4. Exchange Analysis

4.1 Overall Exchange Comparison

“Competition among digital asset derivatives exchanges continues to heat up—and remains far more intense than in the spot market.”

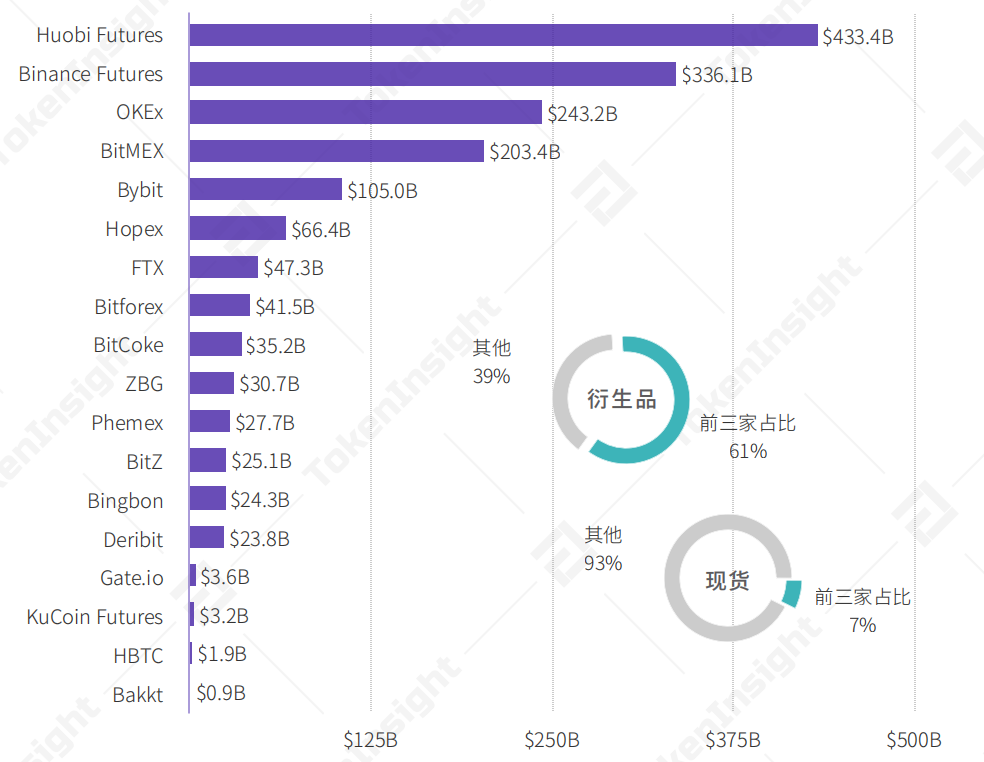

The chart below shows the total trading volume for each derivatives exchange this quarter. The top three exchanges accounted for 61% of the total volume, while the top six made up 83%—representing increases of 5% and 2%, respectively, from Q1 2020.

Derivatives exchange trading volumes and market concentration in Q2 2020. Source: TokenInsight

In contrast, the top three spot exchanges combined accounted for just ~7.3% of total spot volume during the same period—less than one-eighth of the concentration seen in derivatives. Furthermore, no single spot exchange captured more than 3% of the overall spot market, while Huobi Futures alone commanded over 25% of the entire derivatives market this quarter. Competition among digital asset derivatives exchanges intensified this quarter, with the battle for leadership becoming especially fierce.

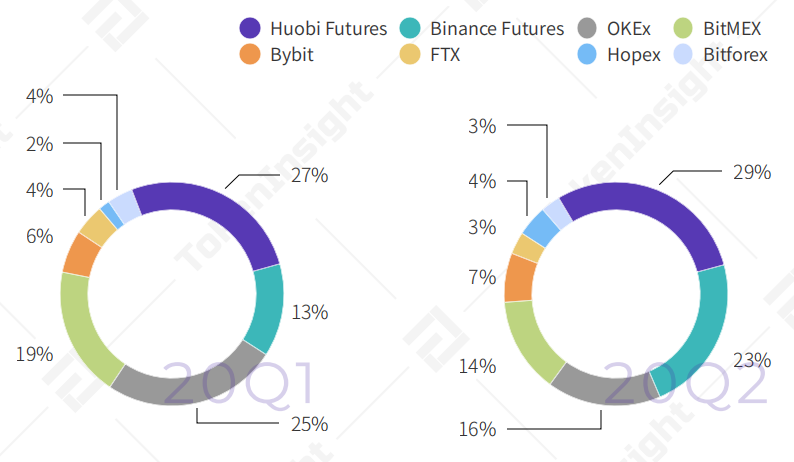

Specifically, the market share shifts among the top eight derivatives exchanges (by volume) this quarter were as follows.Huobi Futures held its share just under 30%, while Binance Futures grew its share by 10%, taking a portion of the market from BitMEX and OKEx. Beyond these four, no other exchange reached a 10% market share or surpassed $200B in quarterly trading volume.

Market share of the top eight derivatives exchanges (by volume) in Q2 2020 vs. the previous quarter. Source: TokenInsight

4.2 Exchange Classification Criteria

“The digital asset derivatives landscape is becoming more segmented—broad generalizations no longer apply.”

Today, digital asset derivatives exchanges have clearly differentiated themselves in terms of products, target users, and geographic focus. For instance, large-scale exchanges like Huobi Global / Huobi Futures pursue a comprehensive strategy across spot, derivatives, and OTC markets. Specialized derivatives platforms such as Bybit focus exclusively on perpetual and futures contracts, while compliance-centric exchanges like Bakkt prioritize building strong regulatory frameworks. Even emerging exchanges with lower current volumes—including HBTC, ZBG, and Bingbon—possess unique competitive edges; and decentralized exchanges like dYdX have begun offering BTC perpetual contracts.

Given the significant differences in strategic focus among exchanges, comparing digital asset derivatives platforms within peer groups yields more practical insights than blanket comparisons across the entire industry.TokenInsight has classified the 42 digital asset derivatives exchanges covered in this report using the following criteria.

Source: TokenInsight, Q2 2020 Derivatives Exchange Classification Criteria

The other exchanges listed in the table above differ significantly and do not form a coherent group. Due to the scope and cost constraints of this report, they will not be analyzed in detail.

“Digital asset derivatives exchanges have only two viable paths forward:

First, specialization in trading, like Bybit and FTX;

Second, becoming a large, all-encompassing platform, like Huobi and Binance.

Smaller exchanges will face severe challenges in the second half of 2020.”

— Zhang Xiaoling, Hopex

4.3 Large-Scale Derivatives Exchanges

“Large-scale derivatives exchanges serve a niche by focusing exclusively on derivatives traders.”

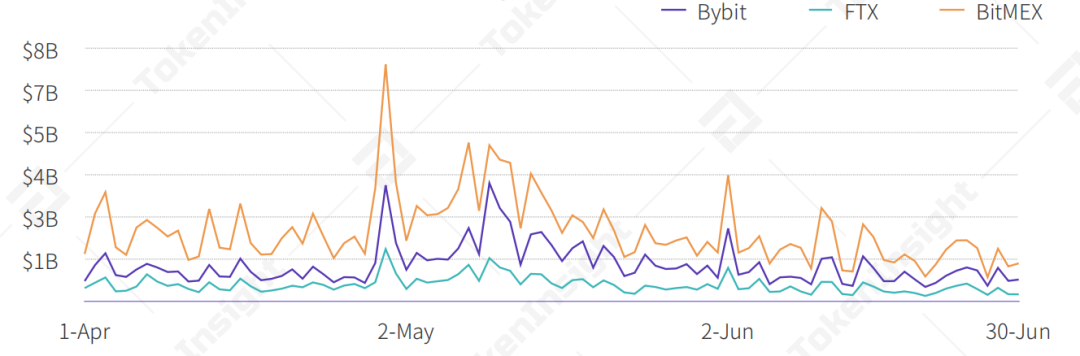

We classify exchanges as large-scale derivatives platforms if their quarterly trading volume exceeds $45 billion and their primary focus is derivatives. This category includes Bybit, FTX, and BitMEX. Unlike large comprehensive exchanges that operate multiple business lines, these three platforms concentrate almost entirely on derivatives. Only FTX conducts a minor amount of spot trading ($2.15B, representing 0.04% of total market share). The success of these specialized exchanges suggests a viable strategy for market participants: targeting a specific niche.

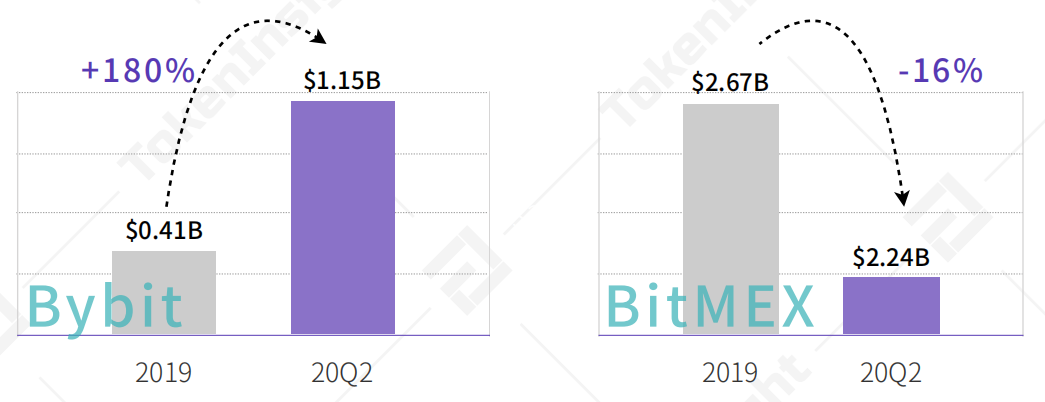

Daily Trading Volume of Large-Scale Derivatives Exchanges in Q2 2020. Source: TokenInsight

This quarter, Bybit led growth in this category with an average daily trading volume of $1.15B, a 180% increase year-on-year from its full-year 2019 average. BitMEX reported an average daily volume of $2.24B, down 16% year-on-year. Note: FTX was founded in mid-2019, so comparable year-on-year data is unavailable.

Change in Average Daily Trading Volume: Q2 2020 vs. Full-Year 2019 for Large-Scale Derivatives Exchanges. Source: TokenInsight

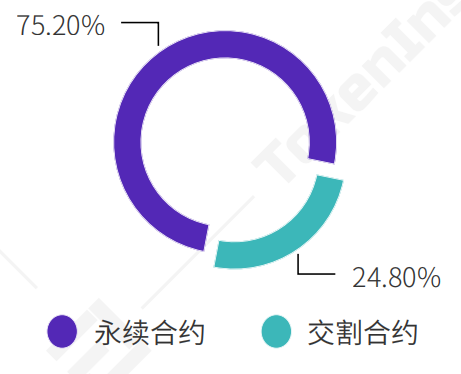

Perpetual vs. Delivery Contract Trading Volume in Q2 2020. Source: TokenInsight

As the chart shows, perpetual contracts made up 75.2% of total derivatives volume in Q2 2020, up from 39.1% in Q1. This indicates a clear shift in trader preference from delivery contracts to perpetual contracts. This trend benefits large-scale derivatives exchanges, whose core business is often perpetual contracts.

“In terms of user growth, Bybit hit new highs in April and May this quarter, with monthly growth exceeding 20%. Growth moderated slightly in May. We also saw increased trading volume from Japan this quarter.”

— Ben, Bybit

4.4 Large Comprehensive Exchanges

“Mega-exchanges are heavily focused on derivatives, with their average contract trading volume 4.4 times that of spot trading—far above the industry average.”

This quarter, mega-exchanges doubled down on derivatives trading. Their daily volumes are shown in the chart below.

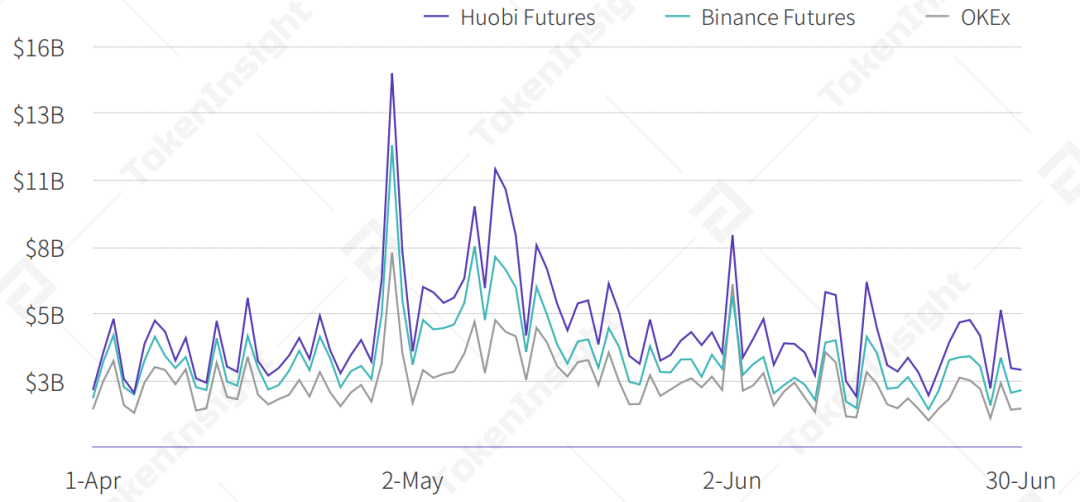

Daily derivatives trading volume of mega-exchanges in Q2 2020. Source: TokenInsight

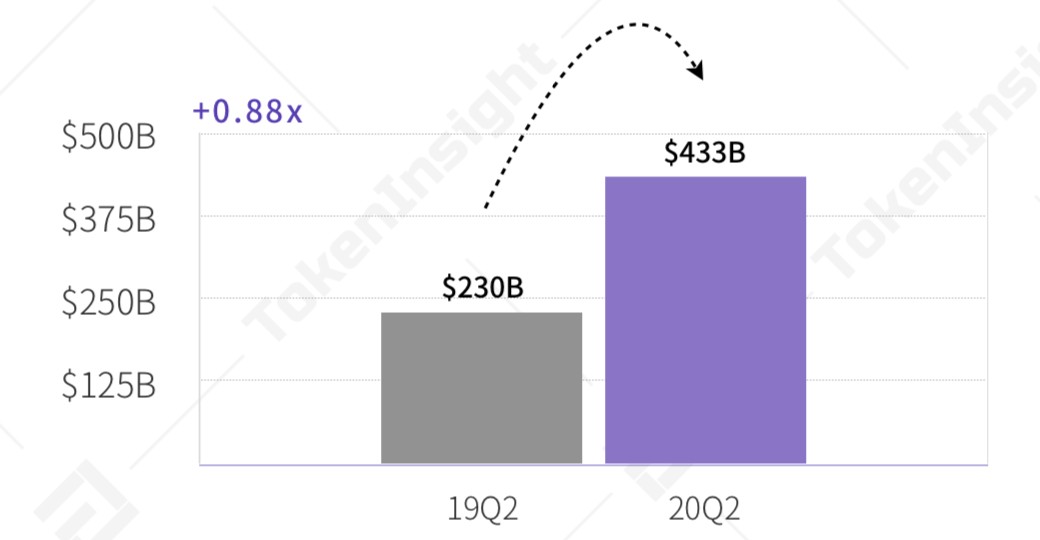

Huobi Futures trading volume: Q1 2020 vs. Q1 2019. Source: TokenInsight

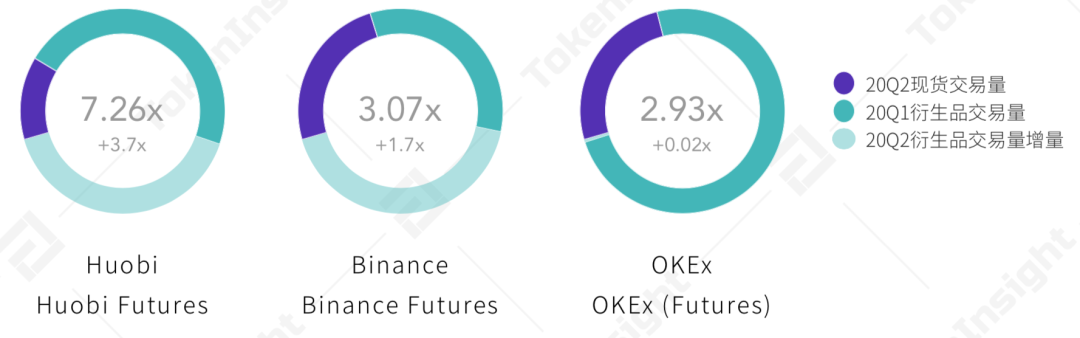

Among the four mega-exchanges with quarterly trading volumes exceeding $200 billion, Huobi Futures led in daily volume this quarter, averaging roughly $4.8 billion—about 30% higher than Binance Futures ($3.73 billion). OKEx and BitMEX followed with daily averages of $2.7 billion and $2.26 billion, respectively.

In terms of growth, Huobi Futures' total quarterly volume rose 88% year-over-year. Its derivatives-to-spot ratio jumped 3.7 times from Q1 2020, reaching 7.26x—the highest among all mega-exchanges.

Derivatives-to-spot trading volume ratios for mega-exchanges, Q1–Q2 2020. Source: TokenInsight

Binance Futures also saw a significant rise in its derivatives-to-spot ratio this quarter, while OKEx's ratio remained nearly flat compared to Q1. The average ratio across mega-exchanges hit 4.4x—160 times the broader market level of 0.274. This underscores how heavily mega-exchanges prioritize derivatives.

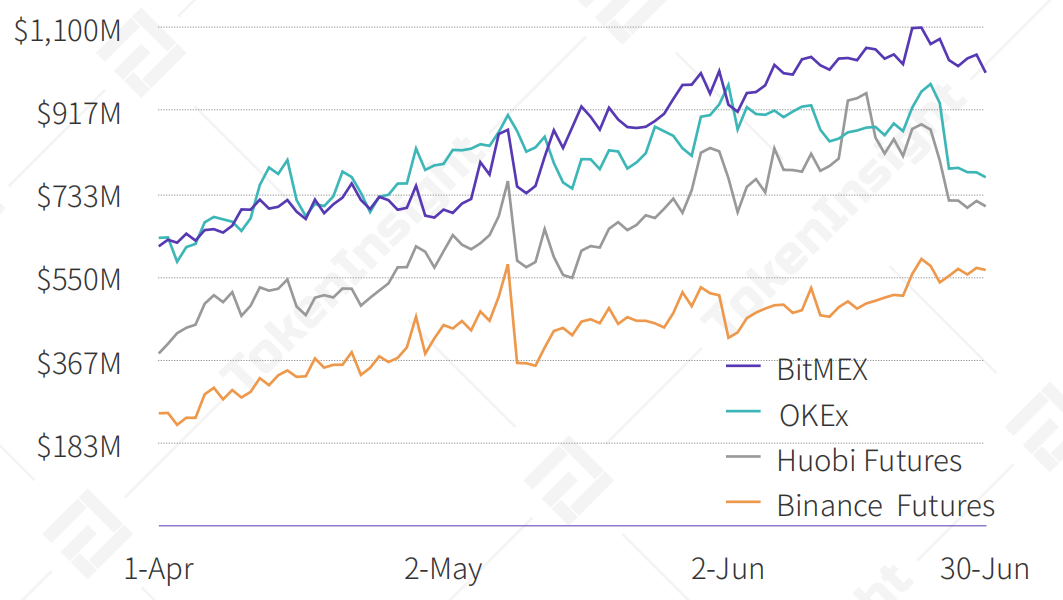

Daily open interest for mega-exchanges (including BitMEX) in Q2 2020. Source: TokenInsight

“Open interest data suggests large-volume traders are likely concentrated on BitMEX.”

From April to May 2020, BitMEX (avg. $769.9M) and OKEx (avg. $773.4M) had nearly identical daily open interest, with neither holding a clear lead. In June, BitMEX's open interest continued climbing, averaging $1,019.2M for the month, while OKEx's growth was more modest at $883.8M daily. Throughout June, BitMEX's average open interest was 39% above the mega-exchange group average ($731.6M), indicating that large-volume traders ("whales") likely favor BitMEX.

“In the digital asset exchange industry, the multi-player competition led by HBOT will continue, evolving into a ‘winner-takes-all’ dynamic. This will further squeeze market share for mid- and small-sized exchanges, posing serious survival challenges.”

— Tom, Huobi Futures

4.5 Key Emerging Exchanges

“Key emerging exchanges are disrupting the market with distinct strategic approaches.”

Compared to major, full-service exchanges with daily trading volumes in the tens of billions, key emerging exchanges typically report significantly lower volumes. As latecomers, they can't match the giants overnight. Their strategy often involves carving out a specific niche.

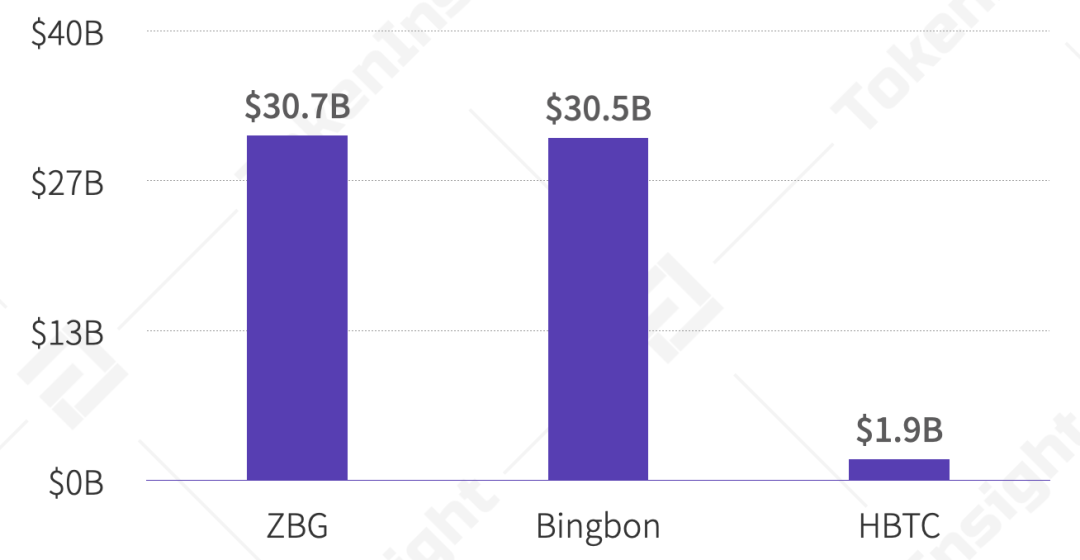

Derivatives trading volume of key emerging exchanges in Q2 2020. Source: TokenInsight

ZBG, a sister exchange of ZB, focuses on the derivatives gap left by its parent. Its breakthrough strategy centers on user education, attracting over 2.5 million visits last quarter with an average session time exceeding 15 minutes. This approach has paid off: its quarterly trading volume surged 11.1x from $2.76B in Q1 2020.

Bingbon Exchange took an indirect route, first targeting Southeast Asia and offering compliant USDC-based stablecoin trading—attracting over 100,000 registered traders so far.

Most derivatives exchanges use only spot trading fees for platform token buybacks. HBTC innovated by sharing a portion of its derivatives revenue with holders of its native token (HBC). Data shows HBTC has already repurchased over 450,000 HBC.

Phemex pioneered a membership model for spot trading, where members trade with zero fees—a tactic that attracts and retains high-volume traders.

Competition in crypto derivatives is fierce, and emerging exchanges face steep challenges. But as the saying goes, "When the Eight Immortals cross the sea, each one shows their true prowess." Opportunities await those who are observant and prepared.

“Risk management is critical—we don't encourage new users to dive into derivatives blindly. They can start by practicing on ZBG's demo trading platform.”

— Xiangxiang, ZBG

4.6 Compliant Exchanges

“Compliant exchanges still represent a small slice of total trading volume, as regulation for crypto derivatives remains in its early stages.”

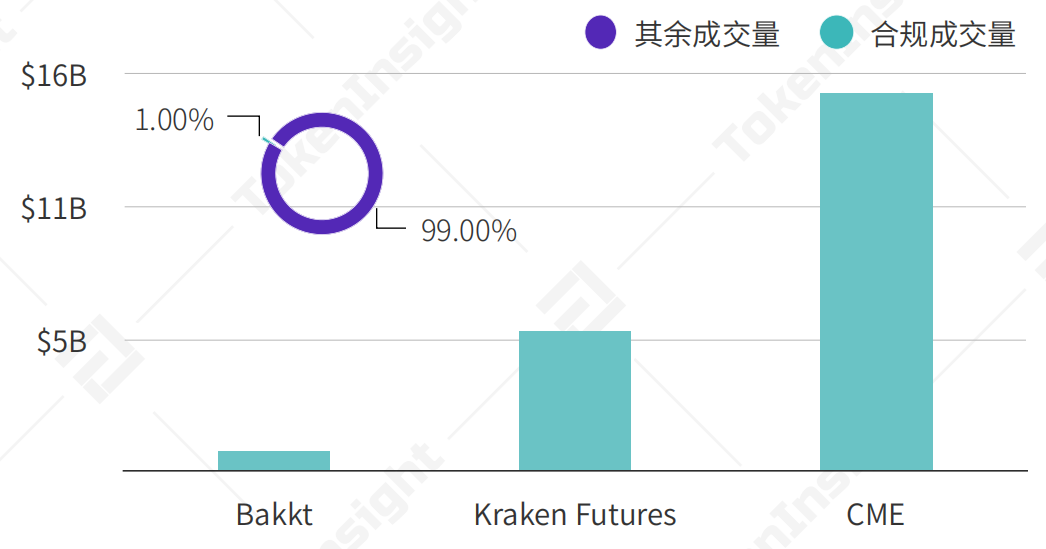

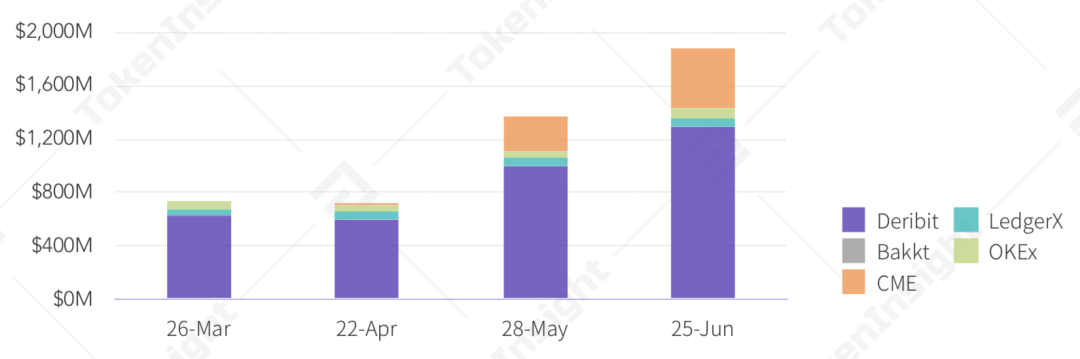

This report covers Bakkt, CME, and Kraken Futures (Crypto Facilities). Their combined reported trading volume this quarter was $21.62B.

Overview of trading volume for compliant exchanges in Q2 2020. Source: TokenInsight

As blockchain-based assets, cryptocurrencies are built on decentralized principles; however, decentralization doesn't mean a lack of rules. On the contrary, well-designed regulation better protects all market participants and their funds. TokenInsight hopes the derivatives industry will achieve a regulatory "soft landing" soon, elevating the entire ecosystem.

“Spot markets were relatively quiet in Q2, while derivatives saw stronger performance. Few new quality spot projects emerged, and many from last year failed to deliver—disappointing investors. But capital stayed in the market and flowed into derivatives.”

— Li Xiandong, BiKi

4.7 Decentralized Exchanges (DEXs)

The launch of the PBTC-USDC perpetual contract on the decentralized exchange dYdX generated approximately $22 million in trading volume this quarter, accounting for roughly 0.1% of the total market. This contract is a BTC perpetual futures product offering 10x leverage and utilizes several DeFi technologies, including oracle price feeds.

The emergence of decentralized digital asset derivatives exchanges highlights the significant potential of DeFi. For more on DEXs and DeFi, see TokenInsight’s “DeFi Series Reports.”

5. Options Overview

“While digital asset derivatives exchanges are actively expanding into options, these products remain largely inaccessible to mainstream retail traders.”

Several digital asset derivatives exchanges now offer options or options-like products. However, due to technical hurdles and limited market maker infrastructure, the flexibility of these products varies widely across platforms. The two main industry approaches are standardized “T-shaped” options, as offered by Deribit and OKEx, and at-the-money (ATM) options, exemplified by Binance Futures. In addition to mainstream digital asset options, platform token options have also emerged. For example, among prominent newer exchanges, HBTC offers options trading for BNB, HT, and OKB.

Deribit captured roughly 60% of global options trading volume this quarter, with average daily volume exceeding $45 million; OKEx and CME also hold notable market shares. In terms of open interest, Deribit’s outstanding BTC options peaked at $1.3 billion at the end of June 2020, while CME’s stood at $439 million during the same period. These two exchanges currently dominate the digital asset options market.

However, most digital asset options products still suffer from insufficient liquidity to varying degrees. For instance, Deribit’s options chain shows gaps in completeness, such as relatively sparse strike price intervals and wide bid-ask spreads. Compared to Deribit, other digital asset derivatives exchanges face even greater shortcomings in their options offerings.

BTC Options Open Interest Across Major Exchanges by Expiry Date, Q2 2020. Source: Skew; TokenInsight

As a key component of the financial derivatives toolkit, options are highly active in traditional markets, where over-the-counter (OTC) options volume can exceed the underlying asset’s trading volume by dozens of times. The digital asset options market is poised for growth. Exchanges that proactively develop and deploy options products now may capture significant market share in the future.

“Digital asset options are still in their infancy. The number of users trading options on Deribit is only about one-tenth of those trading futures contracts. Moreover, I believe American-style options won’t see widespread adoption until European-style options mature.”

— Lin, Deribit

6. Regulatory Updates

January 2020:

① The Canadian Securities Administrators (CSA) released guidance for digital asset exchanges;

② The European Union’s Fifth Anti-Money Laundering Directive (5AMLD) entered into force, now applying to digital asset exchanges;

③ Japan’s Financial Services Agency (FSA) mandated prior registration and approval for conducting digital asset derivatives trading;

February 2020:

February 2020:

① Switzerland introduced stricter regulations, mandating that digital asset exchanges verify customer identities for transactions over $1,000.

② The International Organization of Securities Commissions (IOSCO) published a report calling for tighter regulation of digital asset exchanges.

③ Singapore’s Court of Appeal dismissed Quoine's appeal against a ruling that found its reversal of trades unlawful.

March 2020:

① The U.S. Commodity Futures Trading Commission (CFTC), the primary derivatives regulator, clarified rules for physically settled digital asset products.

② South Korea passed amendments to the "Act on Reporting and Using Specified Financial Transaction Information," extending Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) rules to digital asset exchanges.

③ The Monetary Authority of Singapore (MAS) granted several exchanges exemptions from the Payment Services Act (PSA) licensing requirement.

April 2020:

① Japan enacted amended legislation requiring two forms of KYC documentation to open an account with a digital asset exchange.

② The U.S. Securities and Exchange Commission (SEC) postponed its decision on the digital asset exchange operated by Overstock's subsidiary.

May 2020:

① Dutch digital asset exchange BitKassa shut down on May 17th following new regulatory policies in the Netherlands.

② The Cayman Islands government passed the Virtual Asset (Service Providers) Act, 2020.

③ The SEC again delayed its approval for the digital asset exchange run by Overstock's subsidiary.

June 2020:

① Canada formally recognized digital asset exchanges as Money Services Businesses (MSBs), requiring them to register with the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC).

② The Chair of the U.S. Federal Reserve voiced support for replacing LIBOR with exchange products based on Ethereum.

7. Users and Market Sentiment

7.1 Market Sentiment

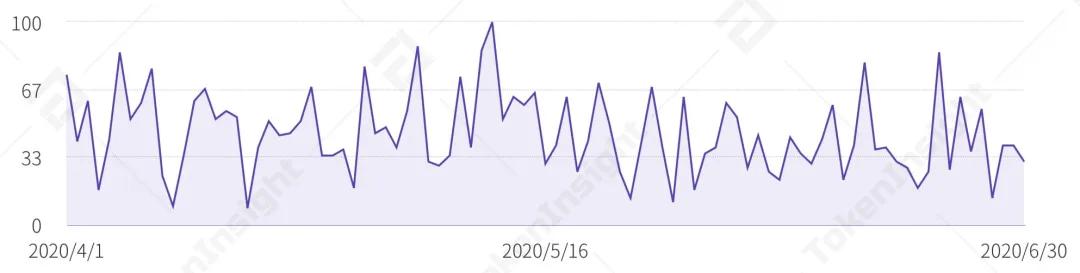

For Q2, TokenInsight tracked Google Trends data for 11 keywords—including "Bitcoin Futures" and "Cryptocurrency Futures"—and calculated their average.

Google Trends results for digital asset derivatives-related keywords in Q2 2020. Source: Google; TokenInsight

The chart shows that market sentiment around digital asset derivatives fluctuated throughout Q2 2020, peaking around May 10–11. During that period, BTC's price fell by roughly $1,500 while trading volume hit a quarterly high. This indicates that Google Trends effectively captures sentiment within the digital asset secondary market, allowing traders to gauge potential price movements based on its shifts.

Global Popularity of Digital Asset Derivatives in Q2 2020. Source: Google Trends; TokenInsight

Media Partners