By | Zhaosheng, Yulin

Reviewed by | Zeling

Preface

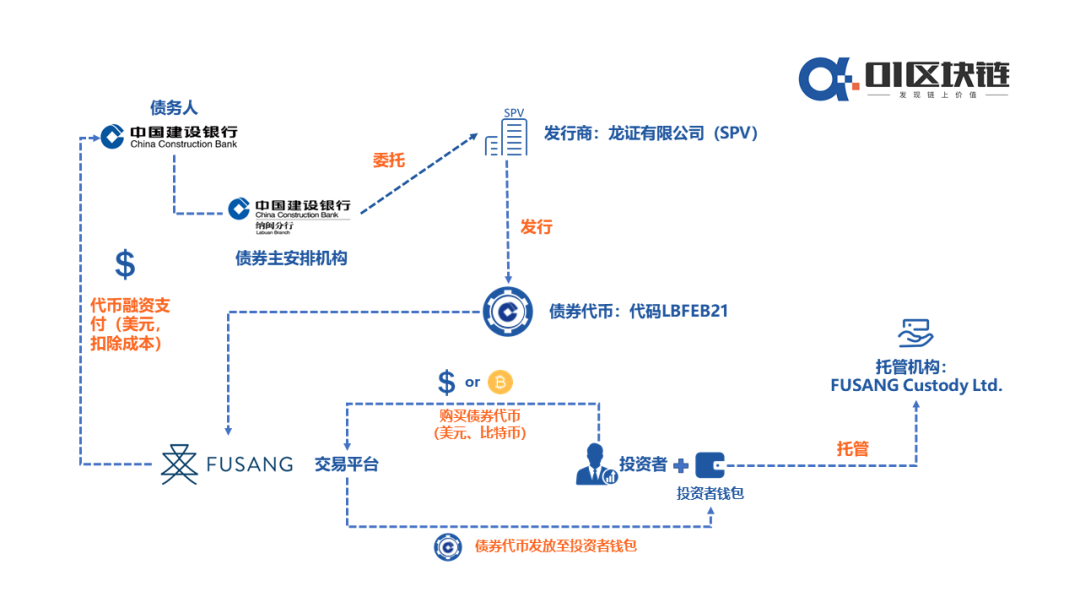

A recent South China Morning Post (SCMP) report reveals that China Construction Bank (CCB) has teamed up with Hong Kong fintech firm Fusang to issue $3 billion worth of bonds on a blockchain.

Notably, the bond is not issued by CCB's domestic entity, but by its Labuan branch in Malaysia. In October 2019, this branch secured Malaysia's first digital banking license and became CCB's first RMB clearing bank in Southeast Asia.

The CCB blockchain bond is a zero-coupon instrument with a face value of $100, offered to investors at $99.7970. According to Fusang Exchange, it will list on November 13 and mature on February 26, 2021, delivering an estimated annualized yield of 0.705%.

Accepting Bitcoin: More Symbolic Than Practical

Unlike previous blockchain bonds that merely recorded issuance data on-chain, CCB's offering is issued primarily on Ethereum as an ERC-20 token. This makes it the world's first publicly traded, tokenized debt security—a structure that closely mirrors a Security Token Offering (STO). However, given the cautious global regulatory stance on STOs, such tokenized securities are likely to remain a niche financial innovation for now, not yet ready for mass adoption.

The initial issuance involves 140,000 bond tokens, each representing a $100 bond. Both retail and institutional investors can participate, with a minimum purchase of one token ($100) and a cap of 10,000 tokens ($1 million). This dramatically lowers the barrier to entry compared to traditional bank bonds, which typically target professional investors with high minimums, signaling a move toward greater financial inclusion.

Fusang Exchange CEO Henry Chong called the tokenized bond a milestone, stating that merging blockchain with traditional securities advances financial accessibility and marks the start of "Crypto 2.0."

According to the bond documentation, investors can buy the bond using USD or BTC through Fusang Exchange. However, CCB will not settle the financing in BTC; Fusang will first convert any BTC to USD before purchasing the bond tokens. In today's bullish Bitcoin market, few investors are likely to sacrifice potential gains to experiment with buying CCB bonds using BTC. While accepting BTC currently has limited practical impact, it underscores Bitcoin's growing influence as an investment asset. This move follows similar steps by institutions like PayPal, which have recently entered the crypto space or increased their holdings of BTC and other digital assets.

Additionally, since this USD-denominated bond is issued overseas by CCB, it is not covered by China's deposit insurance, and its sale is primarily governed by Malaysian law.

Figure: Commercial Structure of CCB Bond Tokens

Blockchain Bonds Are Common—But This One Stands Out

Using blockchain technology for bond issuance is not a new concept.

In late 2019, the Bank of China launched the country's first blockchain-based bond issuance system, successfully using it to issue a RMB 20 billion special financial bond for small and micro enterprises.

However, unlike CCB's digital bond, the Bank of China's offering was simply a bond issued *using* blockchain technology; it did not involve any digital tokens.

The Bank of China's system has three core components: issuing CA certificates, forming underwriting syndicates on-chain, and recording information and transactions on-chain. Its primary value lies in leveraging blockchain to eliminate information asymmetry during issuance, reduce costs, improve efficiency, and facilitate post-issuance auditing and management through the technology's inherent data provenance.

Beyond China, Thailand's central bank launched the world's first blockchain-based government savings bond platform this year, built on IBM's technology. According to an IBM announcement on October 5, the bank sold over $1.6 billion worth of bonds within two weeks of issuance.

Thanks to blockchain, the issuance timeline was slashed from roughly 15 days to just two, boosting efficiency while lowering operational costs and eliminating redundant paperwork.

Even earlier, the World Bank partnered with the Commonwealth Bank of Australia to issue the first-ever blockchain-based bond—a two-year instrument worth about $79 million, sold to seven investors. While no cryptocurrency was involved, this pilot confirmed that blockchain could effectively lower issuance costs.

Other examples abound. South Korea's central bank selected a commercial operator in late 2019 to develop a blockchain-based bond system, though a full rollout may take time. Malaysia's stock exchange has also expressed interest in using blockchain to digitize the bond market, aiming for an end-to-end solution covering issuance, clearing, and settlement.

Back in 2016, then-SEC Chair Mary Jo White highlighted this potential, stating: “Blockchain holds tremendous potential to modernize trading, clearing, and settlement processes in securities markets, simplify business workflows, and even replace certain operational functions.”

It's now widely accepted in both industry and academia that blockchain can enhance the efficiency and lower the costs of securities issuance and settlement, including for bonds. However, initiatives by the Bank of China, Thailand's central bank, and the World Bank treated blockchain purely as a technical tool for issuance—deliberately avoiding any interaction with crypto assets or tokens. Furthermore, these blockchain-issued securities have mostly been privately traded, focusing on operational innovation rather than market structure.

CCB's digital bond represents a new frontier. Crucially, it is the first bond to be publicly tradable on a blockchain. While accepting Bitcoin for purchase may have limited practical significance, issuing on Ethereum truly tokenizes a high-quality off-chain financial asset. This enables finer-grained transactions, lowers participation barriers, and allows ordinary retail investors—not just institutions—to access services previously reserved for large players, all with greater transparency and lower cost. In essence, this is another innovative experiment in technology-driven inclusive finance.

Risks, however, remain. Beyond regulatory uncertainty and potential market speculation or fraud, inherent cybersecurity vulnerabilities—including smart contract bugs and system weaknesses—cannot be ignored. Moreover, blockchain's immutability doesn't fully align with securities markets, where their complexity makes perfect coverage impractical, and regulatory or judicial requirements sometimes necessitate reversing transactions.

Ultimately, technical challenges require technical solutions. The issuance of CCB's digital bonds represents a significant and positive experiment, not just for the traditional securities industry but for the emerging blockchain sector as well. Currently, blockchain—particularly the crypto-asset space—faces several development bottlenecks. Among these, a critical and urgent challenge is the tokenization of large-scale, high-quality off-chain assets, especially traditional financial assets, to bring them on-chain and diversify the ecosystem.

Recently, the crypto derivatives exchange FTX launched equity tokens for major U.S. stocks like Tesla (TSLA), Apple (AAPL), and Amazon (AMZN), as well as for Facebook (FB), Netflix (NFLX), Google (GOOGL), the SPDR S&P 500 ETF (SPY), Alibaba (BABA), Bilibili (BILI), Beyond Meat (BYND), Pfizer (PFE), and BioNTech (BNTX). This allows global retail investors to trade U.S. stocks directly using stablecoins like USDT or BTC. In parallel, projects like Maker DAO have been actively experimenting with tokenizing traditional assets, including physical gold and real estate.

Against this backdrop, CCB's digital bond issuance stands out as another proactive and highly anticipated step forward.