Web3 has matured to the point where its ecosystem has taken shape. If we map out the current Web3 landscape from a bird's-eye view, it can be broken down into four distinct layers, from the ground up: the Blockchain Network Layer, the Middleware Layer, the Application Layer, and the Access Layer. We'll explore each layer in detail below. This section also references numerous projects; due to space constraints, we won't introduce each one individually. Readers interested in a deeper dive are encouraged to consult the relevant resources.

Blockchain Network Layer

At the foundation lies the Blockchain Network Layer, the bedrock of Web3, comprised of various blockchain networks.

This layer includes numerous blockchains—Bitcoin, Ethereum, BNB Chain (BSC), Polygon, Arbitrum, Polkadot, Cosmos, Celestia, Avalanche, Aptos, Sui, and many more. According to Blockchain-Comparison, there were at least 150 active blockchains at the time of writing. We're focusing specifically on public blockchains here, excluding consortium chains. Given the sheer number, categorization is essential for clarity.

First, blockchains have a hierarchical structure: Layer 0, Layer 1, and Layer 2. Second, Web3's growth is heavily dependent on smart contract technology, which runs on a virtual machine. The relationship between smart contracts and their VM is akin to Java programs and the JVM. From this perspective, blockchains broadly fall into two categories: EVM-compatible chains and Non-EVM chains. EVM stands for Ethereum Virtual Machine. Finally, blockchains can also be categorized by their primary function, such as compute-focused versus storage-focused chains.

Let's start with the layered structure. Layer 1 is the most intuitive: well-known blockchains like Bitcoin, Ethereum, EOS, and BSC are all Layer 1 chains, also called mainnets. In distributed systems, the CAP theorem states that a system cannot simultaneously guarantee consistency, availability, and partition tolerance—it can only achieve two of the three. As distributed systems at their core, Layer 1 blockchains face a similar "blockchain trilemma," trading off between scalability, security, and decentralization. Each chain prioritizes two of these three attributes. Bitcoin and Ethereum emphasize security and decentralization, resulting in lower scalability and TPS. In contrast, chains like EOS and BSC rely on fewer consensus nodes, sacrificing some decentralization for greater scalability and significantly higher TPS.

To address the scalability limits of Bitcoin and Ethereum, Layer 2 solutions emerged. These are child chains anchored to their respective Layer 1 mainnets, designed to offload transaction volume. Layer 2s typically act as execution layers, while Layer 1 serves as the settlement layer, significantly reducing the load. Today's dominant Layer 2s are Ethereum scaling solutions like Arbitrum, Optimism, zkSync, StarkNet, and Polygon. Bitcoin also has Layer 2s, such as the Lightning Network, Stacks, RSK, and Liquid, though they remain more niche.

Layer 0 is more abstract, generally defined as the blockchain infrastructure services layer, primarily consisting of modular blockchains like Celestia, Polkadot, and Cosmos. The modular blockchain concept was pioneered by Celestia. Its core philosophy is to decouple key blockchain components—consensus, execution, and data availability—into separate, specialized chains, then integrate them to deliver full functionality. This mirrors software architecture principles that advocate for modularity, high cohesion, and loose coupling.

Cross-chain bridges or protocols that enable interoperability also fall under Layer 0. There are many such bridges; at the time of writing, debridges.com lists 113. The top three by Total Value Locked (TVL) are the official bridges for Polygon, Arbitrum, and Optimism—each facilitating asset transfers between their respective Layer 2 and Ethereum. Ranked fourth by TVL is Multichain (formerly Anyswap), a third-party bridge that connects the most blockchains—81 as of January this year.

Now, let's look at blockchains through the lens of EVM compatibility. As mentioned, they can be broadly split into EVM-compatible and Non-EVM chains.

EVM-compatible chains are the dominant force today, hosting the largest DApp ecosystem and user base in Web3. Some chains, like BSC, Heco, Arbitrum, and Optimism, are natively EVM-compatible. Others have added compatibility over time; for example, zkSync 2.0 supports the EVM, whereas its predecessor did not. Even initially non-EVM chains are increasingly adopting the standard. For instance, Polkadot launched the Moonbeam parachain for EVM support, and Cosmos introduced Evmos.

While most top-tier blockchains today are EVM-compatible, a handful of Non-EVM chains persist, including Solana, Terra, NEAR, Aptos, and Sui. Smart contracts on EVM chains are predominantly written in Solidity, while Non-EVM chains typically use Rust or Move.

The blockchains mentioned above primarily focus on decentralized computation. They generally aren't designed for large-scale data storage, such as file storage. In contrast, storage-oriented blockchains like Filecoin, Arweave, Storj, Siacoin, and EthStorage are built specifically to tackle large-scale data storage challenges.

Together, these blockchains form the "Blockchain Network Layer." This layer is dynamic, with new projects emerging while older ones may fade from prominence.

Middleware Layer

Sitting above the Blockchain Network Layer is the "Middleware Layer," which provides essential services and functionalities for applications. These include security audits, oracles, indexing and query services, API services, data analytics, data storage, basic financial services, digital identity, and DAO governance. Components that deliver these services are called "middleware," which can be on-chain protocols, off-chain platforms, or organizations (like centralized companies or DAOs). Let's explore some key examples.

Security audits are a critical middleware component. Given that most Web3 blockchains and applications are open-source and often involve financial assets, rigorous security audits are essential. These services are provided by specialized firms like CertiK, OpenZeppelin, ConsenSys, Hacken, and Quantstamp globally, and by SlowMist, ChainAegis, and PeckShield in China, alongside many smaller players.

Bug bounty platforms also play a vital role. These platforms incentivize white-hat hackers to find vulnerabilities, with rewards scaling based on the bug's severity. Immunefi is currently the largest such platform.

Next are oracles, which bridge blockchain smart contracts with external data. Blockchains are closed systems to ensure consensus; they can't natively fetch off-chain data. Oracles solve this by providing the external information many applications need, making them a cornerstone of Web3 interoperability.

Oracles today serve various niches: DeFi, NFT, SocialFi, cross-chain, privacy, and credit. Notable projects include CreDA, Privy, UMA, Banksea, DOS, NEST, and Chainlink. Chainlink, as the leading decentralized oracle network, offers a suite of products like Data Feeds, VRF, Keepers, Proof of Reserve, and CCIP.

Indexing and query services address the challenge of efficiently accessing complex on-chain data. For instance, querying Uniswap's daily trading volume directly on-chain is impractical. Leading solutions include The Graph, which allows custom indexing of on-chain data, and Covalent, which provides unified APIs for common on-chain data sets.

Beyond Covalent, other API service providers cater to specific needs: NFTScan for NFT data, Infura and Alchemy for node infrastructure, and API3 for decentralized APIs.

Indexing, query, and API services all fall under on-chain data services. Data analytics is another key category, with major players like Dune Analytics, Flipside Crypto, DeBank, and Chainalysis.

Data storage middleware is distinct from foundational storage blockchains. We classify chains like Filecoin and Arweave as part of the Blockchain Network Layer. At the middleware layer, the key player is IPFS (InterPlanetary File System)—a peer-to-peer hypermedia protocol designed to replace HTTP. While similar to a blockchain in some ways, IPFS is a protocol; Filecoin is the blockchain network built on top of it.

Middleware also includes protocols providing basic financial services. Key examples are Uniswap and Curve for trading, and Compound and Aave for lending. Although these are application-layer protocols, their widespread use as foundational building blocks—like LEGO bricks—by other applications has effectively turned them into generalized middleware.

In essence, any composable component—be it an on-chain protocol, an off-chain service provider, or a DAO—that offers services broadly needed by applications belongs in the Middleware Layer. These components are the diverse LEGO bricks that developers combine to build everything from digital identity solutions to DAO governance tools.

Application Layer

The application layer is the most dynamic part of the Web3 ecosystem, a vibrant landscape teeming with diverse decentralized applications (DApps) where innovation and competition thrive. Here, we explore several of its more established sectors.

NFT

NFT stands for Non-Fungible Token. In China, they are often called "digital collectibles" and represent unique digital assets like artworks.

The first true NFT project was CryptoPunks, launched in June 2017. It features 10,000 unique 24x24 pixel avatars, each algorithmically generated and minted on Ethereum. It remains the only major NFT project to store all image data fully on-chain. Here are a few examples from its official website:

As of this writing, CryptoPunks has a floor price of 66.88 ETH (approximately $84,397.21). The most expensive one sold for 8,000 ETH on February 12, 2022. To many, these staggering valuations are puzzling. A key reason is its pioneering status: much like Bitcoin for blockchain, CryptoPunks pioneered the NFT space, and its historical significance carries immense intrinsic value.

Inspired by CryptoPunks, Axiom Zen (later Dapper Labs) launched CryptoKitties in late November 2017. Upon release, it went viral—so much so that it congested the Ethereum network, highlighting its scalability limits. Prior to the launch, Axiom Zen's CTO, Dieter Shirley, used CryptoKitties as a case study to propose the ERC-721 token standard. Following the project's success, ERC-721 quickly became the foundational technical standard for NFTs, which it remains today.

Following CryptoPunks and CryptoKitties, NFTs began spreading across numerous fields, fueling rapid growth of the broader ecosystem. Today, they span dozens of categories. By use case, they generally fall into these classifications: Collectibles, Art, Music, Film & TV, Gaming, Sports, Virtual Land, Finance, Branding, and DID (Decentralized Identity). Below, we highlight notable projects in each.

"Collectibles" is a broad category—almost anything, from art to in-game items, can be collected. What defines an NFT as a collectible is primarily its scarcity. Among the 10,000 CryptoPunks, for example, the rare "Alien" punks are highly sought after, while the common "Male" punks are less so. Beyond CryptoPunks, the most famous collectible NFT is Bored Ape Yacht Club (BAYC). BAYC is more than a collection; it's the foundation of the "Bored Ape Universe." Its creator, Yuga Labs, later launched companion projects like Bored Ape Kennel Club (BAKC), Mutant Ape Yacht Club (MAYC), the APE token, and the Otherside metaverse platform. Together, they form a comprehensive IP franchise. BAYC's popularity has transcended crypto, spawning real-world merchandise like clothing, statues, and even themed restaurants. Its success has even eclipsed CryptoPunks, which Yuga Labs eventually acquired.

NFTs' ability to verify ownership and provenance makes them a natural fit for protecting artistic copyright. Several landmark NFT artworks stand out. First is Beeple’s "EVERYDAYS: THE FIRST 5000 DAYS," a composite of 5,000 daily digital works sold for $69.3 million in March 2021. Second is generative art, where code, not manual effort, creates the artwork. The leading platform for this is Art Blocks, which lets artists upload algorithms to mint limited-edition NFTs. Finally, the most expensive NFT artwork to date is "The Merge," which sold for $91.8 million in December 2021. Unlike a standard NFT, it's a dynamic composition of multiple "mass" tokens. Buyers purchased these tokens, not a single artwork, with 312,686 tokens sold to 28,983 buyers. Each buyer's share represents fractional ownership of the piece.

Music NFTs have risen for similar reasons as art NFTs: copyright protection and new revenue streams. Key figures include 3LAU (Justin David Blau), an American DJ who was an early adopter, selling his first NFT album in late 2020 and generating $11.68 million with his "Ultraviolet" NFT album in early 2021. He later co-founded the music NFT platform Royal. Dutch DJ Don Diablo sold his concert film NFT "Destination Hexagonia" for 600 ETH ($1.26 million at the time) in 2021. There's also Kingship, a virtual band composed of Bored Apes, formed by Universal Music Group.

NFTs have also entered film and television. Major international franchises like Game of Thrones, Batman, and The Matrix have released official NFT collections. In China, titles such as A Chinese Odyssey, The Wandering Earth, and Creation of the Gods have done the same.

In gaming, NFTs primarily serve as carriers for in-game assets. Unlike traditional game items, NFTs give players verifiable ownership and the ability to trade assets outside the game. CryptoKitties was the first major gaming NFT project. We'll delve deeper into gaming in the dedicated GameFi section below.

The sports world has also embraced NFTs, with NBA Top Shot and Sorare leading the charge. As the name implies, NBA Top Shot focuses on basketball, while Sorare is centered on football (soccer). Beyond these, sports like American football, baseball, boxing, and wrestling have all launched their own NFT collectibles.

Virtual land NFTs are primarily driven by projects built around the "metaverse" concept. Notable examples include Decentraland, The Sandbox, Roblox, Axie Infinity Land, and Otherdeed.

The fusion of finance and NFTs mainly involves applying NFTs within DeFi. For instance, liquidity positions in Uniswap V3 are represented as NFTs. Another approach is to fractionalize NFTs first, then integrate them into DeFi for activities like trading, lending, or staking to generate yield.

Brand-NFT collaborations have emerged as a novel marketing strategy. Over the past few years, countless brands have jumped on the bandwagon: luxury names like GUCCI, Louis Vuitton (LV), and Hermès; food & beverage giants including Taco Bell, Starbucks, Pizza Hut, and Coca-Cola; automotive brands like McLaren and Chevrolet; sportswear leaders such as Adidas, Li-Ning, and Nike; and many more.

Finally, let's talk about DID, or Decentralized Identity. While its importance is widely acknowledged, development has been relatively slow. To date, beyond niche systems like ENS (Ethereum Name Service), no mature DID framework has achieved significant network effects. The most widely adopted application currently is domain names: Ethereum-based ENS leads the space, serving Web3 much like DNS serves Web2. However, unlike DNS—which maps domain names to website IP addresses—ENS resolves domain names to users' Ethereum addresses. For example, Vitalik Buterin's ENS name is "vitalik.eth," which points to the Ethereum address 0xd8da6bf26964af9d7eed9e03e53415d37aa96045.

NFT use cases are incredibly diverse—the categories mentioned above barely scratch the surface. Given NFTs' ability to represent verifiable ownership of virtually any asset, the community often jokes that "everything can be an NFT."

DeFi

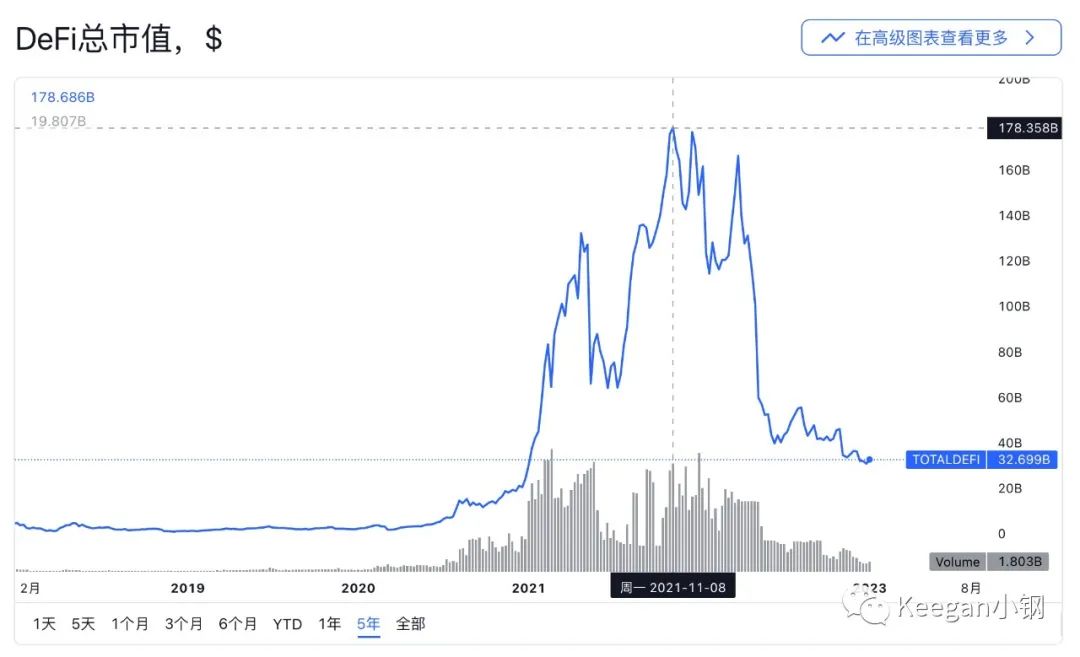

DeFi, short for Decentralized Finance, took off in the summer of 2020—a period famously known as "DeFi Summer." According to TradingView data, DeFi's total market cap was just $5 billion when it first surged that summer, before skyrocketing to nearly $180 billion by the end of 2021, marking its all-time peak.

DeFi encompasses numerous sub-sectors, including: stablecoins, decentralized exchanges (DEXs), derivatives, lending protocols, aggregators, insurance, prediction markets, and indices.

Stablecoins fall into three main categories: centralized stablecoins, over-collateralized stablecoins, and algorithmic stablecoins. Among these, over-collateralized and algorithmic stablecoins are considered decentralized stablecoins.

Centralized stablecoins are directly pegged to fiat currencies and issued by centralized entities, requiring a 1:1 reserve of fiat currency for each unit. The two most actively traded stablecoins—USDT and USDC—are both fiat-collateralized and pegged 1:1 to the U.S. dollar, issued by Tether and Circle, respectively. Additionally, Binance, the world's largest centralized cryptocurrency exchange, partnered with Paxos to launch its own fiat-collateralized stablecoin, BUSD, now the third-largest stablecoin by trading volume globally, trailing only USDT and USDC.

Over-collateralized stablecoins are created by locking up other cryptocurrencies as collateral in smart contracts. These contracts determine the amount of stablecoins minted based on the collateral's value and rely on price oracles to maintain their peg to fiat currencies. DAI, launched by MakerDAO, is the leading example of this type, maintaining a 1:1 peg to the U.S. dollar and ranking fourth in trading volume.

Algorithmic stablecoins represent a newer model, relying primarily on algorithms to regulate supply. Several projects compete in this space—including UST, FEI, AMPL, ESD, BAC, FRAX, CUSD, USDD, and USDN—but none has yet achieved true stability.

Next, let's talk about exchanges. In DeFi, "exchanges" primarily refer to decentralized exchanges (DEXs). DEXs represent the largest market-cap segment within DeFi and serve as a foundational pillar of the ecosystem. They can be broadly categorized into spot DEXs and derivatives DEXs, with the latter focusing on perpetual contracts or options. From a trading mechanism perspective, DEXs fall into two main types: orderbook-based and AMM-based. Prominent orderbook DEXs include dYdX, apeX, 0x, and Loopring. AMM-based DEXs are more numerous, with examples like Uniswap, SushiSwap, PancakeSwap, Curve, Balancer, Bancor, GMX, and Perpetual.

The orderbook model is the earliest trading paradigm, mirroring traditional stock market order matching. Users act as either makers (posting limit orders) or takers (filling existing orders), with trades executed based on price-time priority. Orderbook DEXs have evolved through three main architectural models: fully on-chain matching + settlement, off-chain matching + on-chain settlement, and Layer 2-based.

In the fully on-chain model, users submit limit and market orders directly on-chain, with execution occurring immediately against on-chain orderbooks. EtherDelta is a classic example. Its main advantage is full decentralization, but it suffers from poor transaction performance and high gas costs, as users pay fees for placing and canceling orders.

The off-chain matching + on-chain settlement model is typified by the 0x protocol. It introduces an off-chain "relayer" component: users generate signed orders off-chain and submit them to relayers, which maintain centralized orderbooks and match orders off-chain. Matched orders are then submitted individually to the blockchain for settlement. This significantly improves throughput, but on-chain settlement speed becomes the bottleneck.

The Layer 2 model is represented by dYdX, which primarily uses StarkWare's StarkEx technology. Its core architecture deploys a dedicated, application-specific Layer 2 chain where all order matching and settlement occur. Periodically, batches of transaction records are compiled into cryptographic proofs and submitted to Layer 1 for verification. Unlike general-purpose Layer 2s, dYdX's chain is built exclusively for trading, functioning like a private, application-specific chain. This model delivers a user experience nearly identical to centralized exchanges, but at the cost of higher centralization.

Today, the dominant model balancing strong decentralization with good UX is the AMM (Automated Market Maker) model. Uniswap's launch in November 2018 catalyzed its widespread adoption; subsequent protocols like SushiSwap, PancakeSwap, and Curve built upon its design. AMMs rely on liquidity pools: liquidity providers (LPs) deposit assets into these capital pools, and users trade directly against them. LPs earn a share of the trading fees generated.

That covers exchanges for now. Next, let's look at derivatives. The DeFi derivatives sector includes several key categories: perpetual contracts, options, synthetic assets, and interest-rate derivatives.

Perpetual contracts are leveraged futures contracts. Notable perpetual DEXs include dYdX, apeX, GMX, and Perpetual. Options are more complex; leading DeFi options protocols include Hegic, Charm, Opium, Primitive, and Opyn, though the market remains relatively small and underexplored. Synthetic assets are tokenized representations of underlying assets or derivatives. Early examples include DAI and WBTC, but synthetics now increasingly track real-world equities, currencies, and precious metals. Synthetix leads this space, alongside Mirror, UMA, Linear, Duet, and Coinversation. Interest-rate derivatives are financial instruments built on crypto-native interest rates, designed to provide predictable yield. Key players include BarnBridge, Swivel Finance, and Element Finance.

Now, let's turn to lending—another high-TV L segment and, like DEXs, a foundational DeFi building block. Major lending protocols include Compound, Aave, Maker, Cream, Liquity, Venus, Euler, and Fuse. Most current lending protocols use an over-collateralized lending model: for example, to borrow $80, you must post at least $100 worth of collateral, meaning the collateral value must exceed the loan value.

While over-collateralization dominates, several innovative directions are emerging: interest-free loans, isolated asset pools, cross-chain lending, and credit-based lending. Liquity exemplifies interest-free loans: users pay a one-time fee for borrowing and redeeming its stablecoin LUSD, with no ongoing interest. Isolated asset pools segregate different lending assets into independent pools, each operating autonomously to prevent contagion from bad assets or pool failures. This model has become a near-standard, adopted by Fuse (which pioneered it), Compound, Aave, and Euler. Cross-chain lending is an emerging trend, with Flux, Compound, and Aave actively expanding in this direction. Credit-based lending is common in traditional finance but rare in DeFi due to the lack of robust on-chain credit infrastructure; Wing Finance is currently the leading project in this space.

Next up are aggregators. DeFi aggregators can be grouped into several categories: DEX aggregators, yield aggregators, asset management aggregators, and information aggregators. DEX aggregators pull liquidity from multiple decentralized exchanges (DEXs) and use algorithms to find the best trading routes. Leading examples include 1inch, Matcha, ParaSwap, and MetaMask Swap—which is built directly into the MetaMask wallet. Yield aggregators like Yearn Finance, Alpha Finance, Harvest Finance, and Convex Finance automate yield farming by pooling users' funds to chase the best returns across different platforms. Asset management aggregators help users track and manage their DeFi portfolios; Zapper and Zerion are two prominent players here. Finally, information aggregators such as CoinMarketCap, DeFiPulse, DeBank, and DeFiPrime provide crucial data. It's worth noting that these are centralized platforms, yet they remain essential components of the DeFi ecosystem, highlighting that not every tool in DeFi needs to be fully decentralized.

Moving on to insurance. While insurance is a massive market in traditional finance, DeFi insurance has been slow to develop. The Web3 space is rife with risks—from smart contract bugs and rug pulls to regulatory uncertainty—creating a clear need for coverage. However, high barriers to entry in product design and development, coupled with generally low liquidity, have kept the sector in its early stages. Key projects exploring this space include Nexus Mutual, Cover, Unslashed, and Opium.

Then there are prediction markets. These are data-driven platforms where users can bet on the outcome of future events. They were among the first applications built on Ethereum and saw a surge in activity during the 2020 U.S. presidential election. Major projects include PolyMarket, Augur, and Omen.

Finally, we have the index segment. Index funds, which offer exposure to a basket of assets, are gaining popularity in DeFi. While still a niche, notable examples include DPI, sDEFI, PIPT, and DEFI++. The DeFi Pulse Index (DPI), a collaboration between DeFi Pulse and Set Protocol, is a market-cap-weighted index of leading DeFi tokens like Uniswap, Aave, and Maker, and can be redeemed for the underlying assets. Synthetix's sDEFI is the oldest index in this category; it's a synthetic asset that tracks token prices via oracles rather than holding the tokens directly. PowerPool's Power Index Pool Token (PIPT) comprises eight tokens, and the project also offers the Yearn Lazy Ape Index, Yearn Ecosystem Token Index, and ASSY Index. PieDAO issues DEFI++, which includes 14 assets, as well as BCP (containing WBTC, WETH, and DEFI++) and PLAY (a basket of metaverse project tokens).

GameFi

GameFi, short for "Game Finance," represents the fusion of gaming and decentralized finance and has become synonymous with Web3 gaming. Before this term caught on, such games were typically called blockchain games or simply "chain games."

CryptoKitties was the first blockchain game to achieve widespread recognition. This virtual pet game features unique cat NFTs. The initial generation had 50,000 cats, each with distinct traits. After buying a CryptoKitty, players can breed new kittens. Offspring inherit some traits from their parents while others are randomly generated, with each new kitten being its own NFT that can be sold. Kittens with rare traits can fetch high prices. As of late January 2023, over 2 million kitties have been created, held across more than 136,000 unique wallet addresses.

Following CryptoKitties, a wave of similar breeding games emerged, like CryptoDogs and CryptoFrogs. This trend was interrupted by Fomo3D, a transparent, open-source, Ponzi-style lottery game. Its rules were simple: users paid ETH to buy Keys. The ETH was split between prize pools, dividend pools, an airdrop pool, and a team pool. Key holders received ongoing dividends proportional to their holdings. Each round had a 24-hour countdown timer; the last person to buy a Key before time ran out would win most of the prize pool. However, each Key purchase added 30 seconds to the clock. The first round lasted an extraordinarily long time before being won through a technical exploit. Fomo3D's viral success spawned many copycats, but none proved sustainable.

The next major breakout was Axie Infinity (often called "Axie"). Blending elements of Pokémon and CryptoKitties, it lets players level up, breed, battle, and trade creatures called Axies. Its key innovation was a dual-token economy with SLP and AXS. Players earn SLP through battles and use it with AXS to breed new Axies. Both the earned tokens and the new Axies can be sold on the open market for profit.

Although launched in 2018, Axie Infinity exploded in popularity in 2021, driven largely by its Play-to-Earn (P2E) model. The gameplay loop involves an initial investment to buy Axies, playing to earn SLP and breed new Axies, then selling those assets for ETH or stablecoins to cash out. This model first took off in the Philippines, where pandemic-induced unemployment made the game's income potential highly attractive. It also drew professional gaming studios, expanding its reach to India, Indonesia, Brazil, and China. At its peak, Axie Infinity boasted over 2.8 million daily active users.

Today, the Play-to-Earn model is virtually standard for Web3 games.

Other notable GameFi titles include Decentraland, The Sandbox, Illuvium, Star Atlas, and Alien Worlds. We encourage readers to explore these projects further on their own.

SocialFi

SocialFi, short for Social Finance, merges social interaction with finance in the Web3 space, creating what is essentially decentralized social networking. It's a relatively new concept that has only gained momentum in the last two years. The sector still has few standout projects, with Lens Protocol currently leading the way.

Developed by the Aave team and launched in May 2022, Lens Protocol is not a standalone social app or a complete front-end product. Instead, it's a modular social graph platform that provides reusable components for developers to build into their own applications. In essence, Lens serves as infrastructure for Web3 social apps. At launch, it already supported over 50 ecosystem projects, including popular ones like Lenster, Lenstube, ORB, Phaver, re:meme, Lensport, and Lensta.

Lenster is a decentralized social media app accessed by connecting a Web3 wallet via Lens. Once logged in, users can post content—similar to platforms like Weibo or Twitter—with the added ability to monetize their posts. Users can also comment on others' content, though threaded replies aren't yet supported.

Lenstube is a decentralized video platform, essentially a Web3 version of YouTube.

ORB is a decentralized professional networking app with an end-to-end on-chain reputation system. It links NFTs and POAPs to users' experiences, education, skills, and projects to build verifiable, decentralized professional profiles. Users can explore job opportunities, apply for on-chain identities, share ideas, connect with other Web3 professionals, and build communities. ORB also features a Learn-to-Earn model, allowing users to earn NFTs by learning about Web3 in their spare time.

Phaver is a Share-to-Earn social app available on iOS and Android. Users can publish posts with images, links, or product apps and browse all content on Lens. By connecting their Lens Profile wallet, they can post directly to Lens through Phaver.

re:meme is an on-chain meme generator where users can upload templates and optionally set usage fees. Others can then use an image editor to add text, drawings, or other images. The :meme framework extends beyond images to include music, video, and even academic papers.

Lensport is a social NFT marketplace dedicated to the Lens Protocol. Here, users can discover, publish, and sell posts, as well as invest in and support creators.

Lensta is an image-feed app built exclusively for Lens Protocol, allowing users to browse the latest, most popular, and highest-earning posts from Lens, Lenster, Lensport, and other sources.

Access Layer

The Access Layer sits at the top of the Web3 stack, serving as the direct entry point for end users. It primarily includes wallets, browsers, aggregators, and increasingly, certain Web2 social platforms that have become gateways to Web3.

Let's start with wallets—the most critical access point. Today's wallets fall into several categories: browser wallets, mobile wallets, hardware wallets, multisig wallets, MPC wallets, and smart contract wallets.

Browser wallets are cryptocurrency wallets used directly within web browsers and are the most widely adopted type. Common examples include MetaMask, Coinbase Wallet, and WalletConnect. MetaMask is one of the most broadly supported wallets, compatible with all EVM chains and often considered the de facto standard for DApps. It's available as a browser extension for Chrome, Brave, Firefox, and Edge. Coinbase Wallet, launched by the exchange in November 2021, quickly became a strong competitor to MetaMask, though it's currently limited to Chrome. WalletConnect is unique—it's not a specific wallet app but an open-source protocol for connecting DApps to wallets. Its most common use case is linking mobile wallets to browser-based DApps: when a user selects "Connect via WalletConnect," a QR code appears for scanning with a mobile wallet to authorize the connection. WalletConnect supports all blockchains (not just EVM) and integrates with all wallet types. Unlike MetaMask and Coinbase Wallet, it requires no browser extension, making it compatible with all browsers—including Safari. As a result, WalletConnect has become the most popular wallet connector and the default standard for DApp integration.

Mobile wallets are digital asset wallets for smartphones, offered by many providers. Both MetaMask and Coinbase Wallet have dedicated mobile apps. Other prominent options include TokenPocket, BitKeep, Rainbow, imToken, and Crypto.com. Most mainstream mobile wallets support multiple chains, including both EVM and non-EVM networks. For example, TokenPocket currently supports Bitcoin, Ethereum, BSC, TRON, Polygon, Arbitrum, Avalanche, Solana, Cosmos, Polkadot, and Aptos.

Hardware wallets store users' private keys on secure, offline physical devices, connecting via USB plug-and-play. The most widely used are Ledger and Trezor. Ledger currently offers three models: Ledger Stax (launched in 2023 with a touchscreen), Ledger Nano X, and Ledger Nano S Plus. Trezor offers two: Trezor Model T (with touchscreen) and Trezor Model One. Beyond these, other hardware wallets on the market include SafePal, OneKey, imKey, KeepKey, and ColdLar.

As the name implies, a multi-signature (multisig) wallet requires multiple signatures to authorize a transaction. The most prominent example is Gnosis Safe, a set of on-chain smart contracts. It's often set up with a 2-of-3 signature scheme, where three users collectively manage the wallet, and at least two must sign off on any action for it to be executed on-chain.

MPC, or Multi-Party Computation, represents the next generation of wallet technology. MPC wallets use cryptographic techniques to split a private key into multiple shards, which are then distributed and managed by different parties. To sign a transaction, these parties work together off-chain to reconstruct the key. While they can mimic traditional multisig setups—like a 2-of-3 scheme—the core difference is where the validation happens: multisig relies on on-chain smart contracts, while MPC performs computations off-chain. Current providers in this space include ZenGo, Safeheron, Fordefi, OpenBlock, and Web3Auth.

A smart contract wallet is one where the address is tied to a smart contract account. Gnosis Safe, a multisig wallet, falls into this category. The most significant recent innovation in this area is the integration of "Account Abstraction" (AA). AA decouples the signer from the account itself, breaking the rigid link between a wallet address and a single private key. This enables features like replacing signers, implementing multisignature schemes, and even switching signature algorithms. Beyond Gnosis Safe, key players include UniPass, Argent, and Blocto.

That covers wallets for now. Next up: browsers. Since many DApps are still accessed through web frontends, browsers remain a crucial gateway to Web3. However, not all browsers support wallet extensions, so not every browser is an effective portal. Chrome is the most widely used; virtually all browser-based wallets offer Chrome extensions. Safari, in contrast, is rarely a primary entry point for Web3 DApps, as it generally only supports WalletConnect. Another notable option is Brave, a privacy-focused browser with a built-in wallet called Brave Wallet.

Some aggregators also function as Web3 access points. DappRadar, for instance, catalogs numerous DApps, allowing users to discover and connect to them directly. Other platforms like Zapper, DeBank, and Zerion help users track their assets and transaction history across various Web3 applications.

Finally, mainstream Web2 social platforms like Twitter and Reddit—home to large Web3 communities—have gradually become important gateways into the Web3 ecosystem.