"Dedao Think Tank | 2022–2023 Global Cryptocurrency Market Annual Report: A New Beginning" is a comprehensive analysis and review of the global cryptocurrency market in 2022, produced by ChainDD's research team, Dedao Think Tank.

This annual report begins with an overview of the overall market capitalization changes in the global cryptocurrency market and the top 30 cryptocurrencies. It then provides a comprehensive review of the most prominent Web3 sectors in 2022, analyzes the challenges faced by the centralized exchange (CEX) industry—exemplified by platforms like FTX and Binance—and concludes with a summary of regulatory developments and policy initiatives related to cryptocurrencies from countries and regions around the world. The report aims to offer efficient, professional, and clear decision-making support for investors, entrepreneurs, developers, and other market participants.

The report is divided into four chapters, as follows:

Chapter 2: Web3 Amidst the Internet Industry’s Transformation

Chapter 3: The Turbulent CEX Market: From Bankruptcy to the Shadow of Black Swans

Chapter 4: Policy Review of Cryptocurrency Regulations Across Major Countries and Regions Globally

Dedao Think Tank will release one chapter per day over the coming days for readers' reference.

In Chapter 4, Dedao Think Tank reviews the key laws, policies, pilot programs, and progress related to the cryptocurrency sector issued by major countries and regions in 2022. The full content of Chapter 4 is provided below:

Chapter 4: Policy Review of Cryptocurrency Regulations Across Major Countries and Regions Globally

—1—

United States

Digital Dollar

On March 9, U.S. President Joe Biden signed an executive order directing federal agencies to study and explore the creation of an official digital dollar. Agencies were given between 60 and 210 days, depending on the complexity of their tasks, to complete their studies and submit reports. White House officials stated they plan to act swiftly on the recommendations but did not provide a specific timeline.

The White House emphasized that "researching and developing potential designs and deployment options for a U.S. Central Bank Digital Currency (CBDC)" was its "most urgent priority." It directed the Treasury Department to collaborate with other agencies to submit a report within 180 days on "the future of money and payment systems," covering the conditions for broad digital asset adoption and the potential impact of a U.S. CBDC.

On September 16, U.S. federal regulators announced they would hold regular meetings to support the Federal Reserve's research into a potential digital dollar. The Treasury Department also recommended establishing a federal framework for non-bank payment providers.

Stablecoin Regulation

Following the Terra incident, U.S. and U.K. regulators jointly reaffirmed their commitment to supporting responsible stablecoin innovation while strengthening oversight.

On July 1, financial regulators from both countries issued a joint statement during a U.S.–U.K. Financial Innovation Partnership (FIP) meeting, pledging continued collaboration on safe innovation and cross-jurisdictional stablecoin regulation.

The statement noted that recent events highlighted the critical role of stablecoins and crypto platforms, the differences in their governance, and the need for robust cross-border regulatory cooperation. Participants also discussed opportunities for further dialogue on broader crypto asset regulation.

They emphasized the importance of continued cooperation in international forums, including the G7, the Financial Stability Board, and the Bank for International Settlements, on issues related to crypto assets, stablecoins, CBDCs, and cross-border payments.

Participants intend to continue engaging on these topics to support the next U.S.–U.K. Financial Regulatory Working Group meeting.

—2—

Hong Kong

Hong Kong’s Policy Statement

On October 31, Hong Kong's Financial Services and the Treasury Bureau released the "Policy Statement on Virtual Assets Development in Hong Kong," outlining the government's stance and strategy for fostering a vibrant virtual asset ecosystem.

The statement affirms Hong Kong's open and inclusive attitude toward global virtual asset innovators. The government recognizes the potential of Distributed Ledger Technology (DLT) and Web3.0 to shape the future of finance and commerce, believing that proper regulation can enhance efficiency and transparency. Hong Kong's growing ecosystem is evidenced by NFT issuance, metaverse development, and DLT use in trade finance.

While preparing a new licensing regime for virtual asset service providers (VASPs), Hong Kong invites global exchanges to explore opportunities there. The Securities and Futures Commission (SFC) will consult the public on allowing retail trading under the new regime. The government also welcomes virtual asset ETFs and is open to reviewing the legal status of tokenized assets and smart contracts.

The statement highlights three pilot projects: NFT-based certificates for Hong Kong FinTech Week, tokenized green bonds for institutional investors, and the digital Hong Kong dollar (e-HKD), intended to bridge fiat and virtual assets.

Digital Currency e-HKD

Eddie Yue, Chief Executive of the Hong Kong Monetary Authority (HKMA), stated that the HKMA would launch a series of pilot programs with banks and tech firms in Q4 2022 to test the e-HKD and identify compelling use cases. He noted that for public adoption, the e-HKD must offer clear advantages in convenience or cost over existing electronic payment systems.

—3—

Japan

Digital Yen

On November 24, 2022, Bank of Japan (BOJ) Executive Director Shinichi Uchida announced that the BOJ would partner with Japan's three mega-banks and regional banks to conduct pilot tests for a digital yen, advancing its CBDC plans. A final decision on issuance could come as early as 2026.

Starting in spring 2023, the next phase of Japan's CBDC pilot will involve collaboration with commercial banks to test depositing and withdrawing the "digital yen" and develop offline payment functionality. This two-year trial is the final stage of the pilot program.

The BOJ's CBDC roadmap has three phases: Phase 1 (2021) validated core functionality; Phase 2 added peripheral functions to identify issues; and the upcoming pilot represents Phase 3.

Additionally, the BOJ will host a forum in early 2023 to exchange views with private enterprises on CBDC technology.

—4—

Singapore

4.1 Cryptocurrency Regulation

1) Security Tokens

As a supplement to the Securities and Futures Act (SFA), the Monetary Authority of Singapore (MAS) issued its "Guidance on Digital Token Offerings" in 2017, revised in 2020. It stipulates that digital tokens qualifying as capital markets products (e.g., securities, bonds) fall under MAS supervision. Intermediaries offering security token services must hold the appropriate license.

The guidance regulates security tokens, and MAS assesses projects case-by-case. Entities raising funds via cryptocurrencies are subject to securities regulations.

2) Digital Payment Tokens

Singapore's Payment Services Act (PSA), enacted in 2019, regulates seven payment service categories, including digital payment token (DPT) services. DPTs are defined as cryptocurrencies used for payment, such as Bitcoin (BTC) and Ethereum (ETH).

Similar to Hong Kong's "virtual assets," Singapore's DPT definition aligns with standards from the Financial Action Task Force (FATF).

Providing DPT services in Singapore requires a license from MAS and compliance with anti-money laundering and counter-terrorist financing requirements.

On January 4, 2021, Singapore's Parliament passed amendments to the Payment Services Act to align with the Financial Action Task Force's (FATF) international standards for anti-money laundering (AML) and countering the financing of terrorism (CFT). The amendments broadened the definition of digital payment token (DPT) service providers to include entities offering DPT transfers, custody services, and facilitating decentralized DPT trading. This move tightened regulations on digital payment services and enhanced AML/CFT oversight.

On January 17, 2022, the Monetary Authority of Singapore (MAS) issued "Guidance on Provision of DPT Services to the Public," highlighting the high risks associated with digital payment tokens (DPTs) and deeming them unsuitable for the general public. The guidance mandates that DPT service providers refrain from promoting their services in public areas or on mainstream social media. Promotional activities are restricted to their official websites, mobile apps, and verified social media accounts.

In April 2022, Singapore's Parliament approved the Financial Services and Markets Act (FSM). This legislation requires digital token issuers and service providers to obtain valid financial licenses and imposes stricter AML/CFT requirements. Drawing on FATF standards, the FSM expands the scope of regulated DPT services to include direct or indirect trading, exchange, transfer, custody of cryptocurrencies, and the provision of related investment advice. It also extends regulatory reach to cryptocurrency service providers based in Singapore but serving clients overseas.

On October 26, 2022, Singapore released a public consultation paper on regulatory measures for digital payment token (DPT) services. The aim is to further refine DPT regulations to mitigate transaction risks and enhance investor protection.

3) Stablecoins

On October 26, 2022, the Monetary Authority of Singapore (MAS) issued a consultation paper outlining proposed regulatory policies for stablecoins. In the paper, MAS stated that “if well-regulated, stablecoins have the potential to serve as reliable digital mediums of exchange.”

Currently, stablecoins are classified as digital payment tokens (DPTs) under the Payment Services Act (PSA). However, MAS believes that as Singapore develops its digital asset ecosystem, a dedicated regulatory framework for stablecoins is necessary. The existing PSA regime is deemed insufficient as it lacks specific mechanisms to ensure the value stability of stablecoins.

Given the diversity of stablecoins—which vary by underlying assets and stabilization mechanisms—MAS plans to focus its regulatory efforts on: single-currency pegged stablecoins (SCS) and stablecoins issued in Singapore. To achieve this, MAS intends to introduce a new provision under the Payment Services Act to regulate "stablecoin issuance services," with a focus on ensuring high value stability for SCS.

4.2 Digital Currency

In November 2016, the Monetary Authority of Singapore (MAS), in collaboration with several industry partners, launched Project Ubin. This initiative explored the issuance of a central bank digital currency (CBDC) using distributed ledger technology (DLT), investigated practical DLT applications for clearing and settlement, and piloted interbank payment and settlement solutions based on CBDC.

—5—

Russia

Digital Ruble

The Central Bank of Russia first introduced the concept of a digital ruble in October 2020 and completed a prototype platform by December 2021.

Pilot testing for the digital ruble began in January 2022, starting with consumer-to-consumer (C2C) payments. Initial participating banks included Ak Bars, Alfa-Bank, Dom.rf Bank, Gazprombank, Rosbank, Sberbank, Bank Soyuz, and Transcapitalbank. The second phase will involve the Ministry of Finance and financial intermediaries, enabling transactions between individuals and businesses—covering C2B, B2B, and B2G payments.

In late February, following the outbreak of the Russia-Ukraine conflict, the US and allied nations imposed financial sanctions on Russia. In early April, Central Bank official Olga Skorobogatova emphasized the urgent need for the digital ruble, confirming that regulators would not delay upcoming tests of the prototype platform.

In May, Russian monetary authorities announced plans to begin testing with real transactions and customers starting in April 2023. On September 27, officials indicated intentions to use the digital ruble for trade settlements with China before the end of 2023. Settlement testing with banks is currently underway and is expected to be completed by early next year.

On January 1, 2023, Russian lawmakers, led by Anatoly Aksakov, Chairman of the Committee on Financial Markets, submitted a draft bill on the digital ruble to the State Duma—the lower house of Parliament. The bill proposes legislative amendments to create the necessary conditions for the digital ruble's introduction.

According to explanatory notes cited by RBC's crypto portal, a Russian business news site, the bill's primary goal is to develop the payment infrastructure for the digital ruble. Proponents argue this will provide Russian citizens, businesses, and the state with a fast, convenient, and low-cost funds transfer system.

—6—

Europe

Digital Euro

On February 11, Mairead McGuinness, the European Union's financial commissioner, stated at a fintech conference hosted by Afore Consulting that the EU would formally consider legislation for a digital euro in early 2023.

On April 30, the European Central Bank (ECB) and the Eurosystem began inviting payment service providers, banks, and other relevant companies to participate in developing customer-facing prototypes for a central bank digital currency (CBDC).

In May, the ECB published a report titled "Privacy Options for the Digital Euro." Acknowledging public privacy concerns regarding CBDCs, the report stressed the need to balance these concerns "with other EU policy objectives, particularly anti-money laundering and countering the financing of terrorism (AML/CFT)." In practice, this means the baseline scenario involves full transaction transparency for intermediaries like banks. However, options for higher privacy in low-value transactions are still under discussion and "may be investigated in cooperation with legislators."

On May 13, the ECB released another working paper on the digital euro, providing a broad technical analysis of a potential European CBDC and its role within the existing financial system. The paper examines issues including financial intermediation, payment choices, and privacy in the digital economy, offering several algebra-based conclusions. It finds that while an "anonymous CBDC" may be preferable to traditional digital payments like bank deposits, it "could potentially be displaced" by "payment tokens" issued by digital currency platforms or tech giants—especially if these platforms compete with banks in financial services.

On September 29, the European Central Bank published "Progress Made During the Investigation Phase of the Digital Euro." Regarding transaction validation, the report stated that the Eurosystem would further explore online solutions where transactions are validated by third parties. The Governing Council also approved continued exploration of peer-to-peer validation for offline payments. Several steps remain before launch: in Q1 2023, the European Commission will propose a legal framework; subsequent design decisions must address settlement models, distribution, the role of intermediaries, and funding arrangements; and the Governing Council will decide in autumn 2023 whether to proceed to the implementation phase—developing and testing technical solutions and operational arrangements.

On November 10, ECB President Christine Lagarde noted at a dedicated CBDC conference that Eurozone authorities had made solid progress in exploring the rationale, benefits, and risks of CBDCs. Work has now shifted toward the specific design of the digital euro and its integration into the legal framework.

On December 21, the ECB published a report on the digital euro project, stating, "We will finalize the overall design of the digital euro in the second half of next year." The report confirms that private financial institutions and payment service providers will handle customer-facing services—including account/wallet opening, payment processing, and AML compliance. The ECB will oversee these providers and manage the digital euro service itself.

On December 22, the ECB released its second progress report on the digital euro, outlining design and distribution options recently approved by its Governing Council. The report addresses four key questions aligned with the ECB's timeline, which aims to transition from the investigation phase to implementation in Q3 2023. It outlines roles for the Eurosystem and intermediaries, specifying that supervised intermediaries will handle all management and user-facing responsibilities, while central banks within the Eurosystem will validate and record transactions, correct errors, and ensure accuracy. The report clarifies that the ECB has not committed to blockchain technology, and the Eurosystem has yet to decide on the most suitable technology for the digital euro.

—7—

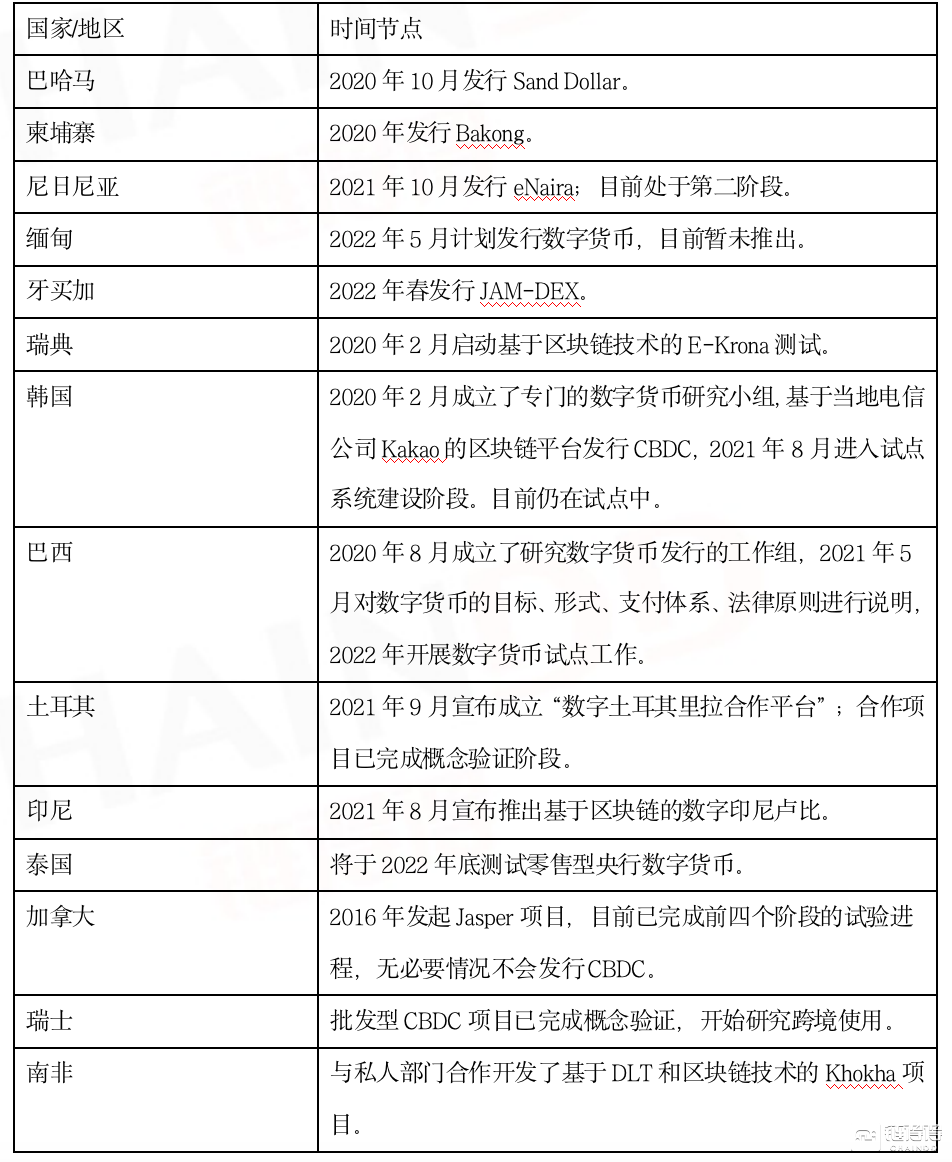

CBDC Developments in Other Countries