As populism and trade protectionism rise, blockchain and cryptocurrency technologies are increasingly becoming critical strategic tools in geopolitical competition among major powers.

What role will Bitcoin play in future geopolitical contests?

Optimists argue it will become the foundational anchor for fiat currency valuation in the future, while pessimists contend it serves no purpose beyond speculation. Even if we classify Bitcoin solely as a commodity, the issue of price-setting power remains unavoidable.

Susan Strange, one of the founding scholars of International Political Economy, introduced the concept of “structural power” in her book *States and Markets*. She posits that two types of power exist in the international system: relational power and structural power.

The former can be understood as coercing others—using force—to do something they otherwise would not do. The latter refers to the ability of a power holder to establish global standards, thereby persuading others “rationally” to voluntarily act in ways that serve the interests of the power holder.

Professor Strange considers structural power more important, since brute force cannot resolve all issues—and achieving victory without battle is the supreme strategy.

She further subdivides structural power into four structures: production structure, security structure, financial structure, and knowledge structure.

From this perspective, whoever controls structural power also controls Bitcoin’s price-setting authority. Thus, although Bitcoin itself is borderless, its price-setting power is inherently national.

Today, using this analytical framework, we examine who holds Bitcoin’s structural power.

Production Structure

The production structure examines production relations—i.e., who decides what to produce, how to produce it, for whom to produce, by what methods, and under what conditions.

First, let’s identify Bitcoin’s supply-side participants.

From a pricing standpoint, suppliers fall into two categories: suppliers of newly minted coins and suppliers of existing (held) coins.

Newly minted Bitcoin comes from miners, whereas holders of existing Bitcoin—the so-called Hodlers—constitute the supply side of the存量 (existing) coin pool. As more Bitcoin is mined over time, miners’ influence on Bitcoin’s price gradually diminishes, while Hodlers’ influence grows correspondingly.

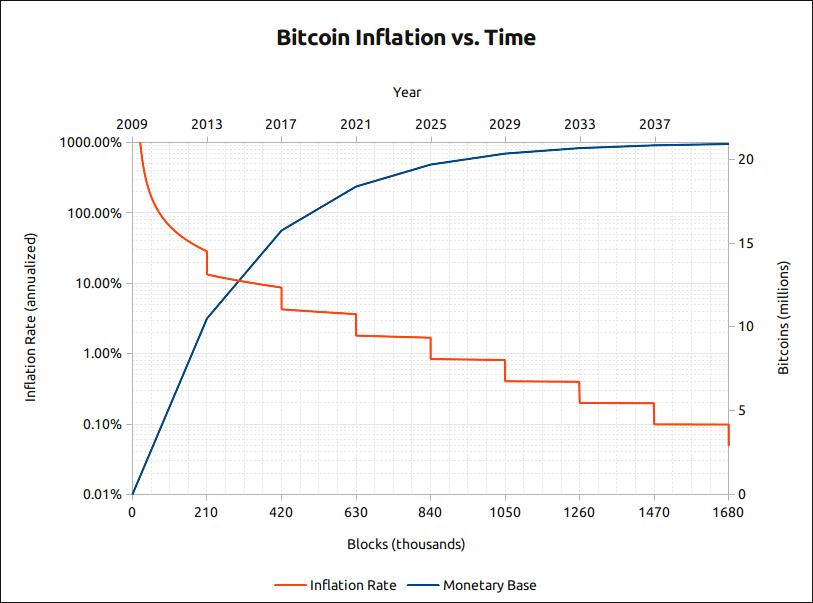

Bitcoin’s inflation chart over time

Let’s first examine incremental supply. As shown in the chart above, Bitcoin’s current circulating supply stands at approximately 18 million BTC, with an inflation rate of roughly 4%. After next year’s halving event, this rate will drop to just 1.8%. Prior to the 2016 halving, Bitcoin’s inflation rate exceeded 8%.

This implies that in Bitcoin’s early years, miners could easily influence its price through coordinated actions—such as collectively hoarding or dumping coins. Today, however, even though China still dominates mining hashrate (according to a recent report by The Next Web, China commands two-thirds of global hashrate, with 54% concentrated in Sichuan Province), its impact on Bitcoin’s price—beyond ensuring network security—has significantly weakened.

A rough estimate of Bitcoin mining’s market ceiling: fewer than 3 million BTC remain to be mined. Assuming Bitcoin’s price stabilizes at $7,500, the total value of remaining coins is approximately $22.5 billion. If electricity costs account for 50% of mining expenses, the industry’s total market ceiling is around $11.25 billion.

Canaan Creative, a classic “pick-and-shovel” company, was valued at $1.4 billion at its IPO but has since halved to $750 million. Meanwhile, industry leader Bitmain reportedly saw its valuation slashed from $15 billion to $5 billion, according to mid-year news reports.

Even so, the combined valuations of the top two “pick-and-shovel” companies already reach $5.75 billion. While selling picks and shovels is often profitable, when shovel production reaches half the value of the gold itself, the sustainability of this business model becomes highly questionable. The central challenge is no longer about building “better shovels”—but rather, whether the “gold” will appreciate in value.

This resembles recent headlines declaring the “hardest-ever postgraduate entrance exam year”: everyone knows the economy has entered an L-shaped bottom, and future employment prospects look bleak (akin to Bitcoin’s halving). Consequently, students collectively opt to take the exam, pushing this year’s applicant count to a record 3.4 million—a doubling within five years (mirroring rising hashrate). This surge has dramatically increased exam difficulty (equivalent to rising mining difficulty). Yet tutoring institutions continue marketing aggressively: “No worries—we’ll launch even more advanced prep courses, plus money-back guarantees if you fail. Enroll now!” (i.e., buy new mining rigs).

Now consider the supply side of existing coins—Hodlers, or Hodlers who defect at critical moments. Indeed, Bitcoin’s price trajectory following the PlusToken hack clearly shows that insufficient demand absorption for existing sell-side pressure has become the primary driver of market declines.

Setting aside short-term factors like hacker theft, rapid price appreciation triggers mass selling of long-held Bitcoin from wallets to exchanges, which constitutes the main cause of subsequent price corrections.

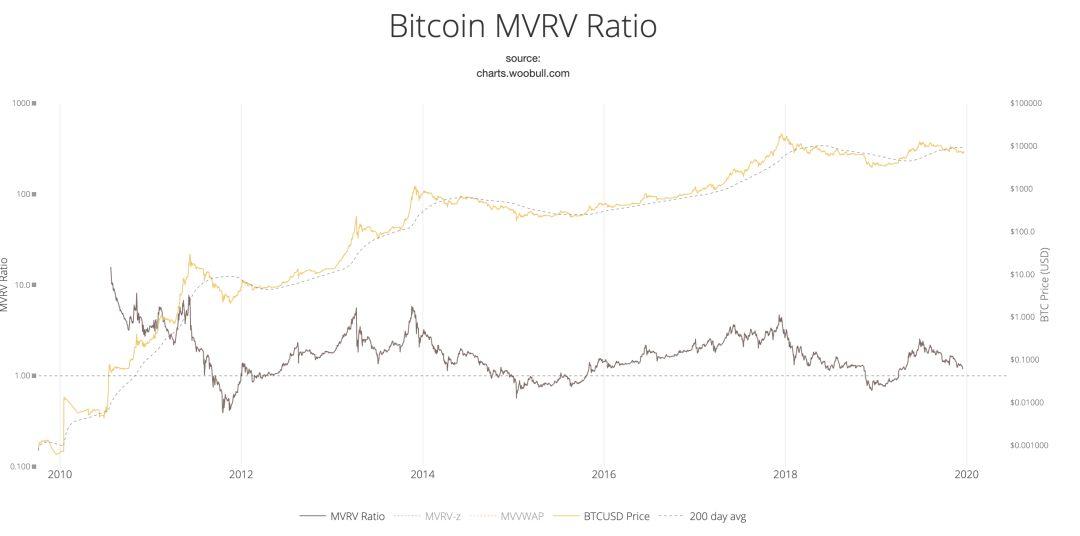

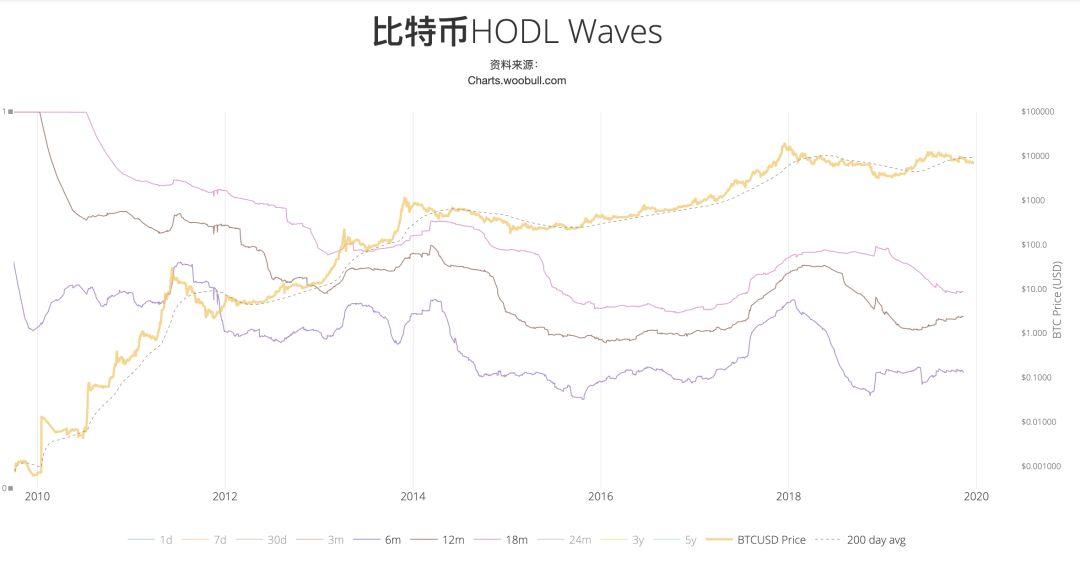

This trend is clearly visible in both the MVRV ratio and HODL Waves metrics:

Both charts above illustrate capital flowing out of wallets into markets during Bitcoin’s price peaks—i.e., profit-taking.

Turning to demand, it broadly falls into two categories: payment demand (cross-border, anonymous gray-market use cases) and store-of-value demand (Hodlers).

Cross-border settlement demand gives Bitcoin a short-term advantage, but in the long term, it may be displaced by stablecoins and central bank digital currencies (CBDCs).

Anonymous gray-market payment demand was largely quantifiable near Bitcoin’s 2015 price bottom—and proves insufficient to sustain higher market capitalization. Moreover, newer privacy-focused cryptocurrencies offer comparable anonymity and can readily fulfill this function.

Store-of-value demand forms the core pillar supporting Bitcoin’s long-term strength—commonly referred to as “faith.” Though interpretations of this “faith” vary, the underlying logic generally holds that Bitcoin will serve as a neutral third-party asset—partially augmenting gold’s role—as a hedge amid prolonged negative real interest rates.

To quantitatively assess the above demand, different models—such as the NVT Ratio (for payment use cases) and the Stock-to-Flow (S2F) model (for value storage)—are employed to guide short-term decisions on whether demand-side participants should continue holding (HODLing) or defect to the supply side.

Overall, in terms of production structure, Bitcoin is far simpler than commodities; in the short term, it is a博弈 (strategic contest) over chips (i.e., circulating supply), where miners’ marginal supply influence is gradually diminishing and is jointly shaped by security structure, financial structure, and knowledge structure. In the long term, Bitcoin’s trajectory hinges on the verification or falsification of collective belief—most significantly influenced by knowledge structure.

Security Structure

In international political economy, “security structure” refers to “a power framework formed when some actors provide security defense for others.” Those providing security protection naturally acquire certain privileges.

For example, during oil transportation, the Strait of Hormuz—the sole maritime passage in and out of the Persian Gulf—grants Iran strategic maneuvering space within the Gulf region and significant leverage in its standoff with the United States once it threatens to close the strait.

Although Bitcoin was designed to be decentralized and permissionless, its gradual integration into the mainstream has subjected it to certain constraints imposed by security structures. Its security structure primarily stems from two aspects:

First, security assurance for mining production.

While mining hashpower is distributed, mining farms have evolved over time into capital-intensive enterprises. Thus, beyond low electricity costs, a stable, reliable, and secure operating environment is critical for mining operations.

Many Chinese miners remain hesitant to relocate to Iran despite its low electricity tariffs—precisely due to concerns over operational security.

Second, compliance and security assurance for fiat on-ramps and trading.

Free, safe, and legally recognized conversion between Bitcoin and fiat currencies—and legal protection under fiat-based jurisdictions—is currently a necessary condition for broader adoption. Countries that adopt more open regulatory stances gain de facto authority to regulate under the banner of openness, thereby securing structural power advantages in security architecture.

Although China no longer strictly bans mining operations—and retains a substantial share of global hashpower—it still maintains a suppressive stance toward fiat on-ramps and trading channels, at least in the foreseeable future. In contrast, Western countries—including the U.S. and EU—are markedly more open and inclusive, having introduced comprehensive regulatory and tax frameworks to formalize and legitimize crypto activities.

In summary, this will profoundly shape Bitcoin’s production, pricing venues, and the composition of pricing agents over the long term.

Financial Structure

Financial structure is defined as “the sum total of all arrangements governing credit availability and all factors determining exchange conditions among national currencies.”

The penetration of financial capital into Bitcoin’s price-setting authority can be divided into two dimensions: capital and market instruments.

From an industrial capital perspective, upstream mining companies are predominantly controlled by Chinese shareholders: Canaan Creative’s management holds 50.8% of shares, while Bitmain’s Jihan Wu and Micree Zhan collectively hold 83.9%, according to publicly available information.

However, as noted earlier in the discussion of production structure, mining currently—and increasingly in the future—exerts greater influence on Bitcoin’s network security than on its price discovery.

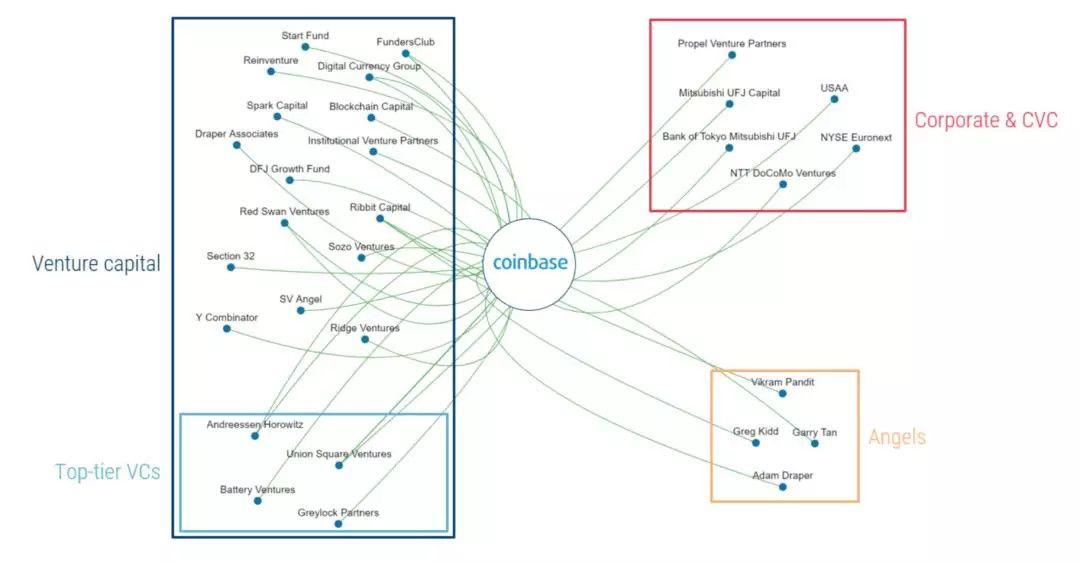

At the exchange level, Coinbase—the most influential exchange—has a diversified shareholder base, including prominent venture firms Union Square Ventures and Andreessen Horowitz, major institutional investors such as the New York Stock Exchange and USAA Financial Services Group, as well as Japanese financial institutions Mitsubishi UFJ Financial Group and telecom giant NTT DoCoMo.

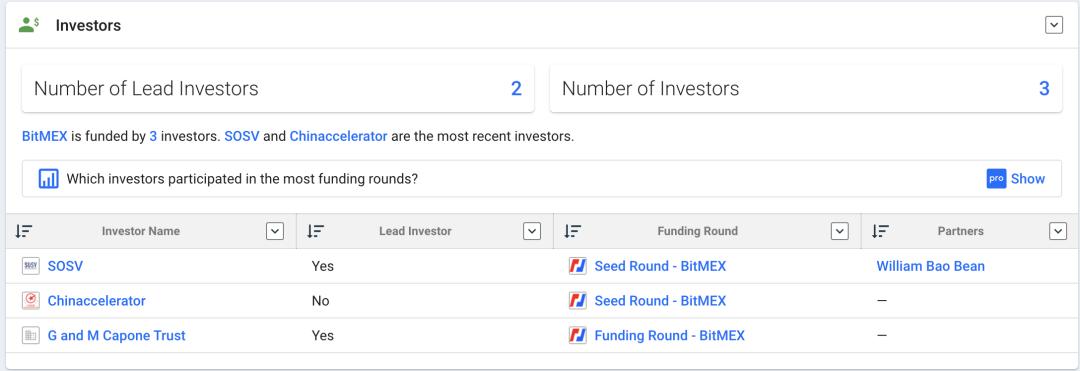

The largest futures exchange, BitMEX, lacks transparency; however, per Crunchbase data, its early investors included SOSV, Chinaccelerator, and G and M Capone Trust.

Among peer-to-peer (P2P) cryptocurrency exchanges, the top three are either Chinese-owned or founded by ethnic Chinese entrepreneurs, accounting for a dominant share of global spot trading volume. However, their direct dependence on stablecoins—and indirect reliance on fiat currencies—places them in a structurally passive position regarding price-setting authority. Repeated USDT-related crises have repeatedly cast a shadow of uncertainty over P2P trading pairs, resulting in a mismatch between trading volume and actual influence.

Moreover, exchanges expand vertically across the ecosystem—from custody wallets and asset management to compliance services, fiat OTC desks, and startup incubators—using themselves as central nodes.

From the perspective of market instruments, historical experience with commodities shows that a mature and well-developed futures market better fulfills functions of price discovery and hedging, leading governments and markets worldwide to widely accept futures markets as the primary pricing centers for commodities—and futures prices as the principal benchmark for commodity valuations.

Unsurprisingly, the U.S. has aggressively seized this high ground in Bitcoin’s case.

In 2017, CME launched cash-settled Bitcoin futures contracts;

In September 2019, Bakkt—a regulated, physically delivered futures exchange—launched boldly. Since inception, Bakkt’s futures trading volume has repeatedly hit new highs.

On December 18, it set a record high of 6,162 BTC. Additionally, Bakkt launched monthly options contracts on December 9.

Furthermore, mainstream futures exchanges—including BitMEX—anchor their Bitcoin futures pricing to indices derived from three major USD-based exchanges: Coinbase, Kraken, and Bitstamp—and retain full authority over index construction and interpretation.

From this vantage point, the U.S. dollar already holds absolute dominance over Bitcoin within the financial structure.

In summary, in terms of financial structure, Europe and the U.S. continue to wield structural power—leveraging decades of experience in commodity pricing—to dominate Bitcoin’s trading and derivatives pricing. While China controls both hashpower dominance and leadership among P2P exchanges, upstream mining alone cannot sustain systemic influence, and P2P exchanges remain dominated by speculative investors—resulting in disproportionate trading volumes relative to real-world influence.

Knowledge Structure

Refers to “a framework encompassing beliefs (and the derived moral values and standards), knowledge and understanding, as well as the channels through which beliefs, ideas, and knowledge are transmitted.” This concept is analogous to Joseph Nye’s notion of “soft power.”

As an emerging alternative asset, Bitcoin currently lacks a universally accepted valuation model.

Yet upon reflection, commonly cited valuation models—including the NVT Ratio (Willy Woo), the MVRV Ratio (Murad Mahmudov & David Puell), and the recently popularized Stock-to-Flow (S2F) model (Plan B)—were all first proposed by Western KOLs or investment institutions and subsequently introduced into China.

Although these models are not always effective, under certain market conditions—where positive feedback validates their utility—they subtly shape our behavior: guiding us on which metrics to prioritize, what algorithms to apply, how to derive valuations, and ultimately when to buy or sell.

Much like the concept of “Inception” in the film *Inception*, both subconscious and conscious cognition drive our behavioral patterns.

These “Western economic frameworks” are continuously embedded into our consciousness, granting their proponents structural authority over knowledge—and thereby translating into real-world influence.

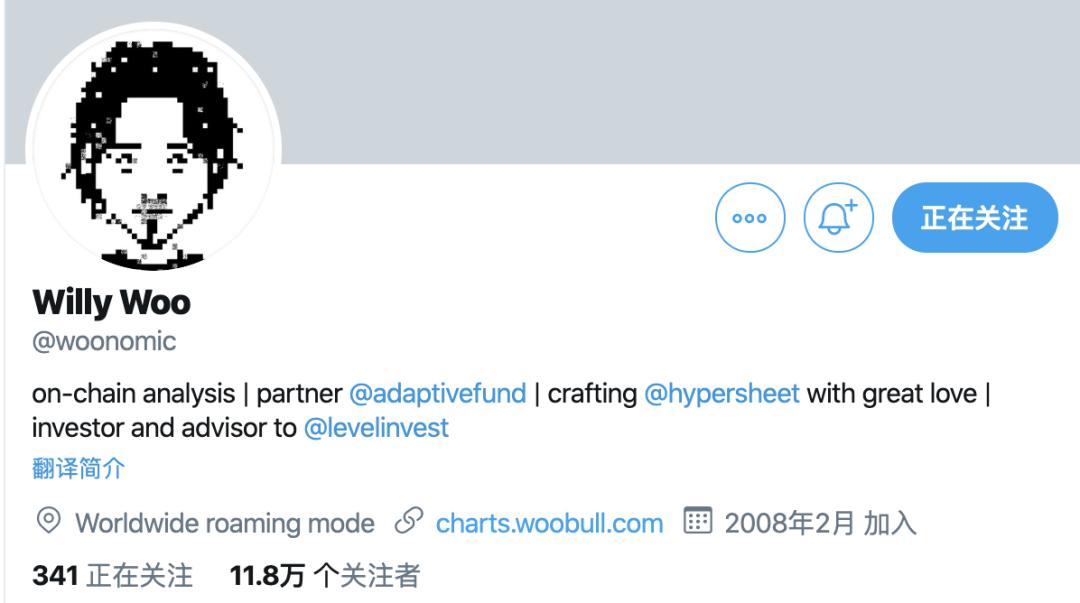

Moreover, Willy Woo—a KOL specializing in developing various indicator models—has amassed 118,000 followers on Twitter, making his platform a critical entry point and distribution channel for these innovative theoretical models.

(Willy Woo and His Indicators)

In terms of knowledge structure, we largely remain passive recipients and improvers. Even when innovations do emerge from China, they struggle to achieve global impact. Frankly speaking, much work remains to be done.

Summary: Under Bitcoin’s current production structure, the four structural forces are deeply interlinked and inseparable. Bitcoin’s pricing power is a composite outcome arising from the convergence of these forces. China’s supply-side advantages within the production structure continue to deteriorate, while the West—across security structures (legal and regulatory frameworks), financial structures (financial capital, market instruments, and theories), knowledge structures (valuation models), and dissemination channels—has already established a multi-dimensional, systemic advantage. As a result, the West has firmly seized Bitcoin’s pricing power—a dominance unlikely to be challenged in the foreseeable future.

How Should China Respond?

Addressing this question requires breaking it down into two sub-questions:

First, is it necessary to contest Bitcoin’s pricing power?

Second, if so, how can China effectively compete for it under current circumstances?

Is It Necessary to Contest Bitcoin’s Pricing Power?

Yes—it is necessary, but not urgent, nor can it be rushed.

Amid renewed global quantitative easing (QE) and widespread negative interest rates, debt levels have surged, placing unprecedented strain on the fiat currency system. Countries worldwide are stockpiling gold. While Bitcoin—an already consensus-backed digital scarcity asset—remains far from becoming a widely accepted value anchor, such a possibility cannot be ruled out entirely. And precisely because it remains possible, contesting its pricing power is necessary.

However, that prospect remains distant, with many uncertainties still at play. First-mover advantage does not guarantee long-term sustainability. Moreover, amid intensifying global efforts to promote central bank digital currencies (CBDCs), Bitcoin’s pricing power is hardly the primary concern. Furthermore, drawing lessons from the Shanghai Stock Exchange 50 ETF futures experience: although Singapore’s FTSE China A50 futures initially held pricing power over the SSE 50 Index due to its first-mover advantage, research shows that once the SSE 50 ETF futures launched, they rapidly reclaimed pricing authority from the FTSE A50. Thus, even delayed entry need not cause undue urgency.

Additionally, even in traditional commodity markets—where China is the world’s largest consumer—we have only recently begun gaining meaningful voice in price-setting. Competing head-on with Western “old money” in the nascent Bitcoin arena is unrealistic—and therefore, cannot be rushed.

That said, leaving room for strategic positioning today remains prudent, for example:

Regulatory Compliance for Related Physical Industries: For instance, taxing Bitcoin mining operations—as previously discussed—while strictly prohibiting such activities domestically, China could open regulated exchanges and derivatives markets in more open jurisdictions like Hong Kong or Macau, creating a legal gateway to accommodate part of the investment and speculative demand.

Beyond the official digital currency (e-CNY), another opening could involve permitting a renminbi-denominated stablecoin.

Financial Trading Testbed: As China gradually opens up its options and other derivatives markets—yet still lacks practical experience—the 24/7 nature of cryptocurrency trading offers an ideal environment to rapidly accumulate hands-on expertise and train professional trading teams.

At the level of knowledge structure, China must not only absorb external ideas but also actively export its own intellectual contributions.

References:

*States and Markets* (Susan Strange)

*Global Commodity Pricing Mechanisms: Four Types of Power Control the Lifeline of “Pricing Authority”* (Huang He, Xie Wei, Ren Xiang)

*Bitcoin Market-Value-to-Realized-Value (MVRV) Ratio* (Murad Mahmudov and David Puell)

*Introducing NVT Ratio (Bitcoin's PE Ratio), use it to detect bubbles* (Willy Woo)

Scarcity and Bitcoin Valuation (PlanB)

A Comparative Study of CSI 300 Index Futures and Xinhua FTSE China A50 Index Futures (Wang Suyang, Sun Yan, Zhou Yue)