXS token for governance and incentives; significant FXS price volatility or declining demand could likewise impair Frax’s operations and development.

Source: Frax

Overall, GHO and crvUSD hold advantages in terms of established market positioning, diverse use cases, and investment appeal. While Frax demonstrates strong technical capabilities, it has yet to withstand large-scale market volatility—its real-world applicability and investment value remain to be observed. Going forward, GHO and crvUSD may further solidify their moats by continuously launching new products and expanding use cases.

Current Challenges

The primary risk facing these stablecoins lies in the growing complexity of their underlying protocols, which expands the attack surface—potentially enabling sudden, devastating “surprise attacks” across entire ecosystems. In recent years, we have witnessed numerous catastrophic failures where stablecoin vulnerabilities led to complete protocol insolvencies. Competition in the stablecoin space is also intense: some decentralized stablecoins have built formidable moats through deep on-chain liquidity and strategic integrations with other protocols (e.g., Aave and Curve). Moreover, native stablecoins issued by single protocols often struggle to achieve deep liquidity—or doing so comes at prohibitively high cost.

Currently, stablecoin development follows two dominant paths: collateralized stablecoins and algorithmic stablecoins—the former sometimes termed “quasi-algorithmic.” Yet both models face inherent challenges: collateralized stablecoins require substantial over-collateralization, while algorithmic mechanisms risk liquidity shortages and inequitable reward distribution.

By contrast, the previously popular “liquidity-backed” model effectively prioritizes “protocol-controlled value” over “algorithmic stability.” However, empirical evidence over the past two years shows that “liquidity-first, not collateral-first” designs are flawed—for instance, during market contractions, insufficient liquidity leads to unfair rewards for holders and DAOs, potentially enabling whale manipulation and undermining long-term ecosystem stability.

Source: Bing Ventures

I. Low Acceptance as a Store of Value

These algorithmic stablecoins currently face hurdles in user adoption. Their main drawback is inferior stability compared to mainstream fiat-backed stablecoins like USD—leading users to treat them primarily as yield rewards rather than reliable stores of value. DAI, as the pioneer decentralized stablecoin, has secured a notable market share. Yet its position has been challenged by the rise of dominant fiat-backed stablecoins such as USDC.

Moreover, algorithmic stablecoin mechanisms tend to be complex and difficult to understand, requiring users to hold multiple tokens and perform various actions to sustain stability. This increases user costs and risks while diminishing usability. Algorithmic stablecoins remain under-adopted, with relatively low market share and liquidity—limiting their utility in payments, lending, cross-border remittances, and other domains, and weakening their appeal as stores of value.

Thus, algorithmic stablecoins must further address stability issues to function more effectively as stores of value. Additionally, they need to better align with user needs—such as offering higher yields—to attract broader adoption. Integrating with real-world assets could enhance liquidity and intrinsic value, boosting competitiveness.

II. Dependence on Diversified Collateral

Currently, algorithmic stablecoin protocols still require certain amounts of collateral such as ETH and CRV—and scalability hinges on continuous appreciation of collateral value. These protocols also face tangible demand-side risks. Some have already exhausted their insurance funds. Whether “more collateral is always better” remains highly questionable.

In the short term, diversified collateral support may strengthen network effects and boost liquidity—especially during bull markets. But long-term, this approach represents a reckless speculative experiment undermining the very stability and security of algorithmic stablecoins. We may need to draw more liquidity from centralized exchanges to improve the viability of algorithmic stablecoin protocols.

Notably, even protocols like Frax—which employ algorithmic stabilization—see their decentralization ratios decline sharply under intense redemption pressure, exposing holders to greater risk. At its core, algorithmic stabilization implies under-collateralization, inherently elevating risk. Mainstream DeFi protocols aim to position their stablecoins as competitors to centralized stablecoins like USDC—but meeting regulatory requirements remains exceptionally difficult. Therefore, algorithmic stablecoins must better resolve decentralization challenges and identify broader application scenarios to fulfill their future potential.

Exploring Decentralized Algorithmic Stablecoins

BTC/ETH-Native Models

LUSD: Liquity’s Native Stablecoin

LUSD is a stablecoin launched by Liquity. Liquity is a decentralized lending protocol enabling users to borrow against ETH collateral at 0% interest. LUSD’s algorithm mandates borrowers maintain over-collateralization; otherwise, their loans face liquidation. LUSD claims rigid redeemability. It also benefits from non-mandatory mechanisms—such as the protocol treating LUSD as equivalent to USD, and charging borrowing fees on newly created debt. These mechanisms influence LUSD’s supply-demand dynamics and market expectations, helping maintain its price within a $1.00–$1.10 band.

LUSD offers interest-free borrowing, allowing users to unlock liquidity from ETH holdings and enhancing capital efficiency. It also incorporates innovative safeguards—including a collateral pool, Stability Pool, and liquidation mechanism—to ensure security and stability. However, competitive pressures may arise from protocols offering similar services, such as MakerDAO or Compound. Simultaneously, LUSD faces regulatory scrutiny across jurisdictions—including the U.S. and EU.

Source: Liquity

DLLR: Sovryn’s Sovereign Stablecoin

Sovryn’s stablecoin is called the Sovryn Dollar (DLLR), a Bitcoin-native stablecoin backed by a diversified basket of Bitcoin-based collateral. 1 DLLR aims to maintain a near 1:1 peg to the US dollar, offering a stable medium for payments or savings. DLLR aggregates several Bitcoin-pegged stablecoins—such as ZUSD and DOC—which individually maintain their 1:1 USD peg via distinct algorithms or protocols. By pooling these stablecoins, DLLR achieves enhanced stability, better insulating itself from market volatility and collateral-specific risks. DLLR’s supply is demand-driven: arbitrage opportunities emerge whenever DLLR’s price deviates above or below $1, helping restore equilibrium.

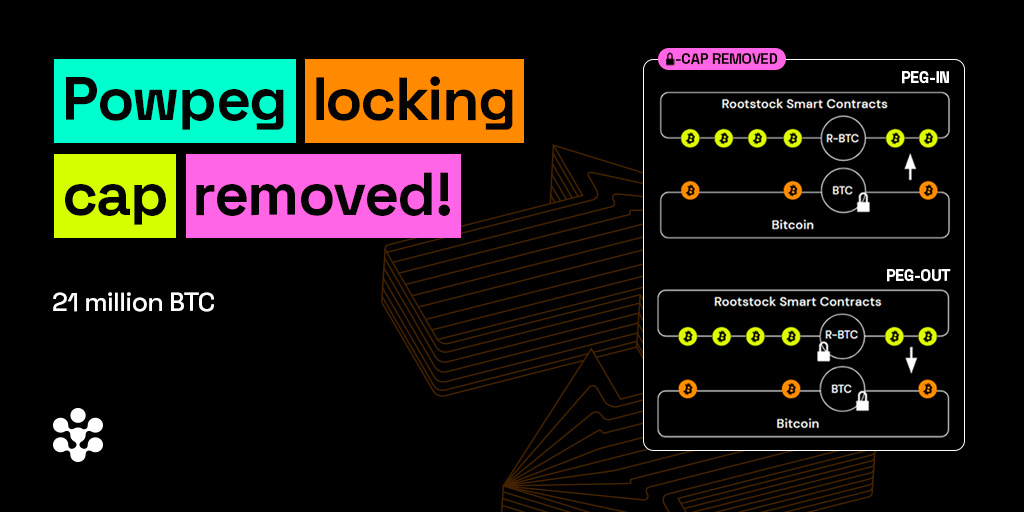

Sovryn is a Bitcoin-based decentralized finance (DeFi) protocol leveraging zero-knowledge proofs to safeguard user privacy. Sovryn enables users to engage in leveraged trading, perpetual contracts, lending, and other DeFi activities—all secured by Bitcoin’s robust security model. All Sovryn services are priced in Bitcoin (BTC) and natively integrated with the Bitcoin network. Its smart contracts run on Rootstock (RSK), a Bitcoin-connected sidechain. Sovryn is among the next generation of permissionless financial applications, supporting cross-chain functionality.

Sovryn deploys EVM-compatible smart contracts on the RSK blockchain and interconnects with Bitcoin and the Lightning Network, Ethereum, and Binance Smart Chain. Most Sovryn features draw inspiration from Ethereum protocols, with parts of its codebase built upon redesigned and audited forks. Rootstock (RSK) is an Ethereum protocol fork—similar to other EVM-compatible blockchains—but uniquely features a two-way peg with Bitcoin and merged mining with the Bitcoin network. Sovryn’s contracts are governed by the Exchequer multisig—a group of anonymous keyholders—except for the Staking and FeeSharingProxy, which can be updated via SOV staker votes. All contract and codebase changes are subject to voting in the Bitocracy DAO, where SOV token stakers hold voting rights.

DLLR’s potential lies in its fully transparent, decentralized, censorship-resistant design—backed exclusively by Bitcoin, with no third-party or central authority involvement or risk. DLLR can accelerate Bitcoin’s circulation and utility, thereby enhancing Bitcoin’s value and real-world adoption. Additionally, DLLR serves as a powerful lending instrument within the Sovryn platform, enabling users to borrow or lend DLLR using BTC as collateral—offering zero-interest borrowing and high yields.

Source: Rootstock

Multi-Asset Backed

sUSD: Synthetix Expands with Synthetic Assets

sUSD is a stablecoin issued by the Synthetix protocol, tracking the USD price via a decentralized oracle network. sUSD is a crypto-native, overcollateralized stablecoin—minted exclusively against Synthetix Network Tokens (SNX). Within the SNX ecosystem, sUSD serves diverse use cases: trading, lending, holding, or swapping for other synthetic assets (Synths), including equities, commodities, and cryptocurrencies.

sUSD’s peg mechanism relies primarily on market-driven arbitrage and supply-demand dynamics. When sUSD trades below $1, arbitrageurs buy sUSD on external exchanges using USD or other stablecoins, then redeem it on Synthetix for other Synths—or use sUSD to borrow SNX or ETH. When sUSD trades above $1, arbitrageurs mint sUSD by staking SNX or ETH on Synthetix, then sell sUSD on external exchanges for USD or other stablecoins. These arbitrage actions adjust sUSD’s supply and demand, pushing its price back toward the $1 peg.

The integration of Atomic Swaps, Curve, and Perp V2 has significantly expanded sUSD’s utility—powered by Synthetix’s multi-chain deployment strategy. In today’s multi-chain era, synthetic assets hold immense promise. Moreover, sUSD’s capital efficiency challenges are expected to be addressed in the upcoming V3 upgrade, which introduces ETH-like collateral types—gradually lowering the required collateral ratio and improving capital utilization. As Synthetix evolves into a “super-app” for synthetic assets, sUSD stands poised to gain backing from increasingly robust real-world assets.

Source: Synthetix

TiUSD: Multi-Asset Reserve

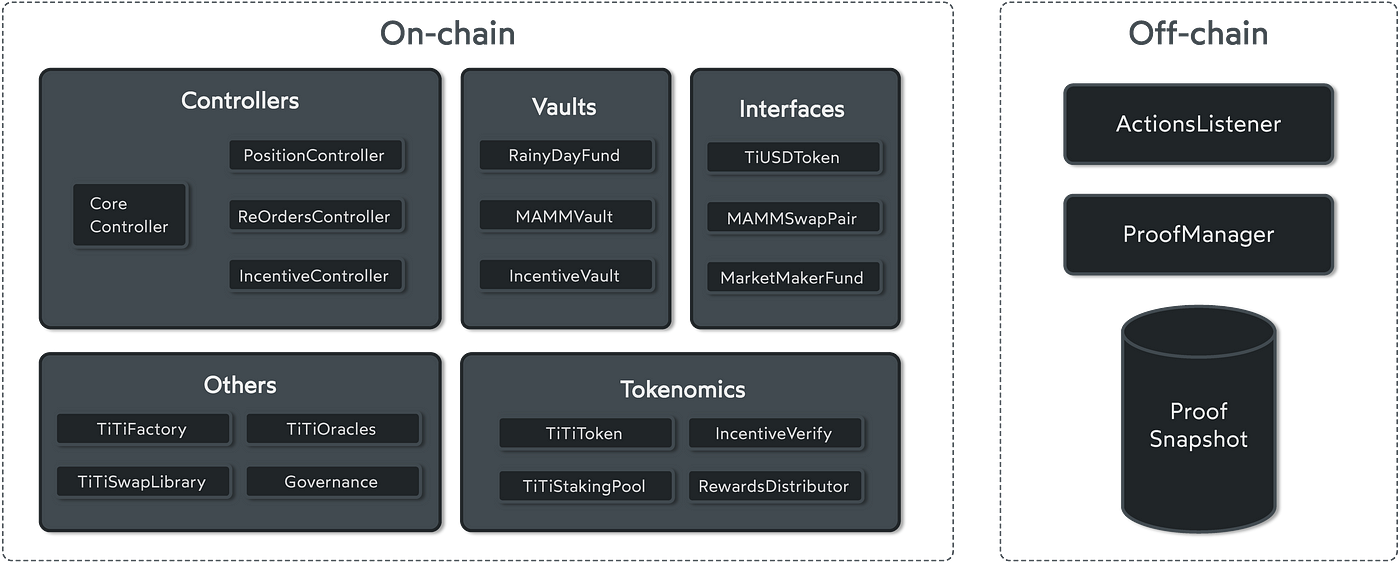

TiUSD is an algorithmic stablecoin issued by TiTi Protocol, tracking the USD price through a decentralized, multi-asset reserve mechanism that combines “use-as-mine” incentives with stability and growth objectives. TiUSD is an elastic-supply stablecoin—its circulating supply automatically adjusts based on market demand and price fluctuations. Its reserve pool comprises multiple crypto assets—including ETH, BTC, and DAI—to enhance diversification and resilience against systemic risks.

TiUSD ensures growth via its decentralized, multi-asset reserve and “use-as-mine” design. Its elastic supply further enables automatic adjustments to market conditions and price deviations—helping maintain a stable ~$1 peg. Key challenges include competition from other algorithmic stablecoins—particularly those with more sophisticated algorithmic designs or governance models, such as MakerDAO and Ampleforth. Additionally, TiUSD must continuously safeguard its reserve pool’s diversity and robustness to prevent under-collateralization or security breaches.

Source: TiTi Protocol

Omnichain Deployed

USD0: Tapioca’s Algorithm

LayerZero is an innovative cross-chain messaging infrastructure enabling secure, direct token transfers across chains—without asset wrapping, intermediary chains, or liquidity pools. Big Bang is a LayerZero-native omnichain money market allowing users to mint USD0, an omnichain stablecoin. It imposes no borrowing limits but enforces a debt ceiling. Collateral accepted for minting USD0 includes native gas tokens (or their staked derivatives), such as ETH, MATIC, AVAX, wstETH, rETH, stMATIC, and sAVAX.

USD0’s peg mechanism is powered by the Tapioca algorithm, which dynamically adjusts the debt ceiling and a tunable stability fee to maintain USD0’s 1:1 peg to the USD. The Tapioca algorithm adapts both parameters in response to changing market conditions and collateral valuations—thereby influencing USD0’s supply and demand. When USD0 trades above $1, Tapioca raises the debt ceiling and lowers the stability fee to incentivize additional minting. When USD0 trades below $1, Tapioca lowers the debt ceiling and raises the stability fee to encourage repayments or purchases of USD0.

Theoretically, USD0 can operate natively on any chain—eliminating wrapping costs and intermediaries. Leveraging LayerZero, USD0 enables seamless cross-chain transfers and swaps, and integrates effortlessly with other LayerZero-native applications like Stargate. However, its primary risks stem from LayerZero’s own protocol security and underlying chain compatibility.

IST: Enabling Cross-Chain Asset Transfers

Inter Protocol’s stablecoin IST is a decentralized stablecoin protocol built on Cosmos, designed to facilitate asset transfers across interoperable ecosystems while maintaining a strict 1:1 USD peg—minimizing price volatility, a core objective of IST. IST can be minted via three mechanisms: the Parity Stability Module, Vaults, and BLD Boost. The Parity Stability Module accepts designated stablecoins (e.g., DAI, USDT, USDC) as collateral; Vaults accept crypto assets as collateral, with varying collateral ratios set by the DAO; and BLD Boost uses BLD tokens as collateral—yielding no node staking rewards but enabling debt repayment.

IST’s stability mechanisms closely mirror those of DAI—including liquidation, dynamic collateral ratio adjustments, debt ceilings, a Reserve Pool for emergency debt reduction, and BLD inflation to repay debt. All mechanisms are governed by fine-grained minting restrictions, enabling a novel, dynamic stablecoin model previously unseen. Inter Protocol is built on Agoric—a Cosmos-based chain supporting JavaScript smart contracts—and its native token is $BLD. IST functions not only as a stablecoin but also as Agoric’s native fee token, delivering critical economic stability and core protocol functionality.

Cosmos, dubbed the “Internet of Blockchains,” connects independent blockchains via the Inter-Blockchain Communication (IBC) protocol—enabling trustless asset transfers and dramatically improving interoperability and scalability. Within the Cosmos ecosystem, stablecoins are a focal point for many projects; IST represents one such solution, delivering a more stable and reliable value-transfer tool for cross-chain ecosystems.

Growing interoperability within the Cosmos ecosystem creates positive spillover effects for Inter Protocol. As more protocols launch using the Cosmos SDK and adopt IBC for cross-chain communication, Inter Protocol gains access to an expanding network of compatible protocols. Bridging via other protocols further extends support to additional chains and enables interactions between supported chains. Increased overall liquidity and broader user adoption significantly benefit Inter Protocol—not only boosting usage of Cosmos-native applications, but also driving wider adoption of the IST stablecoin.

Source: shadeprotocol

Seeking Real-World Anchors

Protocols like Curve are ushering us into the next major paradigm shift in DeFi. Specifically, DeFi protocols are beginning to recognize the need to control stablecoin issuance, liquidity systems, and lending markets. Frax and Aave are following closely behind. As more protocols attempt to solve this “trinity problem,” differentiation will no longer hinge on a protocol’s final business model—but rather on the starting point it uses to reach that end state. Compared to MakerDAO, Curve and Aave possess stronger brand recognition and team capabilities, giving their stablecoins broader development potential.

Currently, demand for stablecoins falls into three main categories: stablecoins used as stores of value, those used for trading and everyday utility, and those preferred by users who wish to avoid fiat-backed stablecoins altogether. Meanwhile, integrating real-world assets (RWAs) into algorithmic stablecoins still faces numerous challenges—including scalability and risk management related to physical assets. Concurrently, many stablecoin projects focus heavily on price stabilization mechanisms and decentralization levels, while overlooking product-market fit—the extent to which their stablecoins are actually adopted and used by end users. This remains a core challenge for many stablecoin initiatives. In summary, the author is most optimistic about the following four directions for algorithmic stablecoin protocols:

Native crypto stablecoin protocols—because Bitcoin and ETH are forming powerful value networks. More importantly, they constitute the foundational trust layer of cryptocurrency, meaning stablecoin projects anchored to these value networks benefit from more robust asset backing. However, key differentiators will be improvements in the user experience layer, the scale of network-locked assets, and the strength of liquidation protection mechanisms;

Stablecoins issued by large-scale “super apps” — essentially bypassing trusted intermediaries and establishing direct minting agreements with their users. In such cases, protocols like Curve, Aave, and Synthetix become “super pawnshops,” enabling users to access customized financial services faster and more seamlessly than in traditional finance. User base size and business innovation determine their ceiling—thus, the author is particularly bullish on Synthetix;

Omni-chain algorithmic stablecoins could achieve true decentralization, cross-chain interoperability, and infinite scalability. They can be freely issued, transferred, and traded across any blockchain, ensuring cross-chain interoperability and portability—and thereby guaranteeing sufficient and comprehensive liquidity. More importantly, omni-chain insurance mechanisms better mitigate liquidity crises during bank runs;

Additionally, delta-neutral stablecoin models may emerge as an important trend in the future. However, implementing such a model requires support from corresponding futures protocols and a sufficiently large futures market—while also demanding careful attention to risk control and market adaptability.

Is there a possibility that one algorithmic stablecoin protocol could combine all the above features? Unfortunately, the author has not yet identified such a project. Algorithmic stablecoins require a robust and reliable algorithmic design capable of maintaining price stability under diverse market conditions—and avoiding extreme outcomes like loss of control or collapse. They also require a broad and loyal user base to sustain their economic model and provide sufficient demand and liquidity. Furthermore, a strong, innovative ecosystem—capable of integrating with both on-chain and off-chain services—is essential to unlock additional use cases and create greater value. At that stage, the diversification of collateral assets becomes comparatively less critical; instead, the author places greater emphasis on the health of the underlying value network and the pegged asset.

The rise of algorithmic stablecoins follows its own internal logic and context—but this does not mean they can fully replace centralized stablecoins, especially at scale. Therefore, algorithmic stablecoins may need to pursue safer, more efficient, and scalable solutions. Moreover, USD-pegged stablecoins like USDC still dominate today’s market, thanks to their issuers’ regulatory compliance and economic strength—which offer users more reliable guarantees. For users seeking to avoid legal oversight and centralization risks, algorithmic stablecoins remain a valuable alternative. Nevertheless, we must acknowledge their limitations—and actively explore more innovative solutions to advance the entire DeFi industry.