A week ago, an article titled “Xiao Zhan Behind the Scenes: Tencent’s Do-or-Die Battle” sparked widespread discussion.

The piece offers a deep dive into Tencent's business model and its current existential challenges, arguing that the entertainment and media giant faces a severe test. Despite its size, Tencent isn't leading cultural exports or boldly exploring new frontiers. Instead, it relies on monetizing existing markets through traffic, engaging in intense internal competition ("neijuan"), and leveraging its "New Cultural Creatives"—which critics say offer little positive guidance for youth—to capture market share. This model, the article suggests, is unsustainable and must change.

The author concludes bluntly: Tencent must prepare for a fight for its very survival.

As the ancient Chinese text “Xishi Xianwen” (“Ancient Wise Sayings”) notes: “You may diligently plant flowers, yet they refuse to bloom; you may casually stick willow branches in the ground, yet they flourish.” This seemingly paradoxical wisdom holds a profound truth: often, your greatest threat isn't a direct competitor, but an unassuming bystander. Since the dawn of the internet, many industry giants have been toppled by exactly such players. Take Nokia: it exhausted every effort but still failed to keep pace. It wasn't defeated by rivals like Samsung or Motorola, but by Apple—a company originally focused on operating systems and, at the time, seen as merely a "bystander" to the mobile phone wars.

Similarly, chewing gum brands like Doublemint weren't dethroned by competitors like Stride, but by the distraction of WeChat, Taobao, and mobile games.

Consider the classic supermarket checkout line, meticulously designed around customers' "short-term choices." In the past, people waiting to pay would habitually grab a pack of gum. Today, they're more likely to scroll through WeChat, check social media, or even shop online. More directly, many younger consumers have eliminated the checkout line altogether, using apps like Ele.me, Meituan, JD Daojia, Tmall Supermarket, and Daily Preferred to get groceries delivered with a tap.

When an elephant falls, it does so silently. When a giant collapses, its body is still warm.

“A giant's sheer size makes its condition hard to gauge—unlike a startup, where you can feel if it's still warm. A giant's fate is often sealed long before its fall, at the crossroads of a major historical shift.”

If Tencent now stands at the crossroads of the "New Cultural Creatives" era, then Binance, too, is at the threshold of a new chapter. This turning point is marked by Binance's acquisition of CoinMarketCap (CMC), which signals a critical development: Binance's user traffic is fracturing.

01

Binance’s Business Lifeline: Its Users

Binance is a product of perfect timing.

In 2017, when nearly all exchanges supported only fiat trading with simple technical architectures, Binance pioneered crypto-to-crypto trading, ushering in the modern era of digital asset exchanges.

The name “Binance” blends “Binary” and “Finance,” symbolizing the fusion of digital technology and finance. Launched in July 2017, it focused exclusively on crypto-to-crypto trading from day one, aiming to become a “world-class blockchain asset trading platform” that provides a secure, fair, and open environment for digital enthusiasts.

In its first two years, Binance seized three pivotal opportunities:

In 2017, it became the first major exchange to launch crypto-to-crypto trading pairs;

In 2018, it implemented token buybacks and burns;

In 2019, it launched Launchpad, a platform letting users participate in token sales by locking up BNB.

These three moves were instrumental to Binance's rise. Just five months after launch, it grew from zero to over 1.5 million users. In 2019, the BNB lock-up mechanism for Launchpad sales helped propel BNB's market cap from $790 million to a peak of $5.36 billion.

But a closer look reveals that beneath its diverse ventures lies a constant core: global user traffic.

Analyzing Binance's key opportunities in 2017, 2018, and early 2019 shows that the lifeline of its core business is—and always has been—its users.

For three years, Binance played a strong opening hand, building a formidable user base.

Unfortunately, it has since failed to fully cherish this hard-won advantage.

From accusations of manipulated futures contracts to immature intraday options, Binance has begun to erode its once-sterling reputation. Moreover, since the start of 2020, beyond aimless expansion, Binance has yet to identify its next big "opportunity."

Now, Binance is sending a crucial signal: its user traffic is fracturing.

02

Traffic Fracture and Hidden Risks in Binance Earn

Just as Tencent's traffic defense campaign began in 2018, Binance's own quiet battle to defend its user base started in Q4 2019—a period when it lacked a clear new "opportunity" to pursue.

The Boston Matrix identifies two key factors shaping a product portfolio: external market attractiveness and internal company strength.

Applying this to Binance reveals four product categories:

First, "Star Products"—high growth, high market share (growth stage): Launchpad;

Second, "Dog Products"—low growth, low market share (decline stage): Binance Earn and margin lending;

Third, "Question Mark Products"—high growth, low market share (intro stage), and often criticized: futures contracts and options;

Fourth, "Cash Cow Products"—low growth, high market share (maturity stage): altcoin spot trading.

Amid the current uncertainty around Bitcoin's third halving and heightened regulatory scrutiny, Binance's cash cow (altcoin spot trading) and its star product (Launchpad) have failed to deliver critical performance, stalling overall business growth.

Amid the current uncertainty around Bitcoin's third halving and heightened regulatory scrutiny, Binance's cash cow (altcoin spot trading) and its star product (Launchpad) have failed to deliver critical performance, stalling overall business growth.

Consequently, Binance faced a user traffic shortfall, prompting it to aggressively push its "dog products"—most notably Binance Earn. This product features exceptionally high individual subscription limits and carries risks related to potential non-redemption and alleged fund misappropriation.

The key risks associated with Binance Earn include its massive scale of fund management, excessively high individual subscription caps, and a complete lack of regulatory oversight.

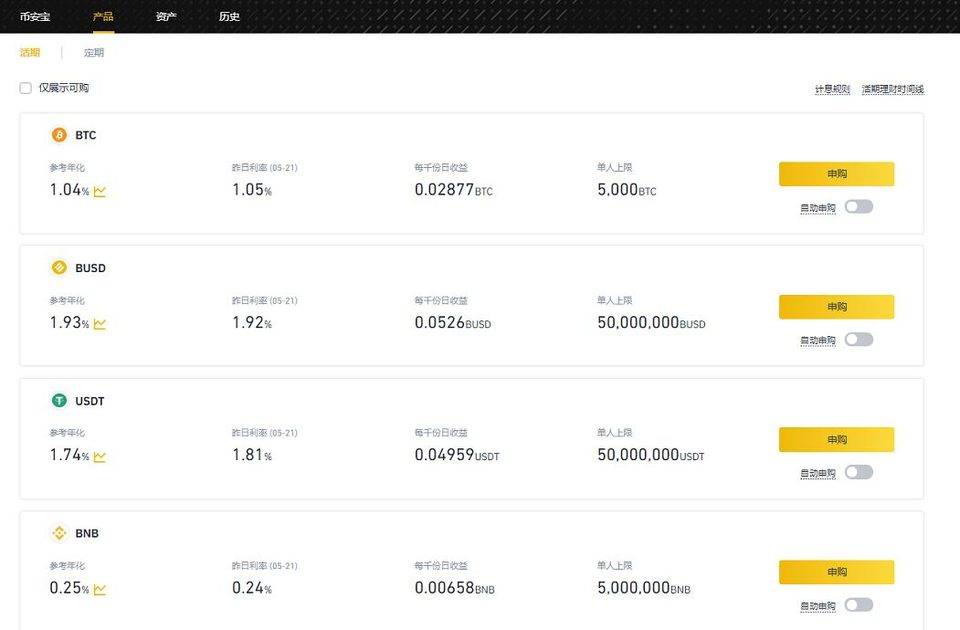

According to Binance's official website, each subscription round for Binance Earn involves enormous volumes. The product supports 23 assets, including BTC, BUSD, USDT, BNB, and ADA, with very high limits for individual participants.

For example, the individual cap for BTC is 5,000 BTC (roughly $45 million). For USDT and BUSD, the cap is 50 million tokens each, totaling $100 million for these two stablecoins. The BNB cap is 5 million BNB (approximately $80 million), while BCH has a cap of 1 million BCH (valued at about $226 million).

Even a conservative estimate suggests that the assets under management (AUM) for a single Binance Earn round easily exceed $100 million.

Such AUM figures would be reasonable for a licensed, regulated private equity fund. However, when wealth management on this scale is conducted by an exchange with no fixed physical address and no clearly defined global legal entity, the risks become extraordinarily high.

Comparing Binance Earn's scale to domestic private equity funds in China reveals that its current size rivals—or even surpasses—that of many established firms.

Data from registered private fund managers in China shows that small to mid-sized firms managing between RMB 50 million and RMB 1 billion form the industry's backbone. As of late April, among the 21,324 registered managers reporting active AUM, the average was just RMB 672 million per firm.

Of these, 4,556 managers reported AUM between RMB 100 million and RMB 500 million, while only 275 had AUM of RMB 10 billion or more.

It's crucial to note that private fund management in China operates under extremely strict regulations.

Preventing financial risk is one of China's three major policy campaigns, and private equity funds are explicitly included. Given their potential to become a new hotspot for financial crime in the post-P2P era, these funds warrant heightened scrutiny. The principle of non-profitability must be upheld: trustees cannot exploit their fiduciary position for personal gain.

However, Binance is not a financial entity operating within any formal legal framework, nor is Binance Earn a regulated private equity fund. So why does Binance need so much capital? Furthermore, who serves as the licensed fund manager for Binance Earn—and where is the on-chain data to verify its operations?

03

Suspected Use of Funds from Non-English Speaking Users

To Buy Traffic from English-Speaking Users

Binance has long marketed itself as the cryptocurrency exchange with the "most authentic traffic." The first prominent figure to publicly question this claim was Yevgeny Devine, an early Bitcoin SV (BSV) investor.

In 2019, after Binance delisted BSV, he tweeted: "70–80% of Binance’s trading volume is fabricated. These fake metrics fuel CZ’s claim of running the 'largest cryptocurrency exchange,' attracting inexperienced investors and projects desperate for listings. Binance grants CZ authority—but that authority is built on a foundation of broken trust."

Devine's earlier concerns take on new significance in light of Binance's $400 million acquisition of CoinMarketCap (CMC) in March. In the crypto world, user traffic can be broadly split into English-speaking and non-English-speaking segments. English-speaking users primarily access services via desktop browsers, while non-English users rely heavily on mobile apps. These are two distinct ecosystems, and CMC serves as a bridge between them.

Within the cryptocurrency industry, users typically don't use traditional search engines like Baidu or Google to look up tokens. Instead, they go directly to specialized data platforms like CMC or Feixiaohao.

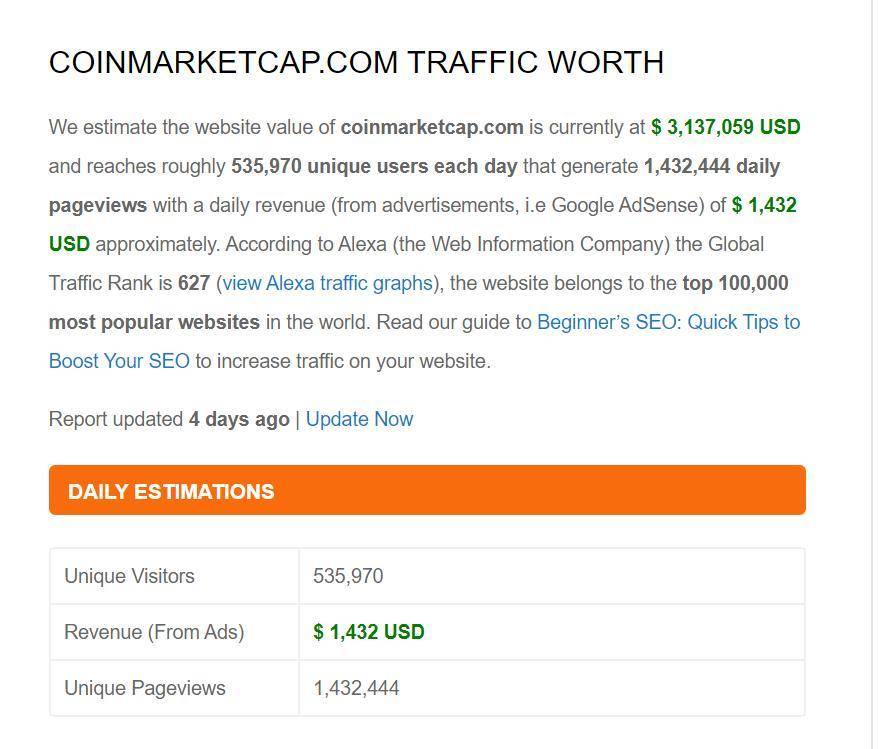

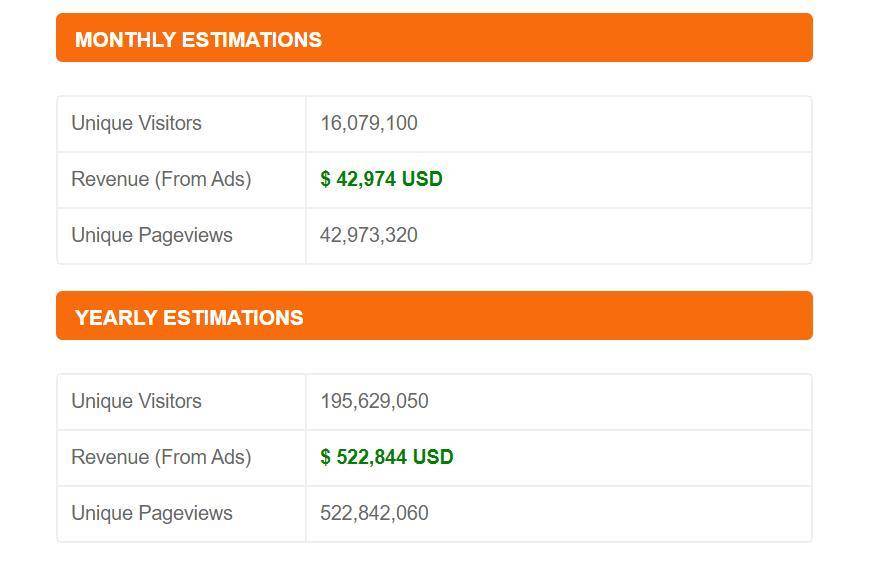

According to SimilarWeb data, CMC is the undisputed central hub for crypto data, attracting 207.2 million visits over the past six months—80% more traffic than Binance's own website. Alexa's global rankings place CMC at #570 worldwide, while Binance sits at #2,045.

This means that while CMC's revenue model may be less lucrative than an exchange's, it remains an exceptionally valuable platform for attracting massive traffic.

In essence, Binance's $400 million acquisition of CMC was a direct attempt to buy English-speaking user traffic to fill its current gap—and thereby generate additional revenue to address its operational challenges.

But where did this $400 million come from? That question demands serious scrutiny.

Although the payment was made in BNB tokens and equity rather than cash, the sum is still enormous. According to official disclosures and statements from CEO Changpeng Zhao (CZ), Binance's 2019 net profit was approximately $550 million—just 72% of its prior-year profit.

With 2020 less than halfway through, such a massive acquisition inevitably creates a significant financial shortfall. How will this gap be filled? Could funds from other Binance products be diverted to cover it? This warrants deeper investigation.

Undoubtedly, this represents a bold and aggressive strategic investment. It also highlights Binance's urgent need to address its traffic gap and structural business issues—challenges that have undermined its profitability and forced it to make a high-stakes move to acquire English-speaking user traffic.

While buying traffic is common in internet business models, CMC's unique position as a data authority means the negative implications of its acquisition may outweigh the benefits—triggering a broader crisis of trust across the cryptocurrency ecosystem.

CoinMarketCap (CMC) built its reputation in the crypto space by earning widespread trust. Binance, on the other hand, has struggled with its own credibility.

An April 2019 report from BTI highlighted severe wash-trading on Binance, with fabricated volumes making up 25–75% of the total for 30 trading pairs. The exchange has also been plagued by server outages, security breaches, and data leaks—some of which rocked the entire industry.

By acquiring CMC, Binance is rewriting the rules. It has already changed CMC’s exchange ranking methodology, adopting web-based metrics that favor English-speaking users to crown itself as the platform’s number-one exchange.

The move sparked industry backlash. Brandon Chez, CMC’s anonymous founder, left the company after the acquisition, citing a desire to focus on his family during the COVID-19 pandemic.

Binance climbed to the top with a simple three-step user onboarding strategy that rapidly expanded its base. But today, an uneven product lineup has led to user churn and fragmented traffic. Its core business isn’t growing in line with the broader market cycle, creating strategic bottlenecks and a pressing need for new sources of users.

The real challenge is improving its underperforming and unproven products to ensure sustainable growth—not just buying English-speaking traffic through CMC while ignoring non-English users.

As mentioned, Binance’s lifeline is its users and reputation. Right now, it’s at a crossroads.

Binance once stood out with superior business models and higher traffic than its rivals.

Now, it seems to be shifting toward a different approach: “Our products might be mediocre, but we can cut off our competitors’ traffic at the source.” By funneling CMC users to Binance and monetizing them through Binance Earn, derivatives, and other high-margin services, Binance aims to boost profits—and then fund more acquisitions and investments to build its empire.

Will a Binance-controlled CMC actually channel traffic and users to help fix Binance’s product gaps? Or is Binance solely focused on profit?

Whether Binance’s post-acquisition strategy is driven by short-term gains or a long-term vision remains unclear.

What is clear is that the rushed acquisition of CMC was a strategic misstep for both companies. Diverting CMC’s traffic into the Binance ecosystem disrupts its existing user base, and the wider crypto community remains unimpressed.

Major shifts in any environment happen gradually—small changes accumulate until they trigger a transformation. The slow decline of the dinosaurs, once the dominant species of the Jurassic, shows how ruthless macro-trends can be.

In today’s climate, competition is often indirect—more like boiling a frog slowly than a head-on fight. The outcome is still brutal, delivered without apology or even a polite “sorry.”

As explored in the article “Xiao Zhan Behind the Scenes: Tencent’s Fight to the Death,” profitability matters for tech giants—but sometimes, something else matters more: fulfilling the mission entrusted by the era.