By: Checkmate

Translation: LH

Source: Lanhu Notes

The Ethereum project has long faced criticism—particularly from Bitcoin enthusiasts—across multiple dimensions, including design, execution, and failure to deliver the product promised during its crowdfunding campaign. Ethereum is currently attempting an enormous engineering challenge: rebuilding the entire blockchain to integrate existing chains while keeping both chains running in real time.

This is not easy. It highlights undeniable flaws in the original design and perpetuates ongoing uncertainty for investors about the future.

Meanwhile, Ethereum has found a new direction—focusing on decentralized finance (DeFi) applications. This is supported by what’s often called the “moat” of developer activity. The underlying ethos of this movement is “open and unstoppable finance,” establishing ETH as the reserve monetary asset across the entire ecosystem.

This article, however, argues a different position: despite these developments, the ETH token is unlikely to develop a credible monetary premium. This becomes especially critical when ETH competes against digital currencies with fixed supply, deterministic issuance schedules, and deep liquidity—such as Bitcoin. The core arguments revolve around the following themes:

Uncertainty surrounding monetary policy and centralized governance

Second-system syndrome and persistent shifts in project direction

Reliance on the application layer for value accrual

Underestimating the “tortoise-and-hare race” reality of Bitcoin’s development

(Lanhu Notes: Second-system syndrome—or second-system effect—was coined by Fred Brooks, author of *The Mythical Man-Month*. It describes how, after successfully building a small, elegant system, designers tend to over-engineer the next one—adding excessive features and complexity—often resulting in failure.)

Monetary Policy and Governance

Bitcoin’s core monetary-policy design is hardcoded into its software from inception, featuring a pre-defined supply schedule capped at 21 million coins. Historically, Bitcoin’s monetary policy has changed only once—via BIP-42 soft fork—to remove undefined behavior in Satoshi’s C++ implementation and enable development of alternative clients.

Today, this monetary policy is safeguarded by a robust social contract. Altering Bitcoin’s monetary policy would require either undermining the project’s foundational values or executing a hard fork of the chain—both highly improbable. Most Bitcoin supporters agree that tampering with the supply schedule would render it no longer Bitcoin.

This provides investors with relative certainty—and has attracted impressive value capture over Bitcoin’s 11-year history. Bitcoin’s design instills confidence in future inflation and supply expectations.

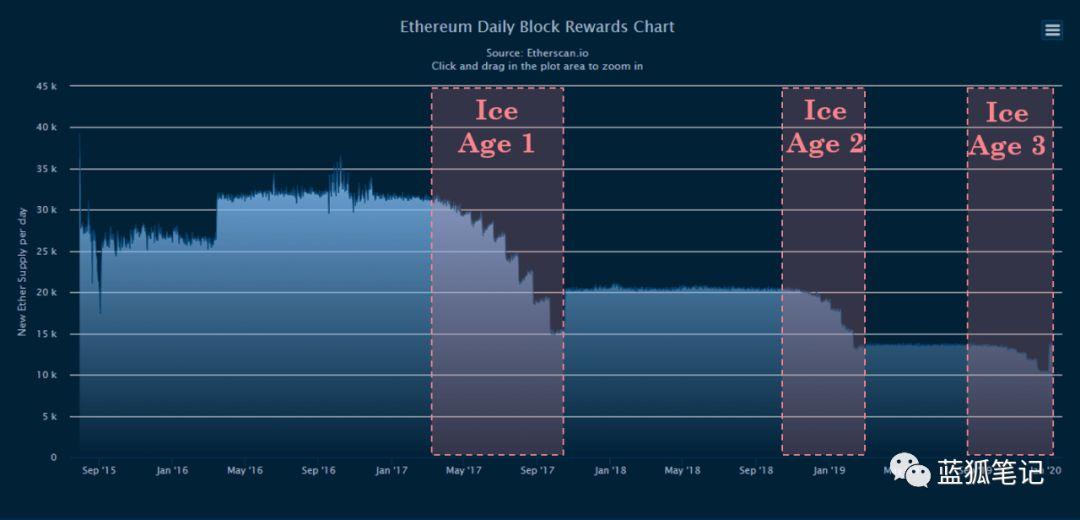

Ethereum’s 2014 crowdfunding occurred under the explicit understanding that the network would eventually transition to Proof-of-Stake (PoS). To incentivize developers toward that goal, the “Ice Age” mechanism was embedded in the protocol—intentionally increasing block times by escalating PoW difficulty. This discouraged miner support for the PoW chain, easing the eventual shift to PoS.

Recently, the Ice Age has been delayed for the third time in Ethereum’s history—each delay requiring a hard fork to modify consensus rules. In every case, PoS implementation was not yet ready for deployment, and the first two delays were bundled with reductions in ETH issuance rates.

Unstable Monetary Policy

Bullish ETH proponents often cite the continuous reduction in block rewards as evidence of increasing monetary hardness and scarcity. However, a clear distinction must be drawn between issuance rate (hardness) and monetary robustness—or resistance to human manipulation.

Although the issuance rate has declined thus far, the choice of inflation rate stems from developer intervention—not deterministic, reliable code-level changes.

The critique here is that a small group holds authority to set the inflation rate for an asset intended to function as a global monetary asset. Given enough time playing this game, those in control will inevitably abuse that power.

Future inflation rates and token supply remain unknown. Even under ETH 2.0, who decides what constitutes “success” at the minimum viable issuance level? Someone will retain authority to adjust staking rates until reaching subjective, dynamic targets. If left to algorithms—and vulnerabilities are discovered—someone will intervene in the protocol to alter inflation. As attack vectors continuously evolve, this process will never cease. Thus, Ethereum can only be considered to have an unstable monetary policy, with its social contract delegating monetary authority to a small collective.

Centralization of Nodes and Validators

Bitcoin experienced its most contentious period during the scalability war over SegWit activation. The UASF (User-Activated Soft Fork) movement rendered miner capture of the Bitcoin chain ineffective via social consensus: users upgraded their nodes so miners violating the new rules received no valid rewards.

To achieve this, Bitcoin node software has always been designed to be lightweight—ensuring minimal hardware requirements and broad public accessibility. Historically, Ethereum required more sophisticated, high-performance hardware to run a node—a consequence of larger transaction volumes and Turing-complete demands on block space.

Although node hardware will continue to be optimized, sync times and hardware requirements will only increase. If Ethereum truly reaches global adoption, this may lead to node centralization—where large participants, capable of frequently upgrading SSDs and hardware, dominate. Node operators will likely concentrate among Ethereum core developers (e.g., EF and ConsenSys), exchanges, crypto banks, and staking service providers.

Due to limited technical capacity, ordinary users will gravitate toward exchanges and staking services for convenience—effectively reinforcing centralization under ETH 2.0’s slashing mechanisms.

As this centralization takes hold, users’ ability to signal intent and mount UASF-style defenses against malicious actors will be severely diminished.

This underscores a gradual concentration of governance authority toward core developers—who hold substantial ETH for PoS validation and influence the direction of monetary policy experiments.

Monetary Experiments

Discussions around monetary policy include the latest experiment—EIP-1559—which introduces an ETH burning mechanism, fundamentally altering the blockchain’s mechanics and incentive structure.

Ultimately, this burning mechanism benefits current ETH holders most, while disadvantaging future holders and users. Assuming network growth, the ETH burn rate increases users’ dollar-denominated gas costs (fee inflation). Stakers remain largely unaffected, benefiting from non-dilutive block rewards and taxation via burning.

The author worries this monetary experiment was carefully engineered by those who stand to gain most—responding to developers’ “research predictions” that the current gas fee mechanism fails to accrue value. This resembles central bank experimentation and the Cantillon Effect today. (Lanhu Notes: The Cantillon Effect describes how newly created money does not affect all prices simultaneously or equally. Its impact depends on how and where new money enters the economy—benefiting early recipients while disadvantaging later ones.)

One can only conclude that Ethereum’s monetary policy remains relatively flexible—shaped by people rather than code. This uncertainty reflects an unstable monetary policy (susceptible to human intervention) and legitimizes centralized governance. Unquestionably, this impedes Ethereum’s development of a monetary premium—and appears poised to worsen over time.

Second-System Syndrome

The Ethereum project was originally designed to extend Bitcoin’s functionality by introducing Turing-complete scripting capabilities. Its design intent was to create a global computing network—the so-called “world computer.” In practice, this was a valid design goal, and Ethereum is well-suited for it—providing, in effect, the CAPTCHA for the new transactional internet.

This design decision entails trade-offs: increased protocol complexity, a larger attack surface and greater vulnerability to exploits, and inevitable blockchain bloat. Ethereum’s design direction has also responded to market demand, undergoing several pivots—from the “world computer” narrative to unstoppable dApps, then to token issuance, and now to open financial applications.

Notably, the original Ethereum design explicitly excluded ETH as a monetary asset. This was later revised on Ethereum.org and in its official documentation.

While this reflects innovation and lessons learned, Ethereum’s design trajectory reveals a persistent gravitational pull toward Bitcoin’s design—and its role as a monetary asset. Meanwhile, Bitcoin has consistently built monetary properties such as liquidity, network effects, and—ultimately—financial products that drive strong reputation and product-market fit.

Ethereum is, in many respects, a textbook example of second-system syndrome: a simple technology like Bitcoin is deemed insufficient for its design goals, prompting iteration into a more complex and ostensibly “promising” project—leading inevitably to endless research cycles, discovery of new problems, and delayed delivery timelines.

With ETH 2.0’s rebuild positioned as the latest solution to this problem, it again paints an uncertain future for ETH holders. This new blockchain will effectively reset the Lindy effect that had developed on the existing chain; meanwhile, it is reasonable to expect further research and the discovery of yet more issues requiring resolution. (Blue Fox Notes: The Lindy effect refers to non-perishable entities—unlike biological organisms—which tend to have longer expected lifespans the longer they have already existed. Examples include classic books and cryptocurrencies. Here, the author argues that ETH 2.0, as a new blockchain, resets Ethereum’s accumulated Lindy effect and introduces new challenges.)

Moreover, the ETH 2.0 Beacon Chain is architecturally very similar to Bitcoin—handling only consensus and global state, while pushing application logic and bloat onto shards (in Bitcoin’s case, sidechains or Layer 2 solutions).

Relying on the Application Layer for Value Accrual

Although the open finance ecosystem has achieved remarkable success in technology and engineering, it remains exposed to risks stemming from dependence on third-party protocols for ETH’s value accrual.

Recently, numerous high-profile “unstoppable,” “non-custodial,” and “decentralized” applications… are, in fact… stoppable, custodial, and centralized:

* MakerDAO features a zero-delay liquidation mechanism, and user funds are custodial.

* Compound Finance was found to be custodial, with developer backdoors and liquidation mechanisms.

* After a bug was discovered in the 0x V2 upgrade, developers shut down 0x.

These developments challenge the “unstoppable” narrative—and represent, in effect, dishonest product-market messaging: claiming “decentralization” while retaining backdoored custodianship. Although security safeguards are effective during early R&D phases, this sounds strikingly like second-system syndrome—perpetual research supporting development timelines perpetually described as “almost ready.”

Cryptography has no secure backdoor. If developers can access it, attackers likely can too.

Reliance on Centralized Oracles

At the core of the DeFi ecosystem lies MakerDAO, governed by the MKR governance token. One might argue that without Maker and its issued DAI/SAI stablecoins, the DeFi ecosystem would depend entirely on permissioned, centralized stablecoin infrastructure—such as USDT and USDC. Furthermore, the vast majority of the ecosystem relies on Maker’s centrally controlled ETH/USD price oracle.

Solving this issue in a trustless manner is not straightforward. Indeed, this article does not consider trustless oracles a solvable problem in the medium term—and emphasizes that this topic has been researched for decades. Any on-chain price feed (e.g., Uniswap) remains vulnerable to liquidity attacks and would require such massive scale that realization remains unlikely for at least several decades. (Blue Fox Notes: This claim is overly subjective.)

Thus, trustless oracles—the critical component of DeFi—are likely to remain centralized for decades. In the foreseeable future, attacks against these centralized oracles will constitute a fundamental risk to investor capital. Describing DeFi as a “house of cards” is highly appropriate: these centralized oracles serve as primitives for other composable protocols. The entire stack’s resilience is only as strong as its weakest link—obscuring users’ true risk exposure.

This appears to be a source of systemic risk—one that cannot be meaningfully mitigated.

Dependence on MakerDAO

A primary criticism of MKR is its extreme concentration among prominent venture capitalists and the core team. Indeed, a recent proposal to reduce the “decentralized” bank rate by 4% received 94% of its votes from a single entity—revealing voter apathy, insufficient participation incentives, and outsized influence wielded by a small cohort of large token holders.

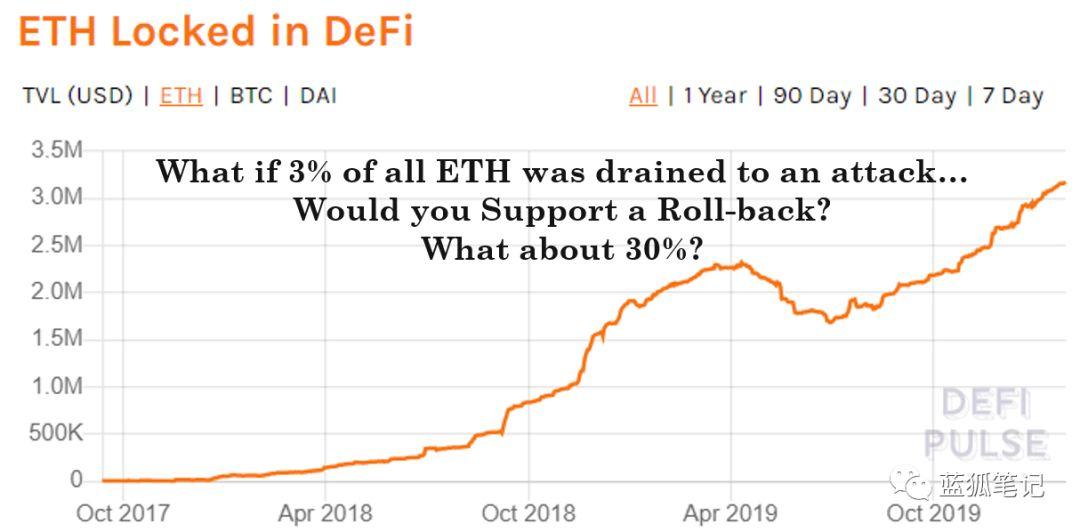

Now, considering the entire open finance ecosystem’s heavy reliance on Maker’s centralized oracle, one must ask: what happens if Maker—or its token holders—is regulated or hacked? Since base-layer forks can restore operations, Maker could only be temporarily disabled. But what cost would ETH holders bear?

A hack targeting the MakerDAO oracle could trigger CDP/treasury liquidations—and all dependent protocols would allow savvy attackers to capture cheaply liquidated ETH.

If 3% of all ETH were stolen in such an attack, would a chain rollback even be on the table? What if it were 30%? The attacker would instantly become the largest validator on the PoS network. (Blue Fox Notes: “3%” here refers to the current amount of ETH locked in DeFi.)

This is a genuine risk—whose consequences remain unclear.

If ETH locking—designed to underpin the value proposition of open finance—is undermined, then all associated value accrual in this scenario can reasonably be expected to collapse. Bullish ETH proponents argue that native protocol smart contracts can be forked by third parties. This is true—but this article questions how many iterations of the new narrative—> boom—> regulation/hack/fraudulent promises—> bust investors will tolerate before future value accrual is callously eroded.

The Tortoise Wins the Race

In summary, the Ethereum project is affected by the following factors:

Signs of relatively centralized governance and an unstable monetary policy—trends that appear likely to worsen over time.

The latest EIP-1559 experiment appears contradictory to the needs of all users except current ETH holders. This creates an unfair system and, due to rising fees, makes on-chain user transactions increasingly unattractive.

A significantly larger attack surface compared to Bitcoin—due to protocol complexity, Turing completeness, developer backdoors, and centralized oracles.

Continuously shifting narratives, project directions, and experimental features—gradually converging toward Bitcoin’s robust monetary narrative.

Over-reliance on third-party applications to increase ETH’s token value—applications that can be stopped. An unlimited supply monetary policy and liquidity requirements necessitate this mechanism.

Ongoing threats to any centralized ETH pools—including custodial DeFi applications—undermining PoS validators.

The peak manifestation of second-system syndrome: a complete rebuild of the foundational blockchain. Rolling one chain into another is a monumental undertaking—requiring years to complete.

Ultimately, the reason Ethereum struggles to develop—and sustain a long-term, compelling monetary premium—is simple.

Investors cannot determine what they are buying; systemic risks and unmitigable risks are embedded in the social contract, and there is no tangible data indicating this reality will change.

One cannot reasonably expect potential investors—who recognize the scale, history, and depth of the aforementioned uncertainty—to willingly exchange part of their capital for ETH tokens.

The original vision of Ethereum as “the world computer” remains the strongest project narrative—if direction were not subject to endless changes, it would be an achievable goal. The problem is that, compared to “monetary assets” like BTC, the “world computer” outcome targets a smaller addressable market. Consequently, its narrative has gradually shifted toward “ETH is money.”

Bitcoin is realizing its goal of becoming a digital, robust, immutable currency, while Ethereum has explored countless dead ends. There is widespread misunderstanding regarding the potential of systems such as the Lightning Network, sidechains, and various higher-layer solutions—systems capable of enhancing Bitcoin’s capacity as a global reserve asset.

This article posits that, should Bitcoin achieve global monetary status, most users will rarely interact directly on-chain due to high fees. Ordinary users will primarily interact at higher layers of the technology stack, while final settlement remains the primary function of the base layer.

Intuitively, it makes sense to build an extremely secure and immutable base layer whose sole purpose is transaction settlement. More complex layers require less security and consensus, and these should be isolated to higher levels of the stack.

Indeed, this is precisely the design objective of the ETH2.0 Beacon Chain—it handles only finality and settlement, with no bloated blocks. The ETH2.0 shards merely replicate Bitcoin’s second-layer, third-layer, and higher-layer solutions—but without Bitcoin’s existing liquidity, reputation, and security premium, all of which continue to grow.